Fill a Valid Nebraska 1040N Form

Fill a Valid Nebraska 1040N Form

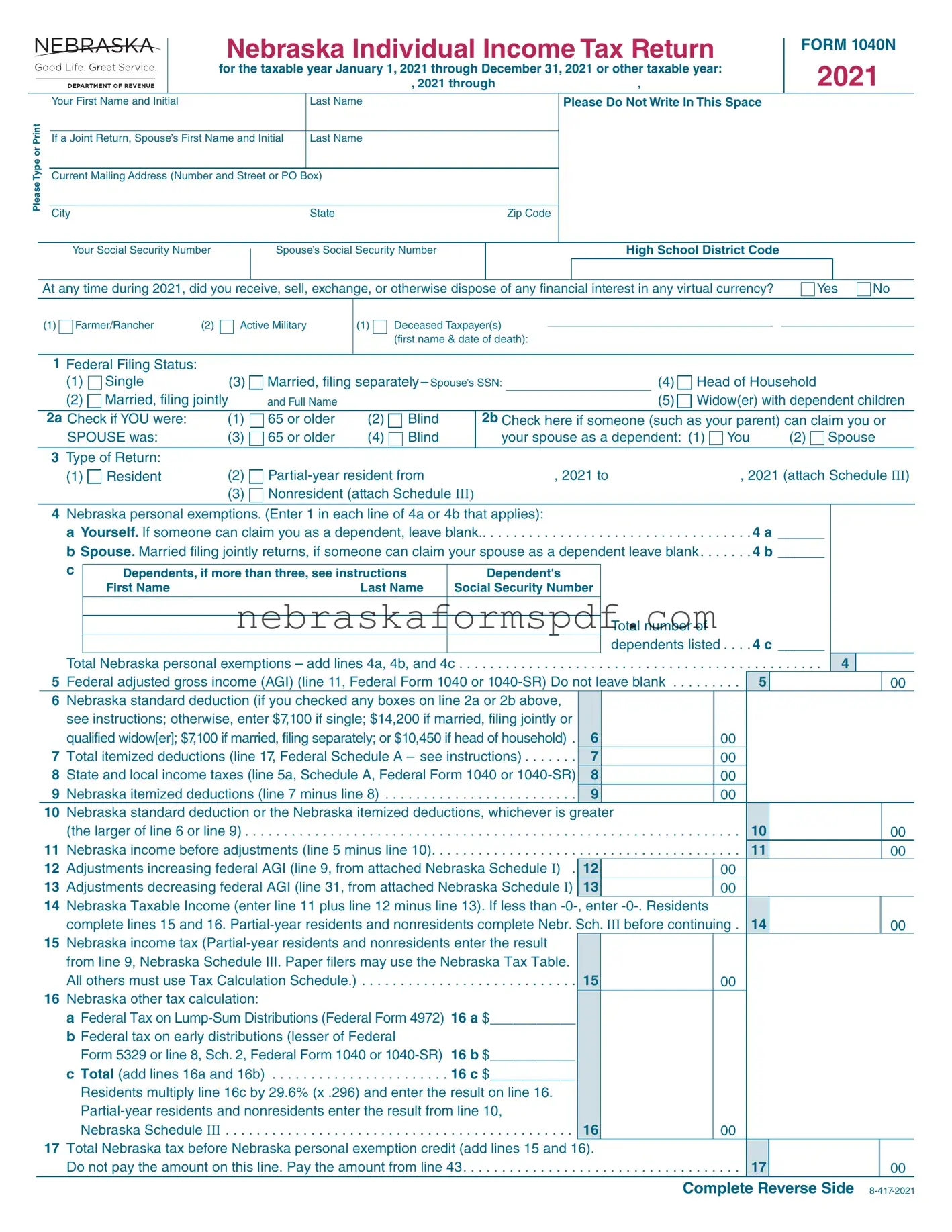

The Nebraska 1040N form is a comprehensive document designed for state residents to report their annual income, calculate taxes due, and claim refunds where applicable for the taxable year starting January 1, 2020, through December 31, 2020, or for any other designated taxable period. Essential for both individuals and families, this form requires meticulous input of personal information, including Social Security Numbers for you and your spouse if filing jointly, as well as your current mailing address. It accommodates various filing statuses, such as single, married (filing jointly or separately), head of household, and widow(er) with dependent children, and includes sections for documenting federal adjusted gross income, adjustments to income, Nebraska personal exemptions, and the option to take either the Nebraska standard deduction or itemized deductions. Additionally, it provides spaces for reporting tax credits like those for elderly or disabled individuals, financial institution tax, or child and dependent care, alongside sections for calculating Nebraska income tax, other taxes, potential penalties for underpayment, and use tax on purchases not covered by collected sales tax. This form concludes with options for allocating overpayments towards future estimated taxes, making charitable donations, and specifying if the refund should be directly deposited into a bank account, highlighting its role not just in tax reporting, but in personal financial management as well.

FORM 1040N

for the taxable year January 1, 2021 through December 31, 2021 or other taxable year:

, 2021 through |

, |

Please Type or Print

Your First Name and Initial |

Last Name |

If a Joint Return, Spouse’s First Name and Initial |

Last Name |

|

|

Current Mailing Address (Number and Street or PO Box) |

|

City |

State |

Zip Code

Please Do Not Write In This Space

Your Social Security Number

Spouse’s Social Security Number

High School District Code

At any time during 2021, did you receive, sell, exchange, or otherwise dispose of any financial interest in any virtual currency?

Yes

No

(1)

Farmer/Rancher (2)

Active Military

(1)

Deceased Taxpayer(s)

(first name & date of death):

1Federal Filing Status:

(1) |

Single |

(3) |

Married, filing separately – Spouse’s SSN: |

|

(4) |

Head of Household |

||||

(2) |

Married, filing jointly |

and Full Name |

|

|

|

(5) |

Widow(er) with dependent children |

|||

|

|

|

|

|

|

|

||||

2a Check if YOU were: |

(1) |

65 or older |

(2) |

Blind |

2b Check here if someone (such as your parent) can claim you or |

|||||

SPOUSE was: |

(3) |

65 or older |

(4) |

Blind |

your spouse as a dependent: (1) You |

(2) Spouse |

||||

|

|

|

|

|

|

|

|

|

|

|

3 Type of Return: |

|

|

|

|

|

|

|

|

|

|

(1) |

Resident |

(2) |

|

, 2021 to |

, 2021 (attach Schedule III) |

|||||

|

|

(3) |

Nonresident (attach Schedule III) |

|

|

|

|

|

||

4Nebraska personal exemptions. (Enter 1 in each line of 4a or 4b that applies):

a Yourself. If someone can claim you as a dependent, leave blank.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4 a ______

b Spouse. Married filing jointly returns, if someone can claim your spouse as a dependent leave blank |

. 4 b ______ |

|

|

|

||||||

c |

|

|

|

|

|

|

|

|

||

Dependents, if more than three, see instructions |

Dependent's |

|

|

|

|

|

|

|||

|

First Name |

Last Name |

Social Security Number |

|

|

|

|

|

|

|

|

|

|

|

Total number of |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

dependents listed . . . |

. 4 c ______ |

|

|

|

||

Total Nebraska personal exemptions – add lines 4a, 4b, and 4c |

. . . . . . . |

4 |

|

|

||||||

5 Federal adjusted gross income (AGI) (line 11, Federal Form 1040 or |

|

5 |

|

|

00 |

|||||

6Nebraska standard deduction (if you checked any boxes on line 2a or 2b above, see instructions; otherwise, enter $7,100 if single; $14,200 if married, filing jointly or

|

qualified widow[er]; $7,100 if married, filing separately; or $10,450 if head of household) . |

6 |

00 |

7 |

Total itemized deductions (line 17, Federal Schedule A – see instructions) |

7 |

00 |

8 |

State and local income taxes (line 5a, Schedule A, Federal Form 1040 or |

8 |

00 |

9 |

Nebraska itemized deductions (line 7 minus line 8) |

9 |

00 |

10Nebraska standard deduction or the Nebraska itemized deductions, whichever is greater

|

(the larger of line 6 or line 9) |

. . . |

. . . . . . . . . . . . . . . . . . |

10 |

00 |

||

11 |

Nebraska income before adjustments (line 5 minus line 10) |

. . . |

11 |

00 |

|||

12 |

Adjustments increasing federal AGI (line 9, from attached Nebraska Schedule I) . |

12 |

|

00 |

|

|

|

13 |

Adjustments decreasing federal AGI (line 31, from attached Nebraska Schedule I) |

13 |

|

00 |

|

|

|

14Nebraska Taxable Income (enter line 11 plus line 12 minus line 13). If less than

|

complete lines 15 and 16. |

00 |

|||

15 |

Nebraska income tax |

|

|

|

|

|

from line 9, Nebraska Schedule III. Paper filers may use the Nebraska Tax Table. |

|

|

|

|

|

All others must use Tax Calculation Schedule.) |

15 |

00 |

|

|

16 |

Nebraska other tax calculation: |

|

|

|

|

aFederal Tax on

bFederal tax on early distributions (lesser of Federal

Form 5329 or line 8, Sch. 2, Federal Form 1040 or

c Total (add lines 16a and 16b) |

16 c $___________ |

|

Residents multiply line 16c by 29.6% (x .296) and enter the result on line 16. |

|

|

|

||

Nebraska Schedule III |

. . . . . . . . . . . . . . . . 16 |

00 |

17Total Nebraska tax before Nebraska personal exemption credit (add lines 15 and 16).

Do not pay the amount on this line. Pay the amount from line 43 |

. . . . . . . . 17 |

00 |

|

Complete Reverse Side |

18 |

Nebr. personal exemption credit for residents only ($142 times the number on line 4) |

18 |

|

00 |

|

|

|

19 |

Credit for tax paid to another state, line 6, Nebraska Schedule II |

|

|

|

|

|

|

|

. . |

. . . . . |

19 |

|

00 |

|

|

20 |

. .Credit for the elderly or disabled (attach copy of Federal Schedule R) . . . |

. . . . . |

20 |

|

00 |

|

|

21 |

. .Community Development Assistance Act credit (attach Form CDN) |

. . . . . |

21 |

|

00 |

|

|

22 |

. .Form 3800N nonrefundable credit (attach Form 3800N) |

. . . . . |

22 |

|

00 |

|

|

23 |

Nebraska child/dependent care nonrefundable credit, only if line 5 is more |

|

|

|

|

|

|

|

than $29,000 |

. . . . . |

23 |

|

00 |

|

|

24 |

. .Credit for financial institution tax (attach Form NFC) |

. . . . . |

24 |

|

00 |

|

|

25 |

. . .Employer’s credit for expenses incurred for TANF (ADC) recipients (see instr.) |

25 |

|

00 |

|

|

|

26 |

. .School Readiness Tax Credit for providers (see instructions) |

. . . . . |

26 |

|

00 |

|

|

27 |

. .Designated extremely blighted area tax credit (attach Form |

. . . . |

27 |

|

00 |

|

|

28 |

. .Total nonrefundable credits (add lines 18 through 27) |

. . . . . |

. . . |

. . . . . . . . . . . . . . . . . . |

|||

|

|

|

|

|

|

|

|

29Nebraska tax after nonrefundable credits. Subtract line 28 from line 17 (if line 28 is more than line 17, enter

federal tax, check box and |

29 |

30Total Nebraska income tax withheld (attach 2021 Forms, see instructions)

a |

|

|

|

c |

30 |

00 |

312021 estimated income tax payments (include any 2020 overpayment credited to

|

2021 and any payments submitted with an extension request) |

. . . 31 |

00 |

|

|||||

|

Form 3800N refundable credit (attach Form 3800N) |

|

|

|

|

||||

32 |

. . . 32 |

00 |

|

||||||

33 |

Nebraska child/dependent care refundable credit, if line 5 is $29,000 or less |

|

|

|

|

||||

|

(attach a copy of Form 2441N) . . |

. . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . . |

. . . 33 |

00 |

|

||

|

Beginning Farmer credit from Form 1099 BFC (NDA NextGen) |

|

|

|

|

||||

34 |

. . . 34 |

00 |

|

||||||

35 |

Nebraska earned income credit. Enter number of qualifying children 97 |

|

|

|

|

|

|||

|

Federal credit 98 $ |

|

.00 |

x .10 (10%) |

|

35 |

00 |

|

|

36 |

Nebraska Property Tax Incentive Act Credit |

. . . 36 |

00 |

|

|||||

|

Credit for qualified Volunteer Emergency Responders (see instructions) |

|

|

|

|

||||

37 |

. . . 37 |

00 |

|

||||||

|

School Readiness Tax Credit for qualified staff members (see instructions) |

|

|

|

|

||||

38 |

. . . 38 |

00 |

|

||||||

39 |

. . . . . . . . . . . . . . . . . . . . . . .Total refundable credits (add lines 30 through 38) |

. . . |

. . . . . . . . . . . . . . . . . . . |

. . |

39 |

||||

40Penalty for underpayment of estimated tax (see instructions). If you calculated a Form 2210N penalty of

or greater, or used the annualized income method, attach Form 2210N, and check this box 96

. . . . . . . . 40

. . . . . . . . 40

41 Total tax and penalty. Add lines 29 and 40 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41

42Use tax due on taxable purchases where applicable sales tax was not collected. (see instructions) Enter purchases subject to state tax 91 $__________ State tax 92 $___________ (purchases x 5.5%); Enter purchases subject to local tax 93 $__________ Local tax 94 $_______ (purchases x local rate of ____%) 95 Local code__ __ __(see local rate schedule);

Add state and local taxes and enter on line 42. If no use tax is due, enter |

42 |

43Total amount due. If line 39 is less than total of lines 41 and 42, subtract line 39 from the total of lines 41

|

and 42. Pay this amount in full. For electronic or credit card payment, check here |

and see instructions . . |

. . 43 |

|||

44 |

Overpayment. If line 39 is more than total of lines 41 and 42, subtract total of lines 41 and 42 from line 39. |

. . 44 |

||||

45 |

Amount of line 44 you want applied to your 2022 estimated tax |

45 |

|

|

00 |

|

46 |

Wildlife Conservation Fund donation of $1 or more |

46 |

|

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

47Amount of line 44 you want refunded to you (line 44 minus lines 45 and 46) Your

|

|

(see instructions) |

. . . . . . . . . . . . 47 |

48a |

Routing Number |

48b Type of Account |

1 = Checking 2 = Savings |

48c |

Account Number |

|

|

48d |

Check this box if this refund will go to a bank account outside the United States. |

|

|

00

00

00

00

00

00

00

00

00

Under penalties of perjury, I declare that, as taxpayer or preparer, I have examined this return and to the best of my knowledge and belief, it is true, correct, and complete.

sign

here |

|

|

|

|

|

Your Signature |

|

Date |

|

Email Address |

Keep a copy of this return for your records.

Spouse’s Signature (if filing jointly, both must sign) |

|

Daytime Phone |

paid preparer’s use only

use only

Preparer’s Signature |

|

Date |

|

|

Preparer’s PTIN |

|

|

|

|

|

|

|

|

|

|

Print Firm’s Name (or yours if |

|

|

EIN |

|

Daytime Phone |

||

Mail returns requesting a refund to: Nebraska Department of Revenue, PO Box 98912, Lincoln, NE

| Fact | Description |

|---|---|

| Purpose of Form 1040N | Form 1040N is used by residents, partial-year residents, and nonresidents of Nebraska to file their state income tax for the year 2020 or other specified taxable year. |

| Types of Returns | Form 1040N accommodates different types of filers: residents, partial-year residents (requiring Schedule III), and nonresidents (also requiring Schedule III). |

| Filing Status Options | Taxpayers can select from multiple filing statuses: Single, Married filing jointly, Married filing separately, Head of Household, or Widow(er) with dependent children. |

| Personal and Dependency Exemptions | Taxpayers can claim personal exemptions for themselves, their spouse, and dependents, while specific conditions affect the amounts entered for each category. |

| Governing Laws | The Nebraska Form 1040N is governed by the state tax laws and regulations of Nebraska, which dictate the taxation rules for individuals and entities within the state. |

Successfully navigating the completion of the Nebraska 1040N form requires a detailed, methodical approach. This state-specific tax documentation, fundamental for residents to adhere to taxation regulations, involves a series of steps aimed at capturing taxpayer information, income details, deductions, and credits. By following a structured guideline, taxpayers ensure compliance with Nebraska tax laws while potentially optimizing their fiscal responsibilities.

Upon successful review and verification of all entries for accuracy and completeness, forward the form to the designated address based on whether you are expecting a refund or not. Keeping a copy of the completed form and associated documents for your records is advisable.

The Nebraska 1040N form is the state income tax return form for residents of Nebraska. It is used to report annual income and calculate the state income tax owed for the year. The form covers the taxable year from January 1, 2020, through December 31, 2020, or for any other taxable year specified by the taxpayer.

Any resident, partial-year resident, or nonresident who has received income from Nebraska sources during the taxable year must file the Nebraska 1040N form. This includes individuals who work in Nebraska, own property in the state, or have other income-generating activities within Nebraska.

Your filing status on the Nebraska 1040N form should match your federal filing status. The options include single, married filing jointly, married filing separately, head of household, and widow(er) with dependent child. Your filing status affects your standard deduction and tax rate.

The Nebraska 1040N form must be filed by April 15th following the end of the tax year. If the due date falls on a weekend or holiday, the deadline is extended to the next business day. Taxpayers who need more time can request an extension, which grants additional time to file but not to pay any taxes owed.

Exemptions can be claimed for yourself, your spouse (if filing jointly), and any dependents. Each exemption reduces your taxable income. If you or your spouse can be claimed as a dependent on someone else's return, you should not claim the personal exemption for yourself or your spouse.

Note: These amounts are adjusted for taxpayers who are 65 or older or blind.

Your taxable income is calculated by taking your federal adjusted gross income, applying the Nebraska standard or itemized deductions, and then subtracting any allowances for exemptions. Specific adjustments specific to Nebraska may also need to be considered.

If you are requesting a refund, mail your completed form to the Nebraska Department of Revenue, PO Box 98912, Lincoln, NE 68509-8912. If you are not requesting a refund, send it to PO Box 98934, Lincoln, NE 68509-8934. Remember to keep a copy of the return for your records.

Filling out the Nebraska 1040N form can sometimes be complex, and taxpayers often make mistakes, leading to delays in processing their returns or impacting their tax liabilities. Understanding these common errors can help ensure that your tax return is accurate and processed efficiently.

Incorrect Social Security Numbers - A frequent mistake people make is entering an incorrect Social Security number (SSN). Your SSN and your spouse’s SSN, if filing jointly, must be entered exactly as they appear on your Social Security cards. Mistakes here can lead to significant processing delays or mismatches in tax records.

Failing to Choose the Correct Filing Status - The choice of filing status affects your tax liability significantly. Taxpayers often select the wrong status, such as Single instead of Head of Household, or Married Filing Jointly instead of Married Filing Separately. Each status comes with different tax implications, so it's crucial to choose the one that best fits your situation.

Errors in Calculating Deductions - Whether choosing to itemize deductions or take the standard deduction, errors in calculation can impact your taxable income. For instance, not understanding which deductions you are legally entitled to or incorrect arithmetic can either inflate your tax liability or understate your taxable income, leading to possible audits or penalties.

Overlooking Tax Credits - Many taxpayers miss out on valuable tax credits such as the Credit for Tax Paid to Another State, the Nebraska Child/Dependent Care Credit, or the Earned Income Credit. Each of these credits can reduce your overall tax bill and, in some cases, lead to a refund. Failing to claim applicable credits means missing out on potential savings.

While preparing your Nebraska 1040N form, double-check each section for accuracy. Reviewing the instructions provided by the Nebraska Department of Revenue and consulting with a tax professional if unsure can help avoid these common mistakes. Remember, taking the time to fill out your tax return carefully can save you time, money, and potential legal issues in the long run.

Filing taxes can sometimes feel like assembling a complex puzzle where each piece represents a different form or document. In Nebraska, the journey often begins with a 1040N form, but it rarely ends there. Alongside the primary form, there are several additional pieces that taxpayers might need to complete this financial picture. Here's a closer look at up to five forms and documents commonly used in tandem with the Nebraska 1040N form, each serving its own unique purpose in the tax filing process.

Each of these documents plays an integral role in ensuring that you accurately report and potentially minimize your tax obligations within the requirements of Nebraska state law. Whether it's detailing out-of-state income, adjusting for state-specific income or deductions, or claiming tax credits, these additional forms ensure that taxpayers can navigate their state tax filings with greater ease and precision. Just like pieces of a puzzle, combining these forms with the 1040N allows Nebraska residents to complete their tax picture clearly and correctly.

The Nebraska 1040N form is similar to the Federal Form 1040 in structure and purpose. Both forms are used by taxpayers to file their annual income tax. The Federal Form 1040 serves as the standard IRS form for individuals to report their annual income, calculate applicable taxes, and determine refunds or tax owed to the federal government. Similarly, the Nebraska 1040N form is the state counterpart for residents of Nebraska, allowing them to report income, calculate state tax liability, and claim any refunds owed from the state. Each form requires information about the taxpayer's income, tax deductions, credits, and personal exemptions. Though they serve the same fundamental purpose, the key difference lies in their jurisdictional focus—one is for federal tax obligations, while the other addresses state-specific tax requirements.

Another document similar to the Nebraska 1040N form is the Schedule III, which is attached to the 1040N for partial-year residents and nonresidents to calculate their Nebraska source income. Like the federal Schedule C used to report profit or loss from a business, Nebraska's Schedule III focuses on adjusting the taxpayer's income based on the portion that is attributable to Nebraska. This form is necessary because partial-year residents and nonresidents have income that may be sourced from multiple states, and only income earned from Nebraska sources needs to be reported for state tax purposes. Therefore, while Schedule C adjusts federal taxable income based on business profits and losses, Nebraska's Schedule III adjusts state taxable income based on residency status and source of income.

Filling out the Nebraska 1040N form is an important process for residents to ensure they are compliant with state tax laws. To make this process smoother, here is a list of things you should and shouldn't do.

Things You Should Do:Following these guidelines will help streamline the filing process, ensuring accuracy and compliance with Nebraska's tax requirements.

Understanding the Nebraska 1040N form can sometimes be as challenging as navigating a corn maze in the dark. With various sections and numbers to fill in, it's easy to get lost in the details. To shine a light on the path, let’s debunk some common misconceptions about the Nebraska 1040N form:

It’s important to approach tax filing with accurate information to ensure a smooth process and avoid unnecessary errors. The Nebraska 1041N form, with all its complexities, is no exception. By demystifying these misconceptions, we take a step closer to navigating tax season with confidence.

Nebraska Notary Rules - Details the legal implications of an oath or affirmation taken before a Notary, emphasizing the truthfulness and accuracy required.

Nebraska Sales Tax Registration - Corporations and partnerships are required to disclose detailed ownership and officer information, facilitating transparent business registrations.