Fill a Valid Nebraska 2210N Form

Fill a Valid Nebraska 2210N Form

The Nebraska 2210N form, a pivotal document for individuals navigating the intricacies of tax obligations, serves as a testament to the government's mechanism for managing underpayments of estimated taxes. This form, attached to Form 1040N, delves deep into the financial responsibilities of taxpayers, ensuring that their payments align with the expected income tax after accounting for nonrefundable credits, with a detailed process outlined for calculating penalties on underpayments. The stakes are high as taxpayers who fall short of their estimated tax payments or those with inadequate state income tax withholdings are faced with potential penalties, adding a layer of complexity to tax management. Notably, the form encompasses provisions for special circumstances that could exempt taxpayers from penalties, ranging from demonstrating the impact of casual, disaster, or other unusual circumstances to considerations for retirees over 62 or those who became disabled. Furthermore, individuals involved in farming, ranching, or fishing enjoy specific guidelines that could exempt them from penalties, underscoring the form's comprehensive approach to addressing varied taxpayer situations. Moreover, clear instructions accompany each section of the form, guiding taxpayers through calculating underpayments and penalties, while outlining the conditions under which the penalties can be waived, thereby demystifying the often complex process of tax payment and penalty assessment.

|

|

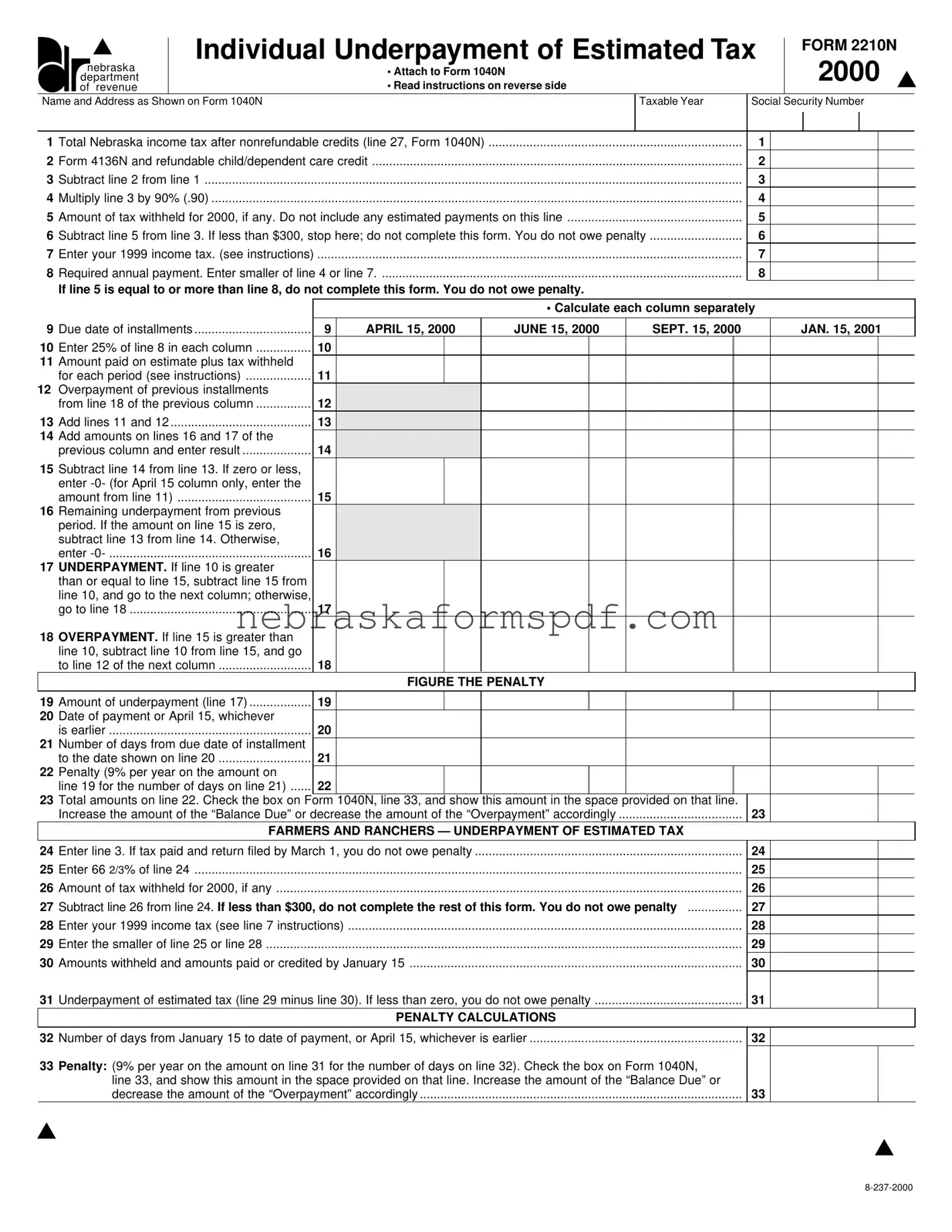

Individual Underpayment of Estimated Tax |

|

|

FORM 2210N |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

||||

|

nebraska |

|

|

|

• Attach to Form 1040N |

|

|

|

|

|

2000 |

|||

|

department |

|

|

|

|

|

|

|

|

|||||

|

|

|

|

• Read instructions on reverse side |

|

|

|

|

||||||

|

of revenue |

|

|

|

|

|

|

|

|

|

|

|

||

Name and Address as Shown on Form 1040N |

|

|

|

Taxable Year |

Social Security Number |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1 |

Total Nebraska income tax after nonrefundable credits (line 27, Form 1040N) |

|

|

1 |

|

|

|

|

|

|||||

2 |

............................................................................................................Form 4136N and refundable child/dependent care credit |

|

|

2 |

|

|

|

|

|

|||||

3 |

.............................................................................................................................................................Subtract line 2 from line 1 |

|

|

|

|

3 |

|

|

|

|

|

|||

4 |

...........................................................................................................................................................Multiply line 3 by 90% (.90) |

|

|

|

|

4 |

|

|

|

|

|

|||

5 |

...................................................Amount of tax withheld for 2000, if any. Do not include any estimated payments on this line |

|

|

5 |

|

|

|

|

|

|||||

6 |

...........................Subtract line 5 from line 3. If less than $300, stop here; do not complete this form. You do not owe penalty |

|

6 |

|

|

|

|

|

||||||

7 |

Enter your 1999 income tax. (see instructions) |

............................................................................................................................ |

|

|

|

7 |

|

|

|

|

|

|||

8 |

. ..........................................................................................................Required annual payment. Enter smaller of line 4 or line 7 |

|

|

8 |

|

|

|

|

|

|||||

|

If line 5 is equal to or more than line 8, do not complete this form. You do not owe penalty. |

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

• Calculate each column separately |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

||||

9 |

Due date of installments |

|

9 |

APRIL 15, 2000 |

JUNE 15, 2000 |

SEPT. 15, 2000 |

|

|

|

JAN. 15, 2001 |

||||

10 |

Enter 25% of line 8 in each column |

10 |

|

|

|

|

|

|

|

|

|

|

||

11Amount paid on estimate plus tax withheld

for each period (see instructions) |

11 |

12Overpayment of previous installments

from line 18 of the previous column |

12 |

13 Add lines 11 and 12 |

13 |

14Add amounts on lines 16 and 17 of the

previous column and enter result |

14 |

15Subtract line 14 from line 13. If zero or less, enter

amount from line 11) |

15 |

16 Remaining underpayment from previous |

|

period. If the amount on line 15 is zero, |

|

subtract line 13 from line 14. Otherwise, |

|

enter |

16 |

17UNDERPAYMENT. If line 10 is greater

than or equal to line 15, subtract line 15 from line 10, and go to the next column; otherwise,

go to line 18 |

17 |

18OVERPAYMENT. If line 15 is greater than line 10, subtract line 10 from line 15, and go

to line 12 of the next column |

18 |

|

FIGURE THE PENALTY |

19 Amount of underpayment (line 17) |

19 |

20Date of payment or April 15, whichever

is earlier |

20 |

21Number of days from due date of installment

to the date shown on line 20 |

21 |

22 Penalty (9% per year on the amount on |

|

line 19 for the number of days on line 21) |

22 |

23Total amounts on line 22. Check the box on Form 1040N, line 33, and show this amount in the space provided on that line.

|

Increase the amount of the “Balance Due” or decrease the amount of the “Overpayment” accordingly |

23 |

|

FARMERS AND RANCHERS — UNDERPAYMENT OF ESTIMATED TAX |

|

24 |

Enter line 3. If tax paid and return filed by March 1, you do not owe penalty |

24 |

25 |

Enter 66 2/3% of line 24 |

25 |

26 |

Amount of tax withheld for 2000, if any |

26 |

27 |

Subtract line 26 from line 24. If less than $300, do not complete the rest of this form. You do not owe penalty |

27 |

28 |

Enter your 1999 income tax (see line 7 instructions) |

28 |

29 |

Enter the smaller of line 25 or line 28 |

29 |

30 |

Amounts withheld and amounts paid or credited by January 15 |

30 |

31 |

Underpayment of estimated tax (line 29 minus line 30). If less than zero, you do not owe penalty |

31 |

|

PENALTY CALCULATIONS |

|

32 |

Number of days from January 15 to date of payment, or April 15, whichever is earlier |

32 |

33Penalty: (9% per year on the amount on line 31 for the number of days on line 32). Check the box on Form 1040N, line 33, and show this amount in the space provided on that line. Increase the amount of the “Balance Due” or

decrease the amount of the “Overpayment” accordingly |

33 |

INSTRUCTIONS

WHO MUST FILE. Individuals who determine on line 17 of this form that their Nebraska individual income tax was not sufficiently paid at any time throughout the year must file Individual Underpayment of Estimated Tax, Form 2210N, to calculate the amount of penalty due.

WHO MUST PAY THE UNDERPAYMENT PENALTY. An individual who did not pay enough estimated tax by any of the due dates or who did not have enough state income tax withheld may be charged a penalty. This is true even if you are due a refund when you file your tax return. The penalty is figured separately for each due date. Therefore, you may owe the penalty for an earlier payment due, even if you paid enough tax later to make up the underpayment.

In general, you may owe the penalty for 2000 if you did not pay at least the smaller of:

1.90% of your 2000 tax liability; or

2.100% of your 1999 tax liability (if you filed a 1999 return that covered a full 12 months).

EXCEPTIONS TO THE PENALTY. You will not have to pay the penalty if either 1 or 2 applies:

1.You had no tax liability for 1999 , you were a U.S. citizen or resident for the entire year, and your 1999 Nebraska tax return was (or would have been had you been required to file) for a full 12 months.

2.The total tax shown on your 2000 return minus the amount of tax you paid through withholding is less than $300. To determine whether the total tax is less than $300, complete lines

Nebraska Tax on Annualized Income. No penalty will be imposed if your Nebraska tax payments equal or exceed 90% of the Nebraska tax for a Nebraska tax liability based on annualized income earned through the end of the month preceding the installment date. Attach a separate schedule showing your computation similar to the federal Annualized Income Installment Method Schedule.

Other Circumstances. Attach a statement to this form outlining why the penalty should not be imposed. This would include an underpayment due to casualty, disaster, or other unusual circumstance where it would be inequitable to impose the penalty. Penalty may also be waived if in 1999 or 2000, you retired after age 62 or became disabled, and your underpayment was due to reasonable cause. Attach a statement if this circumstance applies to you.

WHEN AND WHERE TO FILE. Form 2210N must be attached and filed with the Nebraska Individual Income Tax Return, Form 1040N.

SPECIFIC LINE INSTRUCTIONS

LINE 7, 1999 TAX. Use your 1999 tax after nonrefundable credits from your 1999 tax return. If the 1999 tax year was for less than 12 months, do not complete this line. Instead, enter the amount from line 4 on line 8 and complete the remainder

of the form. If federal adjusted gross income in 1999 was more than $150,000 ($75,000 – married separate), enter 108.6% of your 1999 taxes on line 7.

LINE 9, INSTALLMENT PAYMENTS. If you filed your Nebraska income tax return and paid the balance of the tax due by January 31, that balance is considered paid as of January 15.

Fiscal Year Taxpayers. The installment due dates for fiscal year taxpayers are the 15th day of the following months: the first month of the second quarter, the third month of the second quarter, the third month of the third quarter, and the first month of the following fiscal year. All dates on Form 2210N are to be considered in the corresponding month of the fiscal year.

LINE 11, TAX WITHHELD. An equal part of the Nebraska income tax withheld during the year by your employer is considered paid on each required installment date unless you establish the dates on which withholding occurred and consider such withholding as paid on the dates when actually withheld.

For nonresident individuals, the amount of tax withheld by S corporations, partnerships, limited liability companies, or fiduciaries shall be considered paid on the last day of the organization’s taxable year unless you establish the dates on which all amounts were actually withheld and consider such withholding as paid on the dates when actually withheld.

LINE 18, OVERPAYMENT. Any overpayment of an installment on line 18 in excess of all prior underpayments should be applied as a credit on line 12 against the next installment.

LINES

19.If the payment applied is less than the underpayment, make separate penalty calculations through the date of payment and for the remaining underpayment through the date it is paid, then add the results together and enter on line

22.See the instructions for Federal Form 2210 for more information. The penalty is calculated at 9% per annum for all installments.

SPECIAL RULES FOR FARMERS AND RANCHERS. If your gross income from farming, ranching, or fishing is at least

1.How to Figure Your Underpayment. If the gross income test was met but the date for filing and payment of the tax was not, complete lines 24 through 31. If no underpayment is indicated on line 31, do not complete lines 32 and 33.

2.Penalty Calculation. Complete lines 32 and 33 to determine the amount of the penalty which is calculated at 9%.

| Fact Number | Description |

|---|---|

| 1 | The Nebraska Form 2210N is used for calculating the penalty for underpayment of estimated tax by individuals. |

| 2 | This form must be attached to the Nebraska Individual Income Tax Return, Form 1040N. |

| 3 | Penalties are determined separately for each installment due date, which means taxpayers may owe penalties for any payment period where insufficient taxes were paid. |

| 4 | No penalty is imposed if the total tax shown on the 2000 return minus the amount paid through withholding is less than $300. |

| 5 | The penalty rate is 9% per annum, applied to the underpayment amount for the number of days the underpayment remains unpaid. |

| 6 | Special rules apply to farmers and ranchers. If over two-thirds of annual gross income is from farming, ranching, or fishing, and taxes are paid by March 1, penalties for underpayment of estimated tax may be waived. |

| 7 | The form requires details such as total Nebraska income tax after credits, amount of tax withheld, estimated tax payments made, and addresses reasons for any penalties not to be imposed. |

Filing the Nebraska 2210N form is a step that should be taken with close attention to detail. This form is utilized to evaluate and calculate any penalties due to the underpayment of estimated taxes throughout the year. When navigating through this process, it is crucial to gather all necessary financial documents beforehand to ensure accuracy and compliance with Nebraska state tax regulations. Here's how to systematically fill out the form:

Once you have completed the necessary calculations and filled out the form accurately, attach Form 2210N to your Nebraska Individual Income Tax Return, Form 1040N. Ensure that all information provided is accurate and complete to the best of your knowledge to avoid any possible discrepancies or additional penalties. Remember, this form is essential for those who have underpaid their estimated taxes and can help in identifying any potential penalties that may be owed to the Nebraska Department of Revenue.

The Nebraska Form 221 of Estimated Tax is designed for individuals who discover they have not paid enough tax through withholding or estimated tax payments. If upon completing line 17 of the form it's clear that the individual's Nebraska income tax was underpaid at any point during the year, filing this form is a requirement to compute the penalty owed. This scenario is typical for people who either did not make estimated tax payments when needed or whose withholding taxes were insufficient.

Yes, there are exceptions where you're not liable to pay the underpayment penalty:

Installment payments are due quarterly, and an equal portion of the Nebraska income tax withheld throughout the year is considered paid on each due date unless specific withholding dates are established. For nonresident individuals, taxes withheld by certain entities are deemed paid on the last day of the entity’s tax year, unless specific withholding dates are proven otherwise. Overpayments from a previous installment should be credited towards the next installment due.

Special provisions are in place for individuals whose main source of income is from farming, ranching, or fishing. If at least two-thirds of your total annual gross income comes from these sources in either 1999 or 2000, and you file Form 1040N and pay the Nebraska income tax by March 1, you are exempt from the penalty for underpayment of the estimated tax. This exception relieves such individuals from having to file Form 2210N, under the condition that no underpayment is indicated after completing the form up to line 31.

When filing the Nebraska 2210N form, also known as the Individual Underpayment of Estimated Tax form, people often make a series of common mistakes. These errors can lead to inaccuracies in the calculation of penalties owed, potentially resulting in either overpayment or underpayment of taxes. Understanding these mistakes is crucial for accurate completion and submission.

One of the first errors involves misunderstanding the prerequisites for filing the form. Individuals sometimes fill out the 2210N without realizing that it is not required if their underpayment of estimated tax is less than $300, as the penalties for underpayment would not apply in such scenarios. This mistake can lead to unnecessary paperwork and confusion.

Another area where mistakes frequently occur is in the calculation of the required annual payment on line 8. Individuals often incorrectly choose the larger number between line 4 (90% of current year tax) and line 7 (the previous year's tax) instead of the correct smaller number, which can lead to an incorrect calculation of underpayments or overpayments.

Individuals also commonly input incorrect values or leave blank the sections related to tax withheld and estimated payments made during the year on lines 5 and 11, respectively. This oversight can result in inaccuracies in determining if an underpayment occurred for each period.

Here is a list of nine common mistakes made on the Nebraska 2210N form:

To avoid these mistakes, individuals are advised to carefully read the instructions provided with the form and double-check their calculations. Seeking assistance from a tax professional can also help in navigating the complexities of this form. It's essential to ensure all information is accurate and complete before submission to avoid potential penalties or the need to amend the form later.

When it comes to managing your taxes, especially if you're trying to figure out your individual underpayment of estimated tax with the Nebraska 2210N form, there are several other forms and documents you might find yourself working with. Knowing what each of these forms is for can simplify the process and ensure you have everything in order for your tax submissions.

Managing your taxes involves a lot of paperwork, and each document serves its unique purpose. From reporting your income on Form 1040N to making adjustments with schedules and requesting credits, each form ensures your taxes are accurate and benefits are maximized. Keep these forms in mind as you navigate your tax responsibilities, and remember, staying organized is key to handling your taxes efficiently.

The Nebraska 2210N form is similar to several other documents used for tax purposes, each with its own specific focus but sharing common elements in their structure and purpose. For example, the Internal Revenue Service (IRS) Form 2210, "Underpayment of Estimated Tax by Individuals, Estates, and Trusts," mirrors the objective of the Nebraska 2210N form. Both forms are designed to calculate penalties for underpayment of estimated tax. The structure encompasses sections for the taxpayer's information, calculation of the underpayment, determination of the penalty, and specific conditions that might waive the penalty. They similarly require the taxpayer to detail income, tax liability, and payments made throughout the tax year to assess any shortfall in estimated tax payments.

Another document resembling the Nebraska 2210F is the Form 1040-ES, "Estimated Tax for Individuals." While 1040-ES focuses on helping taxpayers figure out their estimated taxes for the upcoming year, the Nebraska 2210N form addresses the penalty for not accurately paying estimated tax in the past year. However, both forms involve a detailed analysis of the taxpayer’s income, deductions, and credits to estimate the tax owed. The connection lies in their mutual aid to taxpayers in managing their estimated tax payments to avoid underpayment penalties. The resemblance is in their shared goal of ensuring that taxpayers properly anticipate and pay their taxes due throughout the year.

Somewhat similarly, the Nebraska Form 1040N, the state's individual income tax return, also shares important connections with the Nebraska 2210N form. The 1040N form is where taxpayers calculate their total tax liability for the year based on their Nebraska income. Importantly, the results from Form 1040N, particularly the total tax liability figure, are required for completing the Nebraska 2210N. The tie between these documents is direct as the 2210N form calculates the penalty based on underpayment relative to the tax liability determined on the Form 1040N. This direct link underscores the importance of accuracy and timeliness in tax payments, showing how multiple forms work together to navigate the complex territory of tax obligations.

When it comes to filling out the Nebraska 2210N form, it’s crucial to approach the task with careful attention to detail. Known officially as the Individual Underpayment of Estimated Tax form, it’s designed for those who have not paid sufficient estimated taxes throughout the year. To ensure you navigate this process smoothly, here are a few dos and don’ts:

By adhering to these guidelines, taxpayers can navigate the complexities of the 2210N form more effectively, ensuring accuracy and compliance with Nebraska’s tax regulations. Always consider consulting a tax professional if you find yourself unsure or overwhelmed by the process.

Misunderstandings about the Nebraska 2210N form can lead to confusion. Here's a breakdown aimed at clearing up some of these misconceptions:

Understanding these key points about the Nebraska 2210N can help prevent misconceptions and ensure compliance with state tax laws.

Understanding the Nebraska 2210N Form is crucial for those who have underpaid their estimated taxes. Here's what you need to know to navigate this process effectively:

Filling out the Form 2210N accurately is key to correctly determining any underpayment penalties. Take the time to understand each section, consult the instructions provided, and consider seeking professional advice if your situation is complex. This proactive approach can help you avoid unnecessary penalties and ensure compliance with Nebraska tax laws.

Nebraska Filing Requirements - Form 12N serves as a commitment by nonresidents to file a Nebraska Individual Income Tax Return and pay any due taxes, specifically relating to income earned from Nebraska entities.

Nebraska Form 6 - Highlights the importance of accurate tax reporting to avoid severe penalties, including a Class IV felony for fraudulent statements.