Fill a Valid 84Ag Nebraska Form

Fill a Valid 84Ag Nebraska Form

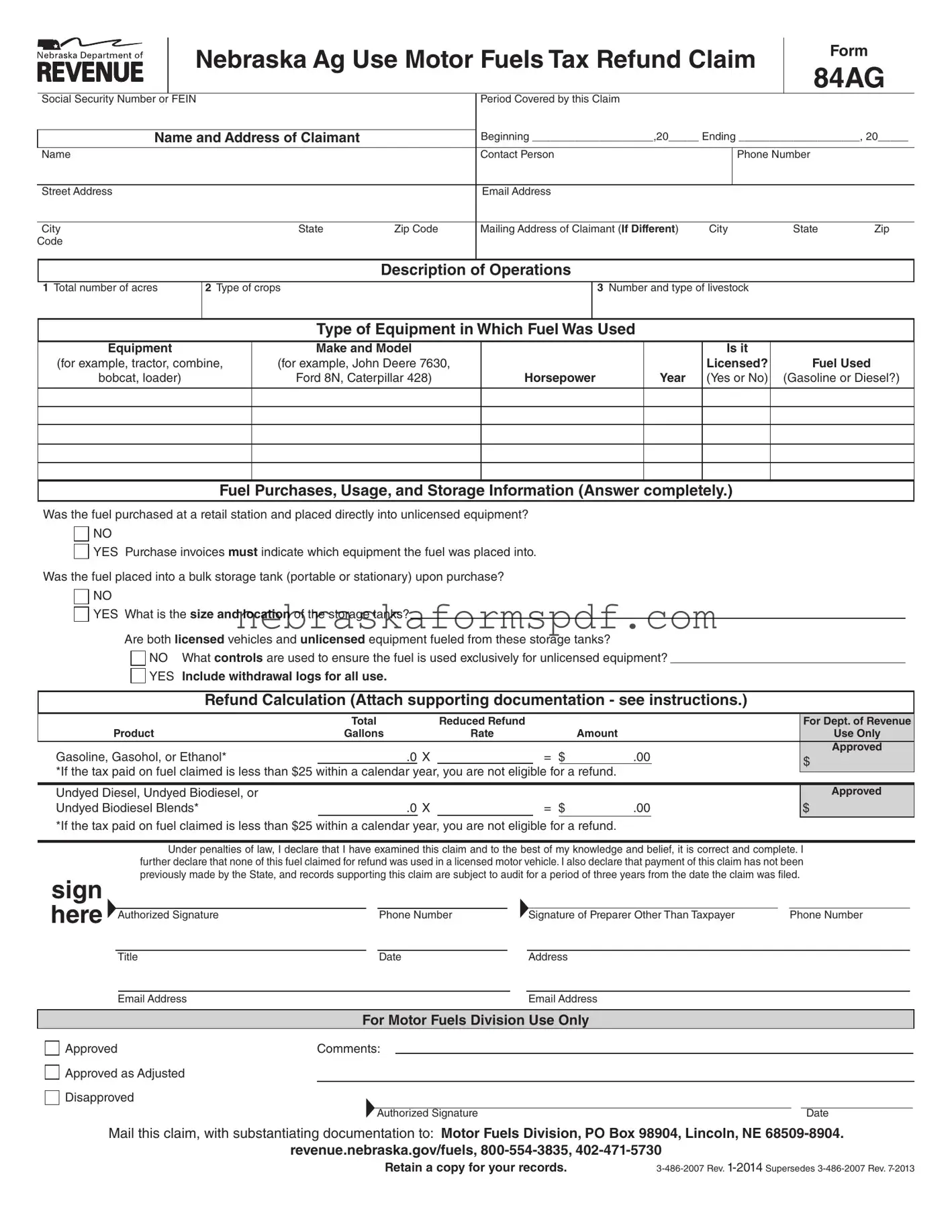

For farmers and ranchers in Nebraska, managing operational costs is a significant aspect of their business, and the Nebraska Ag Use Motor Fuels Tax Refund Claim, Form 84AG, serves as a crucial tool in this financial balance. This form allows individuals to apply for a refund on the motor fuels tax paid on fuel used in unlicensed equipment, specifically for farming or ranching purposes. It covers a range of details, from the period the claim covers, the claimant's name and address, a description of the operations including the number of acres farmed, types of crops raised, and livestock managed. Additionally, it asks for specifics about the equipment in which the fuel was used – including make, model, horsepower, and whether or not the equipment is licensed, alongside the type of fuel used. The claim process requires the submission of detailed documentation including fuel purchase invoices, storage information, and withdrawal logs if applicable, all aiming to verify the tax-paid fuel's eligible use. The form outlines a specific minimum tax paid before filing claims, the timing for submitting claims, and emphasizes the importance of including supporting documentation to substantiate the refund request. Furthermore, it highlights the adjustments and audits that may follow the submission, laying foundational guidelines for ensuring compliance and accurate refund calculation. This introductory discourse into Form 84AG unpacks the involved components and the structured approach to claiming tax refunds, underpinning the due diligence required in harnessing this financial relief measure for the agricultural sector.

Nebraska Ag Use Motor Fuels Tax Refund Claim

Form

84AG

Social Security Number or FEIN |

|

|

|

Period Covered by this Claim |

|

|

|

|

|

||

|

|

|

Beginning ____________________,20_____ Ending ____________________, 20_____ |

||||||||

Name and Address of Claimant |

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|||

Name |

|

|

|

Contact Person |

|

|

Phone Number |

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

Street Address |

|

|

|

|

Email Address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

City |

|

State |

Zip Code |

Mailing Address of Claimant (If Different) |

City |

State |

Zip |

||||

Code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Description of Operations |

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

1 Total number of acres |

2 Type of crops |

|

|

|

3 Number and type of livestock |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Type of Equipment in Which Fuel Was Used |

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

Equipment |

|

Make and Model |

|

|

|

|

Is it |

|

|

||

(for example, tractor, combine, |

(for example, John Deere 7630, |

|

|

|

|

Licensed? |

Fuel Used |

|

|||

bobcat, loader) |

|

Ford 8N, Caterpillar 428) |

|

Horsepower |

Year |

(Yes or No) |

(Gasoline or Diesel?) |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Fuel Purchases, Usage, and Storage Information (Answer completely.)

Was the fuel purchased at a retail station and placed directly into unlicensed equipment?

NO

YES Purchase invoices must indicate which equipment the fuel was placed into.

Was the fuel placed into a bulk storage tank (portable or stationary) upon purchase?

NO

YES What is the size and location of the storage tanks?

Are both licensed vehicles and unlicensed equipment fueled from these storage tanks?

NO What controls are used to ensure the fuel is used exclusively for unlicensed equipment?

YES Include withdrawal logs for all use.

Refund Calculation (Attach supporting documentation - see instructions.)

|

Total |

|

|

Reduced Refund |

|

|

|

|

|

For Dept. of Revenue |

Product |

Gallons |

|

|

Rate |

|

|

Amount |

|

|

Use Only |

Gasoline, Gasohol, or Ethanol* |

|

.0 |

X |

|

= |

$ |

.00 |

|

Approved |

|

|

|

$ |

||||||||

|

|

|

|

|

|

|

|

|

|

|

*If the tax paid on fuel claimed is less than $25 within a calendar year, you are not eligible for a refund. |

|

|

||||||||

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

Undyed Diesel, Undyed Biodiesel, or |

|

|

|

|

|

|

|

|

|

Approved |

Undyed Biodiesel Blends* |

|

.0 |

X |

|

= |

$ |

.00 |

|

$ |

|

|

|

|

|

|

|

|

|

|

|

|

*If the tax paid on fuel claimed is less than $25 within a calendar year, you are not eligible for a refund.

sign here

Under penalties of law, I declare that I have examined this claim and to the best of my knowledge and belief, it is correct and complete. I further declare that none of this fuel claimed for refund was used in a licensed motor vehicle. I also declare that payment of this claim has not been previously made by the State, and records supporting this claim are subject to audit for a period of three years from the date the claim was filed.

|

|

|

|

|

|

|

|

|

|

|

Authorized Signature |

|

Phone Number |

|

|

Signature of Preparer Other Than Taxpayer |

|

Phone Number |

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

Title |

|

Date |

|

|

Address |

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

Email Address |

|

|

|

|

Email Address |

|

|

|

For Motor Fuels Division Use Only

Approved |

Comments: |

|

|

|

|

Approved as Adjusted |

|

|

|

|

|

Disapproved |

|

|

|

|

|

|

|

|

|

|

|

|

|

Authorized Signature |

Date |

||

Mail this claim, with substantiating documentation to: Motor Fuels Division, PO Box 98904, Lincoln, NE

revenue.nebraska.gov/fuels,

Retain a copy for your records. |

Instructions

Caution: Only federal governmental agencies and buses for hire are eligible for the refund of tax on fuel placed into a licensed motor vehicle. All other users of fuel in licensed motor vehicles, regardless of how those vehicles are used, are not eligible for a refund of motor fuels tax.

Note: All refund claims are subject to audit for three years after the claim is iled.

Who May File. Any person requesting a refund of Nebraska motor fuels tax paid on fuel used in unlicensed equipment for farming or ranching purposes may ile a Nebraska Ag Use Motor Fuels Tax Refund Claim, Form 84AG. Prior to adjustments, the tax paid on the eligible fuel must be at least $25. This minimum must be

met within a calendar year for each fuel type.

When to File. Only one claim per month may be iled by any claimant. You must ile your claim within three

years from the date of payment of the tax.

Where to File. This claim, along with supporting documentation, must be iled with the Nebraska Department of Revenue, Motor Fuels Division, PO Box 98904, Lincoln, NE

Basis for Claim. Appropriate documentation must be attached to the Form 84AG. Documentation submitted with the Form 84AG will not be returned.

Exempt Use of

Required Documentation. In order to support the claim, the following information must be included:

•A description of your operations must be submitted with the initial claim, and then on an annual basis; include the number of acres farmed, types of crops raised, and the number and type of livestock;

•A list of the type of equipment in which the fuel was used must be submitted with the initial claim, and then on an annual basis; include the make, horsepower, and other mechanical description of the machinery;

•Information regarding the fuel purchase usage and storage;

•Legible copies of fuel purchase invoices indicating the amount of tax paid, the date of purchase, fuel type, gallons purchased, and vendor’s name. If the fuel was placed directly into unlicensed equipment, the equipment fueled must be indicated on the invoice; and

•Legible copies of withdrawal logs documenting the date, gallons, and equipment into

which the fuel was placed if both licensed vehicles and unlicensed equipment are fueled from the same storage facility (refer to the Nebraska Motor Fuels Tax Refunds Information Guide for additional information).

If your documentation exceeds the Form 84AG space limitations, you may attach additional sheets of paper.

Specific Instructions for Calculating the Refund

Multiply the number of gallons claimed by the refund rate in effect when the fuel was purchased and enter the amount calculated. Round all gallon and dollar amounts from .50 to .99 to the next higher whole number. Round all gallon and dollar amounts less than .50 to the next lower whole number. If gallons are claimed for periods with

multiple refund rates, attach a summary of these calculations.

Refund Rates. The refund of the tax paid on fuel consumed in a qualiied exempt manner is determined at a

reduced rate. See the refund rate table for the correct rate.

Signatures (Original signature required). This claim must be signed by the claimant, partner, member, or corporate oficer. If the claimant authorizes another person to sign this claim, a Power of Attorney, Form 33, must

be attached. Any person who is paid for preparing a claim must also sign the claim as preparer.

| Fact Number | Fact Detail |

|---|---|

| 1 | The form is titled "Nebraska Ag Use Motor Fuels Tax Refund Claim Form 84AG". |

| 2 | It is designed for individuals seeking a refund of the Nebraska motor fuels tax paid on fuel used in unlicensed equipment for farming or ranching purposes. |

| 3 | The minimum tax paid on the eligible fuel must be at least $25 within a calendar year for each fuel type before any adjustments. |

| 4 | Claimants can file only one claim per month and must do so within three years from the date the tax was paid. |

| 5 | Claims must be filed with the Nebraska Department of Revenue, Motor Fuels Division. |

| 6 | Required documentation includes a description of operations, a list of equipment in which the fuel was used, information on fuel purchase, usage and storage, and copies of fuel purchase invoices and withdrawal logs. |

| 7 | Refund calculation is based on the number of gallons claimed multiplied by the refund rate in effect when the fuel was purchased. |

| 8 | The claim must be signed by the claimant, a partner, member, or corporate officer. If the claim is prepared by another person, a Power of Attorney form must be attached, and the preparer must also sign the claim. |

| 9 | Claims and any fuel refund activities are subject to audit by the state for three years after the claim is filed. |

Filing a Nebraska Ag Use Motor Fuels Tax Refund Claim Form 84AG requires careful attention to detail to ensure all necessary information is accurately provided. This documentation is essential for individuals seeking a refund for taxes paid on fuel used in unlicensed equipment, primarily for agriculture. The following steps are designed to guide you through completing the form correctly. Remember, providing clear and correct information is crucial for the processing of your claim.

By following these steps, you can ensure your claim is submitted correctly. Remember, this process is designed to reclaim taxes paid on fuel that was used for qualifying agricultural purposes. Accuracy and thoroughness in filling out the Form 84AG and in compiling your documentation can help expedite the review process.

The Form 84AG, known as the Nebraska Ag Use Motor Fuels Tax Refund Claim, is a document specifically designed for individuals or entities requesting a refund of Nebraska motor fuels tax. This tax is paid on fuel that is used exclusively in unlicensed equipment for farming or ranching operations. If you operate a farm or ranch and use fuel in equipment such as tractors, combines, or loaders that are not licensed for road use, you may be eligible to file this form to claim a refund on the taxes paid on this fuel.

The form allows for the filing of one claim per month by any claimant. However, there is an important timeframe to be aware of - the claim must be filed within three years from the date the tax on the fuel was paid. This means that if you have fuel invoices or records going back up to three years, you may be able to file a claim for a refund on the taxes paid during that period, but you cannot file for refunds on taxes paid before this three-year window.

To ensure a successful claim, several pieces of documentation are required alongside Form 84AG:

If there is insufficient space on the Form 84AG for all your supporting documentation, you are allowed to attach additional sheets of paper to ensure that all necessary information is included.

The refund amount is calculated by multiplying the number of gallons for which the refund is claimed by the refund rate in effect at the time of fuel purchase. It's important to note that these calculations should be rounded to the nearest whole number, with amounts from .50 to .99 rounded up and amounts less than .50 rounded down. If multiple refund rates apply to the gallons claimed due to purchases at different times, a summary of these calculations must be attached to the form. This calculation ensures that claimants receive a refund commensurate with the actual taxed amount paid on the fuel consumed in qualified exempt operations.

Completed forms, along with all required supporting documentation, should be mailed to the Nebraska Department of Revenue, Motor Fuils Division at PO Box 98904, Lincoln, NE 68509-8904. Keeping a copy of the entire submission for your records is advised, as the documents submitted will not be returned. This process helps to ensure that your claim is processed efficiently and allows you to retain evidence of your submission for future reference or in the event of an audit.

Filling out the 84Ag Nebraska form, which is used to claim a refund for Nebraska motor fuels tax paid on fuel used in unlicensed equipment for farming or ranching purposes, requires attention to detail. Common mistakes can lead to delays or the denial of the claim. Understanding and avoiding these errors can streamline the process.

Incorrect or incomplete Social Security Number (SSN) or Federal Employer Identification Number (FEIN): It is critical to provide a correct and complete SSN or FEIN. This number is a key identifier, and any mistake can result in processing delays or a failure to recognize the claimant.

Misunderstanding the period covered: Each claim must specify the exact beginning and ending dates of the period for which the refund is sought. Claims cannot be processed if these dates are not clearly stated or if they cover an incorrect period for the intended refund.

Inaccurate description of operations: The form requires detailed descriptions of operations, including the total number of acres farmed, types of crops raised, and the number and type of livestock. Claims often fail to provide sufficient detail, which can affect eligibility and the refund amount.

Omitting equipment details: The make, model, horsepower, and other specifics of the equipment where the fuel was used must be accurately described. Errors or omissions in this section can lead to questions about the validity of the claim.

Incorrect fuel usage information: Claimants must specify whether the fuel was placed directly into unlicensed equipment or a bulk storage tank. Incorrect answers, especially regarding the control measures taken to ensure fuel is used exclusively for unlicensed equipment, can invalidate a claim.

Failure to attach purchase invoices and withdrawal logs: These documents are critical for substantiating the claim. They must clearly indicate the amount of tax paid, the date of purchase, the type of fuel, gallons purchased, and for which equipment the fuel was used.

Errors in refund calculation: The refund calculation must be done correctly, taking into account the specific rates for gasoline, gasohol, ethanol, undyed diesel, undyed biodiesel, and approved undyed biodiesel blends. Incorrect calculations can lead to reduced refunds.

Missing or incorrect signatures: The form must be signed by the claimant or an authorized representative. If prepared by someone other than the taxpayer, that individual must also sign the form. Missing or incorrect signatures can lead to the rejection of the claim.

The following practices can also enhance the success of your claim:

Double-check all information: Before submission, reviewing the entire form for accuracy and completeness can prevent many common mistakes.

Ensure documentation is legible: Illegible documents can delay processing. Ensure all supporting documentation is clear and readable.

Understand eligibility: Not all uses of fuel qualify for a refund. Reviewing the program guidelines carefully can prevent the submission of ineligible claims.

Adhere to deadlines: Claims must be filed within three years from the date of payment of the tax. Late submissions may not be accepted.

By avoiding these common mistakes and adhering to the form's instructions, claimants can streamline the process of claiming a refund for the Nebraska motor fuels tax. Comprehensive and careful preparation of the 84Ag form is essential for a successful claim.

When it comes to managing agricultural operations in Nebraska, savvy farmers and ranchers know that maximizing returns often involves understanding the nuances of tax benefits and refund opportunities. The Nebraska Ag Use Motor Fuels Tax Refund Claim, Form 84AG, provides an excellent case in point. Filing this form correctly and on time can lead to significant savings, but it doesn't stand alone. To complement this process and ensure a thorough and compliant submission, several other forms and documents often accompany Form 84AG. Together, these documents create a comprehensive snapshot of an operation's eligibility for fuel tax refunds, offering a smoother pathway through Nebraska's tax landscape.

Preparing a claim for a motor fuel tax refund involves more than just filling out and submitting Form 84AG. It's about assembling a comprehensive dossier that reflects the scale, nature, and specifics of your agricultural operation. With the correct supporting documents and forms in hand, you're not just submitting paperwork; you're laying down the groundwork for potential savings that can be reinvested into your operation. Whether it's ensuring the accuracy of fuel purchase invoices or keeping meticulous withdrawal logs, each document plays its part in supporting your claim. Navigate the paperwork with care, and you'll find that Nebraska's agricultural tax benefits can offer a substantial boost to your operation's bottom line.

The 84Ag Nebraska form, officially known as the Nebraska Ag Use Motor Fuels Tax Refund Claim Form 84AG, is specifically tailored for individuals requesting a refund of Nebraska motor fuels tax paid on fuel used in unlicensed equipment for farming or ranching activities. This form shares similarities with several other documents designed to reclaim taxes or fees for specialized purposes. Each of these documents, while unique in its application, carries a fundamental similarity in structure, purpose, and the kind of detailed information required from the claimant.

One such document is the Federal Heavy Vehicle Use Tax (HVUT) Form 2290. Despite its focus on the taxation of heavy vehicle usage on public highways, similarities with the 84Ag form become apparent in the necessity for detailed vehicle and operational descriptions. Just as the 84Ag form requires a breakdown of equipment used, acres farmed, types of crops, and livestock, Form 2290 demands specifics about the taxable vehicles, including their weight, usage, and identifying information. Both forms serve a purpose in the agrarian and transportation industries by allowing for tax refunds or credits based on the nature of the use of equipment or vehicles, emphasizing precise record-keeping and documentation of use.

Another document sharing parallels with the 84Ag form is the State Sales Tax Exemption Certificate utilized by agricultural producers to purchase supplies and equipment without paying state sales tax. Although this certificate directly relates to the exemption of taxes at the point of purchase rather than a refund of taxes paid, the underlying similarity lies in the requirement to detail the nature of agricultural operations. Claimants must describe the agricultural use of purchased items, closely mirroring the 84Ag's need to detail the agricultural use of fuel. This similarity highlights the broader theme of tax advantage mechanisms available to those in agricultural sectors, underlining the importance of detailed operational disclosures to qualify for financial benefits.

Finally, the Energy Star Rebate Form for energy-efficient appliances and equipment shares a resemblance with the 84Ag form in its intention to offer financial returns for specific types of purchases or uses. While the Energy Star Rebate is geared towards encouraging energy efficiency through rebates on purchases, the structural similarity with the 84Ag form lies in the requirement for applicants to provide detailed information about the purchase, including the type of equipment, its use, and the expected efficiency or savings. Both forms incentivize a certain type of expenditure—energy efficiency in one and agricultural fuel use in the other—demonstrating the government's role in influencing consumer behavior through financial incentives.

Filing out the Form 84AG in Nebraska, a document designed for claiming a tax refund on motor fuels used in agricultural operations, demands careful attention to detail and adherence to certain rules. Proper completion and submission of this form can lead to successful refunds, aiding in the reduction of operational costs for farming and ranching businesses. Here are some do's and don'ts that should be kept in mind when tackling this form:

Do:Understanding the Nebraska Ag Use Motor Fuels Tax Refund Claim Form 84AG can sometimes be challenging due to various misconceptions. Here, we’ll address 10 common misunderstandings to help clarify the process.

Only for large-scale farmers: Some believe this refund is strictly for large-scale farming operations. However, any individual or entity using motor fuels in unlicensed equipment for farming or ranching purposes, meeting the claim requirements, can file.

Personal information isn't secure: Concerns about providing social security numbers or FEINs are common. The state ensures the confidentiality and security of this information as part of the claim process.

Refunds apply to all fuel types: There’s a misconception that all fuel types are eligible for a refund. In reality, the refund pertains only to undyed diesel, gasoline, gasohol, ethanol, and undyed biodiesel, under specific conditions.

No deadline for filing: Some think claims can be filed anytime. Claims must be filed within three years from the date of tax payment, emphasizing the importance of timely submissions.

One claim per year: Unlike the belief that only one claim can be filed annually, claimants are actually allowed to file one claim per month, enabling more frequent refunds.

Documentation is returned: It's mistakenly assumed that submitted documentation with the Form 84AG will be returned. All provided documentation will not be returned; hence, keeping copies is crucial.

Refund amount is fixed: The refund amount is not fixed but calculated based on the number of gallons claimed at the reduced rate, which may vary.

No audit risk: There’s a false assumption that submitted claims aren’t subject to review. All claims can be audited for up to three years after filing, making accurate and honest reporting vital.

Only for vehicles: While the focus is on motor fuels, the refund is not just for fuel used in vehicles but extends to all unlicensed equipment used for agriculture, such as tractors and combines.

Immediate processing: Some expect immediate refund processing upon submission. The review process can take time, especially during peak periods, requiring patience.

Clarifying these misconceptions helps streamline the process, making it more understandable and accessible for those eligible to claim the Nebraska Ag Use Motor Fuels Tax Refund.

When completing the Nebraska Ag Use Motor Fuels Tax Refund Claim Form 84AG, it's crucial to understand its requirements and processes to ensure accuracy and compliance. Here are key takeaways to guide you:

Please note: The Nebraska Ag Use Motor Fuels Tax Refund Claim Form 84AG is subject to audit for three years after the claim has been filed. This necessitates maintaining accurate and comprehensive records to support your claim should any questions arise during an audit.

Nebraska 1040n - Designed to ensure compliance and streamline administrative processes for businesses adjusting their operational or tax-related details in Nebraska.

Or Title Application - Dealerships must specify their service capabilities or provide a service agreement for external repairs.