Fill a Valid Nebraska 12N Form

Fill a Valid Nebraska 12N Form

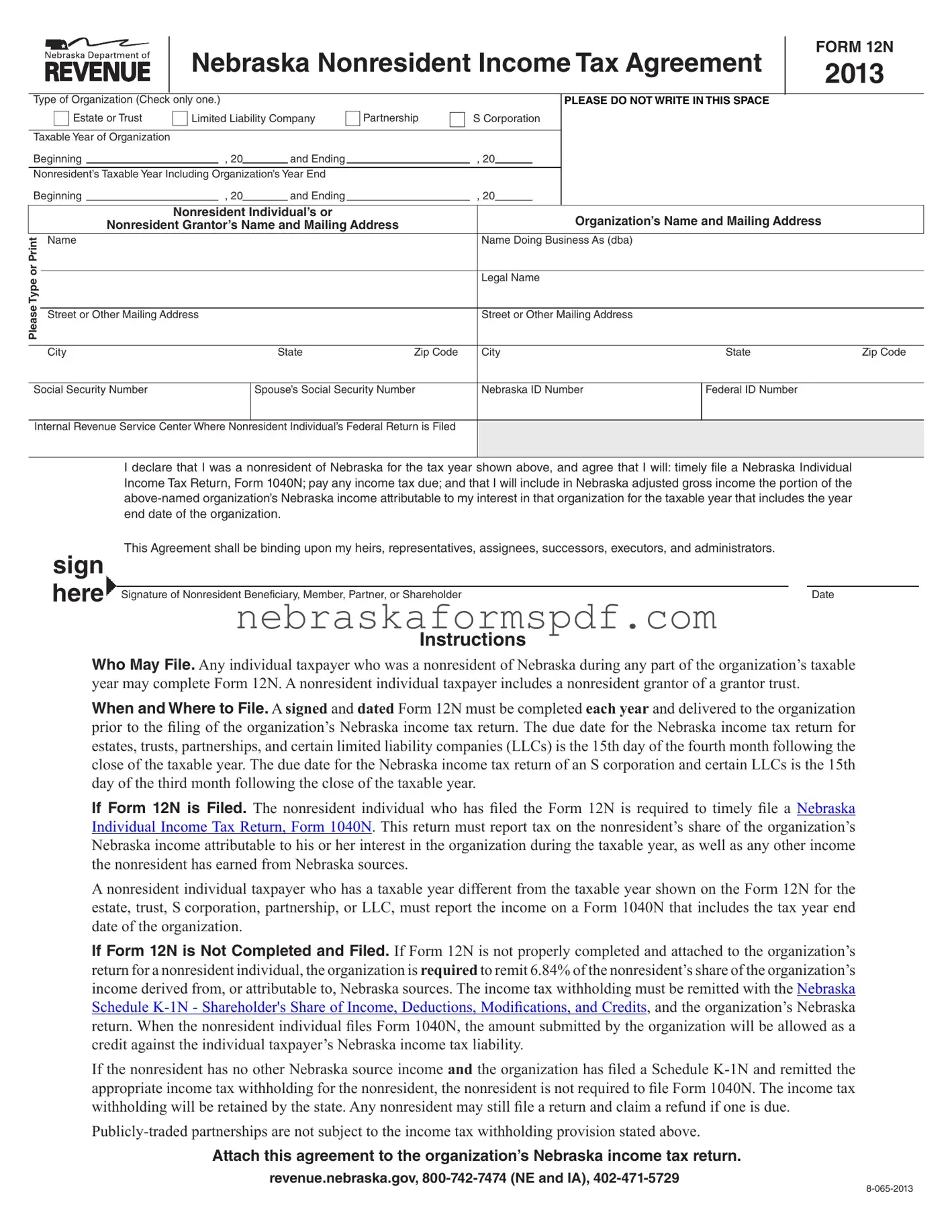

In the landscape of tax obligations, the Nebraska 12N form emerges as a pivotal document for nonresidents earning income within the state's borders. Tailored for individuals who were not residents of Nebraska during the taxable year, this form encapsulates an agreement between nonresident individuals—spanning from members of estates or trusts to partners in various organizational structures—and the state of Nebraska. The essence of the Form 12N lies in its requirement for nonresidents to declare their income derived from Nebraska sources, ensuring the timely filing of a Nebraska Individual Income Tax Return (Form 1040N) and the settlement of any resultant tax dues. Furthermore, this form spells out the obligations of entities such as estates, trusts, partnerships, S corporations, and certain limited liability companies (LLCs) in detailing the tax year and the nonresident's portion of income attributable to Nebraska operations. Critical deadlines are set forth for these organizations, underlining the necessity for punctuality in submissions to avoid the mandatory withholding of a portion of the nonresident’s income at a flat rate. Additionally, the procedure offers a pathway to rectify oversight by allowing nonresidents to claim refunds under specific conditions. The Form 12N stands as a testament to Nebraska’s methodical approach to tax administration, presenting a structured process to ensure that nonresidents contribute their fair share to the state's coffers, while delineating clear steps for compliance and potential remuneration.

Nebraska Nonresident Income Tax Agreement

FORM 12N

2013

Type of Organization (Check only one.) |

|

|

|

|

|

PLEASE DO NOT WRITE IN THIS SPACE |

||||

Estate or Trust |

Limited Liability Company |

Partnership |

S Corporation |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

Taxable Year of Organization |

|

|

|

|

|

|

|

|

|

|

Beginning |

|

|

, 20 |

|

and Ending |

|

, 20 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Nonresident’s Taxable Year Including Organization’s Year End |

|

|

|

|

|

|||||

Beginning |

|

|

, 20 |

|

and Ending |

|

, 20 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Nonresident Individual’s or

Nonresident Grantor’s Name and Mailing Address

Type or Print |

Name |

|

|

|

|

|

|

|

|

Please |

Street or Other Mailing Address |

|

|

|

|

|

|

|

|

|

City |

|

State |

Zip Code |

Social Security Number |

|

Spouse’s Social Security Number |

||

|

||||

|

|

|

|

|

Internal Revenue Service Center Where Nonresident Individual’s Federal Return is Filed

Organization’s Name and Mailing Address

Name Doing Business As (dba)

Legal Name

Street or Other Mailing Address

City |

|

State |

Zip Code |

Nebraska ID Number |

|

Federal ID Number |

|

|

|

||

|

|

|

|

|

|

|

|

sign here

I declare that I was a nonresident of Nebraska for the tax year shown above, and agree that I will: timely file a Nebraska Individual Income Tax Return, Form 1040N; pay any income tax due; and that I will include in Nebraska adjusted gross income the portion of the

This Agreement shall be binding upon my heirs, representatives, assignees, successors, executors, and administrators.

Signature of Nonresident Beneficiary, Member, Partner, or Shareholder |

Date |

Instructions

Who May File. Any individual taxpayer who was a nonresident of Nebraska during any part of the organization’s taxable year may complete Form 12N. A nonresident individual taxpayer includes a nonresident grantor of a grantor trust.

When and Where to File. A signed and dated Form 12N must be completed each year and delivered to the organization prior to the iling of the organization’s Nebraska income tax return. The due date for the Nebraska income tax return for

estates, trusts, partnerships, and certain limited liability companies (LLCs) is the 15th day of the fourth month following the close of the taxable year. The due date for the Nebraska income tax return of an S corporation and certain LLCs is the 15th

day of the third month following the close of the taxable year.

If Form 12N is Filed. The nonresident individual who has iled the Form 12N is required to timely ile a Nebraska

Individual Income Tax Return, Form 1040N. This return must report tax on the nonresident’s share of the organization’s

Nebraska income attributable to his or her interest in the organization during the taxable year, as well as any other income the nonresident has earned from Nebraska sources.

A nonresident individual taxpayer who has a taxable year different from the taxable year shown on the Form 12N for the estate, trust, S corporation, partnership, or LLC, must report the income on a Form 1040N that includes the tax year end

date of the organization.

If Form 12N is Not Completed and Filed. If Form 12N is not properly completed and attached to the organization’s return for a nonresident individual, the organization is required to remit 6.84% of the nonresident’s share of the organization’s income derived from, or attributable to, Nebraska sources. The income tax withholding must be remitted with the Nebraska Schedule

credit against the individual taxpayer’s Nebraska income tax liability.

If the nonresident has no other Nebraska source income and the organization has iled a Schedule

Attach this agreement to the organization’s Nebraska income tax return.

revenue.nebraska.gov,

| Fact Name | Description |

|---|---|

| Purpose of Form 12N | This form is an agreement for nonresidents of Nebraska, confirming their commitment to file a Nebraska Individual Income Tax Return (Form 1040N) and pay taxes on income earned from Nebraska sources for the tax year. |

| Eligible Filers | Nonresident individuals of Nebraska, including nonresident grantors of grantor trusts, who earned income from an organization operating within Nebraska during the taxable year. |

| Due Dates for Filing | Form 12N must be delivered to the organization before it files its Nebraska income tax return. The specific due date varies by the type of organization, generally the 15th day of the fourth month after the organization's tax year ends for estates, trusts, partnerships, and certain LLCs, and the 15th day of the third month for S corporations and certain other LLCs. |

| Requirement if Form 12N is Filed | Upon filing Form 12N, the nonresident must file Form 1040N, reporting their share of the organization’s Nebraska income and any other Nebraska-source income. |

| Consequences of Not Filing Form 12N | If not filed, the organization must withhold 6.84% of the nonresident's Nebraska-source income and remit it with the Nebraska income tax return. This amount can be credited against the nonresident's Nebraska income tax liability when they file Form 1040N. |

| Governing Law | The requirements and procedures for Form 12N are governed by Nebraska state tax law, specifically as it pertains to nonresident income tax liability and compliance. |

Filing Nebraska Form 12N, the Nonresident Income Tax Agreement, is a necessary step for every nonresident who earns income from a Nebraska entity and seeks to comply with state tax laws. This form plays a critical role in how income earned in Nebraska by nonresidents is reported and taxed. It not only facilitates the right tax treatment of such income but also affects how nonresidents complete their tax obligations. Let's navigate through the steps required to complete this form accurately and ensure that all information is presented clearly.

After completing Form 12N, it's crucial to deliver it to the organization concerned before the organization files its Nebraska income tax return. The timing is key here — the form must be submitted each year as part of compliance. Should there be discrepancies or a failure to file, it could result in the organization being responsible for withholding a percentage of the income for tax purposes, a situation that ideally both parties would prefer to avoid. Thus, accurate and timely submission of Form 12N benefits all involved by ensuring proper income reporting and tax treatment under Nebraska state laws.

The Nebraska 12N Form, known as the Nebraska Nonresident Income Tax Agreement, is a document that nonresident individuals of Nebraska associated with certain types of organizations - such as estates, trusts, S corporations, partnerships, and some limited liability companies (LLCs) - must complete. This form demonstrates the individual's commitment to file a Nebraska Individual Income Tax Return (Form 1040N), pay any applicable income tax, and include in their Nebraska adjusted gross income any income attributed to their interest in the specified organization for the tax year.

Any individual taxpayer who was a nonresident of Nebraska during any part of the taxable year of the organization stated on the form needs to file the Nebraska 12N Form. This includes nonresident grantors of a grantor trust. Essentially, if an individual has income from an organization that operates in Nebraska and is one of the organization types listed, they are required to complete this agreement.

The Nebraska 12N Form should be signed, dated, and delivered to the associated organization before the filing of the organization's Nebraska income tax return. For estates, trusts, partnerships, and some LLCs, the due date is the 15th day of the fourth month following the end of the taxable year. For S corporations and certain LLCs, the deadline is the 15th day of the third month following the close of the taxable year. The completed form should be attached to the organization’s Nebraska income tax return upon submission.

If a nonresident fails to complete and submit the Form 12N, the organization they're associated with is mandated to withhold 6.84% of the nonresident's share of the organization’s Nebraska-sourced income. This withheld amount must be remitted with the Nebraska Schedule K-1N and the organization's Nebraska income tax return. The withheld taxes will be credited against the nonresident individual's Nebraska income tax liability when they file Form 1040N. If there's no other Nebraska source income and taxes have been withheld properly, the nonresident may not be required to file a return, unless they seek a refund.

Yes, if an individual taxpayer has a taxable year that differs from the organization’s taxable year, they are still required to file Form 12N. When reporting the income on their Nebraska Individual Income Tax Return (Form 1040N), it should include the organization's year-end date to properly align the reported income with the correct tax period.

Yes, if the organization has fulfilled its obligation by filing a Schedule K-1N and remitting the appropriate income tax withholding for the nonresident's Nebraska-sourced income, and the nonresident has no other Nebraska source income, they are not required to file Form 1040N. However, any nonresident can file a return to claim a refund if one is due. Notably, publicly traded partnerships are exempt from the income tax withholding requirement outlined for other organizations.

Filling out the Nebraska 12N form, officially known as the Nebraska Nonresident Income Tax Agreement, is a critical step for nonresident individuals to ensure they are in compliance with state tax regulations. However, misunderstandings or errors in filling out this form can lead to complications or delays. Here are five common mistakes to avoid:

By paying close attention to these details, nonresident individuals can avoid common pitfalls when completing the Nebraska 12N form. Successfully navigating these challenges ensures compliance with Nebraska’s tax requirements and aids in the efficient processing of nonresident income tax agreements. Remember, it is always advisable to review the form thoroughly before submitting it and consult with a tax professional if there are questions or complexities in your tax situation. Understanding the nuances of state tax laws can be tricky, but careful attention to the specifics of tax forms like the Nebraska 12N can prevent unnecessary complications.

When dealing with the Nebraska Nonresident Income Tax Agreement, also known as Form 12N, there are several other forms and documents that individuals often need to be aware of to ensure compliance and precision in their tax filings. Each of these documents plays a unique role in the broader scope of tax preparation, affecting different aspects of the tax process for nonresidents and those with interests in various types of organizations within Nebraska.

Compiling all necessary documents and forms, such as those mentioned above, plays a crucial role in fulfilling tax obligations accurately. Having a comprehensive understanding of each document’s purpose helps smoothen the tax filing process, ensuring individuals meet their responsibilities without overlooking crucial details. Individuals working with these forms are encouraged to seek guidance as needed and stay informed about any changes to state tax laws that may affect their filings.

The Nebraska 12N form is similar to other tax documents that nonresident individuals or entities must file in various contexts, specifically when they have income associated with a state in which they do not reside. These documents often serve the purpose of declaring income received and ensuring compliance with state tax laws. Each document, while tailored to the requirements of different states or circumstances, shares the objective of reporting and managing tax responsibilities for nonresident income.

The Nebraska 12N form and the California Form 540NR share similarities in that both are designed for nonresidents to report income earned within the respective states. The California 540NR, much like the Nebraska 12N, allows individuals who are not residents of California but have earned income from California sources during the taxable year to calculate and report their state income tax. Both forms require detailed information about the income earned, personal information of the filer, and calculations to determine the amount of tax owed based on the income attributable to the state's sources.

Comparing the Nebraska 12N form with the New York IT-203 form, one notices that both serve nonresidents who need to report their income and calculate state taxes owed. The New York IT-203 form is used by individuals who are not residents of New York but have earned income from New York sources. Similar to the Nebraska 12N, this form includes sections for reporting the taxpayer's income, tax deductions, and credits applicable to reduce the tax liability associated with New York-sourced income. Both forms play a crucial role in ensuring that nonresidents contribute to the tax revenues of the states where they earn their income, despite not residing in those states.

When filing the Nebraska 12N form, it's crucial to follow specific guidelines to ensure the process is smooth and error-free. Here are the dos and don'ts that one should keep in mind:

Do:Understanding the Nebraska Nonresident Income Tax Agreement, or Form 12N, is crucial for nonresident individuals, grantors, and beneficiaries with income from Nebraska sources. However, there are common misconceptions that need clarification to ensure proper compliance and avoid potential legal pitfalls:

It’s imperative for nonresidents earning income from Nebraska sources to fully understand the requirements and implications of Form 12N. Ensuring accurate and timely filing can avoid unnecessary penalties and secure compliance with Nebraska tax laws.

Filling out and using the Nebraska 12N form is crucial for nonresidents involved with certain organizations within the state. Here are key takeaways to ensure compliance and understanding:

Adherence to these guidelines ensures compliance with Nebraska tax obligations for nonresident individuals involved in partnerships, LLCs, trusts, and other entities requiring the completion of Form 12N.

Nebraska Sales Tax Filing - Details the tax payment process for purchases made by governmental entities not engaged in utility services.

Form 941 Irs - For accurate tax reporting, Form 14N captures the essence of tax withheld for nonresidents, paving the way for transparent tax compliance.