Fill a Valid Nebraska 14N Form

Fill a Valid Nebraska 14N Form

The intricacies of tax compliance for nonresident individuals in Nebraska revolve significantly around the completion of the Nebraska 14N form, formally known as the Statement of Nebraska Income Tax Withheld for Nonresident Individual. This crucial document facilitates the withholding process of income tax for nonresidents involved in various organizational structures such as estates, trusts, S corporations, partnerships not publicly traded, and limited liability companies (LLCs). The form stands as a testament to the organization's adherence to tax withholding requirements, earmarking 6.84% of the income subject to withholding for nonresident individuals. It serves not only as a record of withheld tax but also as a beacon guiding nonresident individuals through their tax liabilities in Nebraska, offering detailed instructions on its filing alongside an organization's Nebraska income tax return. Exceptionally, it caters specifically to individuals, excluding entities, and extends its coverage to nonresident grantors of grantor trusts, highlighting the broad spectrum of its applicability. Moreover, the eligibility criteria for filing, juxtaposed with the provisions for non-filing in certain scenarios, articulate a nuanced approach to taxation – which not only ensures compliance but also underscores the state’s commitment to an equitable tax system. Interestingly, the form is pivotal for nonresidents as it influences their Nebraska income tax returns, where the amount withheld can be credited against their tax liabilities. This interconnectedness of documentation underscores the complexity and the seamless integration of tax protocols, ensuring a comprehensive framework for tax administration in Nebraska.

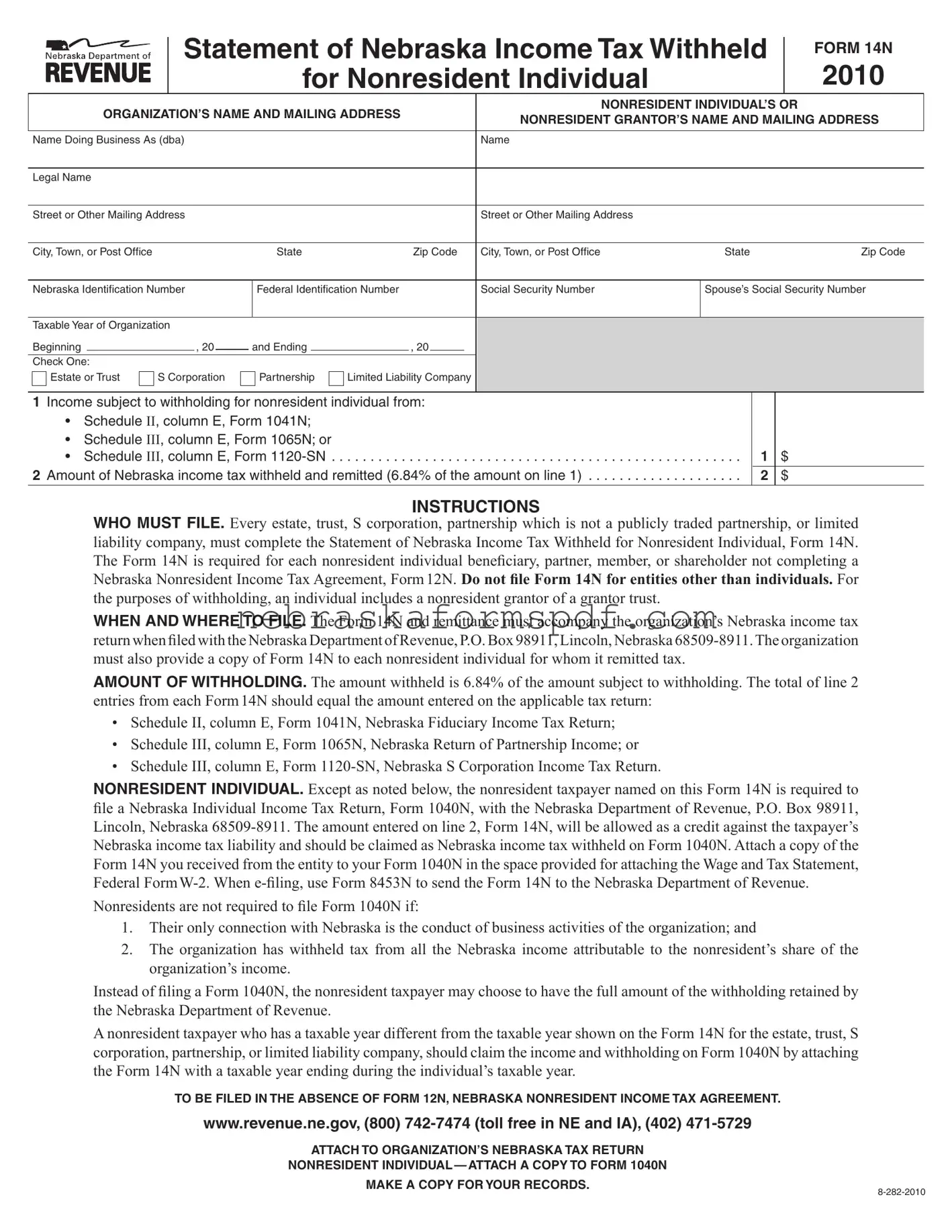

Statement of Nebraska Income Tax Withheld

for Nonresident Individual

FORM 14N

2010

|

ORGANIZATION’S NAME AND MAILING ADDRESS |

|

|

|

|

NONRESIDENT INDIVIDUAL’S OR |

|

||||||||

|

|

|

|

NONRESIDENT GRANTOR’S NAME AND MAILING ADDRESS |

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name Doing Business As (dba) |

|

|

|

|

|

|

Name |

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Legal Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Street or Other Mailing Address |

|

|

|

|

|

|

Street or Other Mailing Address |

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City, Town, or Post Office |

|

|

|

|

State |

|

Zip Code |

City, Town, or Post Office |

|

State |

Zip Code |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Nebraska Identification Number |

Federal Identification Number |

|

|

|

Social Security Number |

|

Spouse’s Social Security Number |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Taxable Year of Organization |

|

|

|

|

|

|

|

|

|

|

|||||

Beginning |

|

|

, 20 |

|

|

and Ending |

|

|

, 20 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

Check One: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Estate or Trust |

S Corporation |

Partnership |

Limited Liability Company |

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1 |

Income subject to withholding for nonresident individual from: |

||

|

|

• ScheduleII, column E, Form 1041N; |

|

|

|

• |

Schedule III, column E, Form 1065N; or |

|

|

• |

Schedule III, column E, Form |

2 |

Amount of Nebraska income tax withheld and remitted (6.84% of the amount on line 1) |

||

1$

2$

INSTRUCTIONS

WHO MUST FILE. Every estate, trust, S corporation, partnership which is not a publicly traded partnership, or limited liability company, must complete the Statement of Nebraska Income Tax Withheld for Nonresident Individual, Form 14N.

The Form 14N is required for each nonresident individual beneiciary, partner, member, or shareholder not completing a Nebraska Nonresident Income Tax Agreement, Form 12N. Do not ile Form 14N for entities other than individuals. For the purposes of withholding, an individual includes a nonresident grantor of a grantor trust.

WHEN AND WHERE TO FILE. The Form 14N and remittance must accompany the organization’s Nebraska income tax return when iled with the Nebraska Department of Revenue, P.O. Box 98911, Lincoln, Nebraska

must also provide a copy of Form 14N to each nonresident individual for whom it remitted tax.

AMOUNT OF WITHHOLDING. The amount withheld is 6.84% of the amount subject to withholding. The total of line 2

entries from each Form14N should equal the amount entered on the applicable tax return:

•Schedule II, column E, Form 1041N, Nebraska Fiduciary Income Tax Return;

•Schedule III, column E, Form 1065N, Nebraska Return of Partnership Income; or

•Schedule III, column E, Form

NONRESIDENT INDIVIDUAL. Except as noted below, the nonresident taxpayer named on this Form 14N is required to ile a Nebraska Individual Income Tax Return, Form 1040N, with the Nebraska Department of Revenue, P.O. Box 98911, Lincoln, Nebraska

Nonresidents are not required to ile Form 1040N if:

1.Their only connection with Nebraska is the conduct of business activities of the organization; and

2.The organization has withheld tax from all the Nebraska income attributable to the nonresident’s share of the organization’s income.

Instead of iling a Form 1040N, the nonresident taxpayer may choose to have the full amount of the withholding retained by the Nebraska Department of Revenue.

A nonresident taxpayer who has a taxable year different from the taxable year shown on the Form 14N for the estate, trust, S corporation, partnership, or limited liability company, should claim the income and withholding on Form 1040N by attaching the Form 14N with a taxable year ending during the individual’s taxable year.

TO BE FILED IN THE ABSENCE OF FORM 12N, NEBRASKA NONRESIDENT INCOME TAX AGREEMENT.

www.revenue.ne.gov, (800)

ATTACH TO ORGANIZATION’S NEBRASKA TAX RETURN

NONRESIDENT INDIVIDUAL — ATTACH A COPY TO FORM 1040N

MAKE A COPY FOR YOUR RECORDS.

| Fact Number | Fact Detail |

|---|---|

| 1 | Form 14N is titled "Statement of Nebraska Income Tax Withheld for Nonresident Individual". |

| 2 | This form is used by estates, trusts, S corporations, partnerships not publicly traded, or limited liability companies. |

| 3 | The purpose of Form 14N is to document Nebraska income tax withheld for nonresident individuals. |

| 4 | Form 14N must be completed for each nonresident individual not completing Nebraska Nonresident Income Tax Agreement, Form 12N. |

| 5 | The form requires details such as the organization's and nonresident individual's name, addresses, and identification numbers. |

| 6 | Nebraska income tax is withheld at a rate of 6.84% of the income subject to withholding. |

| 7 | Form 14N and remittance should accompany the organization's Nebraska income tax return when filed. |

| 8 | The nonresident individual must file a Nebraska Individual Income Tax Return, Form 1040N, and can credit the amount on Form 14N against their Nebraska income tax liability. |

| 9 | Governing law for Form 14N includes regulations for income tax withholding and reporting for nonresident individuals as specified by the Nebraska Department of Revenue. |

Filling out the Nebraska 14N form is a crucial step for any entity required to withhold income tax for nonresident individuals. This guide will walk through the essential steps, ensuring accuracy and compliance. After completion, the form and its accompanying payment must be submitted with the entity's Nebraska income tax return. Additionally, a copy of the Form 14N should be provided to each nonresident individual on whose behalf tax was withheld, assisting them in claiming a credit against their Nebraska income tax liability.

After completing these steps, it’s important to forward the necessary documents and payment to the Nebraska Department of Revenue by the prescribed deadline. This process not only meets tax obligations but also supports nonresident individuals in managing their Nebraska tax responsibilities efficiently.

Form 14N, officially named the Statement of Nebraska Income Tax Withheld for Nonresident Individual, must be completed and filed by every estate, trust, S corporation, partnership that is not a publicly traded partnership, or limited liability company operating within Nebraska. This requirement is specifically for these entities to report and remit withheld income tax for each nonresident individual who is a beneficiary, partner, member, or shareholder and who has not completed a Nebraska Nonresident Income Tax Agreement, Form 12N. Importantly, Form 14N is aimed at nonresident individuals, including nonresident grantors of a grantor trust, and should not be filed for entities other than individuals.

Form 14N, along with the appropriate payment for the withheld tax, must be submitted to the Nebraska Department of Revenue at the same time as the organization's Nebraska income tax return. Specifically, it should be sent to P.O. Box 98911, Lincoln, Nebraska 68509-8911. Additionally, it is the responsibility of the filing entity to furnish each nonresident individual, for whom income tax was withheld, with a copy of the completed Form 14N. This step ensures that nonresident individuals can correctly report and claim the withheld tax on their Nebraska Individual Income Tax Return, Form 1040N.

The withholding rate for income subject to Form 14N is established at 6.84% of the income that is deemed taxable under Nebraska state law. This determination is made using one of three schedules, depending on the type of organization: Schedule II, Column E, of Form 1041N for trusts and estates; Schedule III, Column E, of Form 1065N for partnerships; or Schedule III, Column E, of Form 1120-SN for S corporations. The total amount withheld, as recorded on line 2 across all Form 14Ns filed by the entity, should match the sum reported on the respective tax return of the organization.

Nonresident individuals who have had Nebraska income tax withheld by an entity must file the Nebraska Individual Income Tax Return, Form 1040N. When doing so, they should claim the amount withheld, as reported on Form 14N, as a credit against their Nebraska income tax liability. A copy of Form 14N received from the entity should be attached to Form 1040N in the designated area for attaching the Wage and Tax Statement, Federal Form W-2. For those filing electronically, Form 8453N should be used to transmit Form 14N to the Nebraska Department of Revenue. It's crucial for nonresidents to understand that they are not required to file Form 1040N if their only Nebraska income derives from business activities of the withholding entity and taxes have been fully withheld on all Nebraska income attributable to them. Nonresidents facing this scenario may choose to forfeit filing a Form 1040N, thereby allowing the full amount of the withholding to remain with the Nebraska Department of Revenue.

Filling out tax forms can be daunting, especially when dealing with specifics for nonresident individuals, such as the Nebraska 14N form. Being meticulous in completing this form is crucial to avoid common pitfalls. Let's navigate together through some of the most frequent mistakes made when handling this document to ensure your submissions are error-free and smooth.

Incorrect Identification Numbers: One of the initial steps in filling out the form is to accurately provide identification numbers, both for the organization and the nonresident individual. Misplaced digits or outright wrong numbers can lead to processing delays or mismatches in the tax system. It's essential to double-check these fields to ensure the Nebraska and federal identification numbers, as well as social security numbers, are correct. Pay special attention to the spouse’s social security number, if applicable, as it's often overlooked.

While the list above covers common mishaps, attention to detail in every section of Form 14N is fundamental. Careful reading of the instructions, double-checking figures and information, and consulting with a tax professional if uncertainty arises, can significantly reduce errors. Remember, accurate and complete submissions not only comply with tax laws but also streamline the process for everyone involved.

When working with the Nebraska 14N form, a statement of Nebraska income tax withheld for nonresident individuals, it's not uncommon to encounter additional forms and documents that need to be filed alongside it. Each of these documents serves a specific purpose in the tax filing process, ensuring that nonresident individuals comply with Nebraska tax laws correctly.

Each of these forms plays a vital role in ensuring tax compliance for nonresident individuals and entities operating within Nebraska. Proper completion and submission of these documents, in conjunction with the Form 14N, streamline the tax filing process and ensure accuracy in reporting income and withholding taxes. It's crucial for nonresident individuals and entities to familiarize themselves with these forms to fulfill their tax obligations efficiently.

The Nebraska 14N form is similar to the Federal Form 1040NR in various ways. Both are designed primarily for nonresident individuals, focusing on income generated within the jurisdiction—Nebraska for the 14N and the United States for the 1040NR. These forms calculate the tax liability based on earnings within the respective areas and offer a structure for withholding tax. However, while the 14N is specific to the state's tax requirements and is used alongside other state forms, the 1040NR serves nonresidents dealing with federal tax obligations. The core similarity lies in their purpose to determine the tax duties of nonresidents, ensuring they pay the appropriate amount on income derived from within the territory.

Aside from the Federal Form 1040NR, the Nebraska 14N form also shares characteristics with Form W-2. Although the W-2 is an employment-related document detailing wages paid to employees and taxes withheld by employers, it similarly requires the reporting of income and tax withholdings. In essence, the Form W-2 is utilized to report wages on a federal level, whereas the Form 14N is applied for reporting withholding on income for nonresident individuals in Nebraska. The comparable aspect of these documents is their role in reporting income and taxes withheld, essential for filing personal income tax returns both at the federal and state level.

When preparing the Nebraska 14N form, it is crucial to follow specific guidelines to ensure accuracy and compliance with the Nebraska Department of Revenue's requirements. Here are several dos and don'ts to keep in mind:

By following these guidelines, you can help ensure that the Nebraska 14N form is filled out correctly and efficiently, reducing the chance of errors and ensuring compliance with Nebraska's tax withholding requirements for nonresident individuals.

There are several common misconceptions about the Nebraska 14N form, which is essential for accurately reporting income tax withheld for nonresident individuals. Understanding these can help in correctly completing and filing the form.

Clearing up these misconceptions can help individuals and organizations involved navigate the complexities of tax withholding and reporting for nonresidents in Nebraska, ensuring compliance and reducing the likelihood of errors when dealing with state income tax obligations.

Understanding how to properly fill out and make use of the Nebraska 14N form is essential for entities such as estates, trusts, S corporations, partnerships not publicly traded, and limited liability companies that have nonresident individual beneficiaries, partners, members, or shareholders. Here are key takeaways for those who are tasked with this responsibility:

Adherence to these guidelines ensures compliance with Nebraska’s tax withholding requirements for nonresident individuals and helps avoid potential issues with the Nebraska Department of Revenue.

Nebraska Sales Tax Login - Equipped with detailed instructions on completing Schedule I for accurate local tax reporting.

Can You Have Blue Lights on Your Car - Critical for anyone looking to satisfy Nebraska regulations for vehicles requiring red light installation.

Nebraska 1040n - Secure your rights and interests in tax proceedings by designating representatives through Nebraska's Form 33.