Fill a Valid Nebraska 33 Form

Fill a Valid Nebraska 33 Form

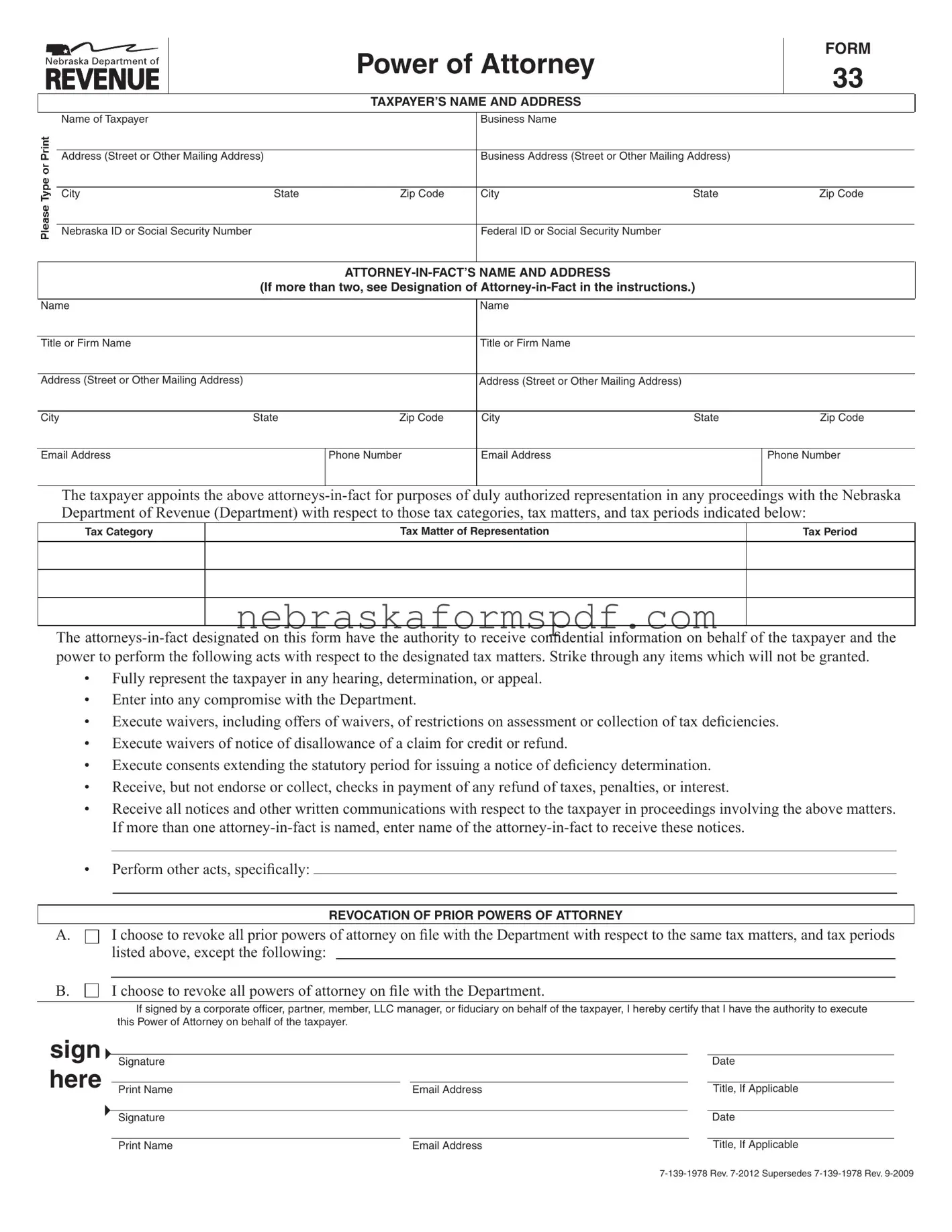

Understanding the essentials of the Nebraska 33 Form, or Power of Attorney (POA), is crucial for anyone dealing with tax representation matters in the state. This comprehensive form serves as a pivotal tool for taxpayers aiming to authorize a representative to act on their behalf in proceedings with the Nebraska Department of Revenue. Essentially, it allows designated attorneys-in-fact to receive confidential information, and engage in a variety of actions, including negotiating compromises and executing waivers related to tax assessment, penalty abatements, and refunds. The form demands detailed information about the taxpayer and the attorney-in-fact, including names, addresses, and respective identification numbers. A thoughtful provision also enables the taxpayer to specify the extent of the representation, allowing for the delineation of tax categories, matters of representation, and relevant tax periods. Furthermore, the form includes options to revoke previous POAs, presenting a clear process for taxpayers to update or change their designated representatives as necessary. This form not only outlines the legal framework for representation but also emphasizes the seriousness with which the Department treats such delegations, underlining the responsibilities bestowed upon the appointed attorneys-in-fact and the trust placed in them by taxpayers. In reviewing these facets, the Nebraska 33 Form emerges as a vital instrument for ensuring proper representation and handling of tax-related matters in Nebraska, highlighting the importance of accuracy, clarity, and discretion in its completion and submission.

Power of Attorney

FORM

33

TAXPAYER’S NAME AND ADDRESS

Name of Taxpayer

Business Name

Address (Street or Other Mailing Address)

Business Address (Street or Other Mailing Address)

City |

State |

Zip Code |

City |

State |

Zip Code |

Nebraska ID or Social Security Number

Federal ID or Social Security Number

(If more than two, see Designation of

Name |

|

|

Name |

|

|

|

|

|

|

|

|

Title or Firm Name |

|

|

Title or Firm Name |

|

|

|

|

|

|

|

|

Address (Street or Other Mailing Address) |

|

|

Address (Street or Other Mailing Address) |

|

|

|

|

|

|

|

|

City |

State |

Zip Code |

City |

State |

Zip Code |

|

|

|

|

|

|

Email Address |

|

Phone Number |

Email Address |

|

Phone Number |

The taxpayer appoints the above

Tax Category

Tax Matter of Representation

Tax Period

The

•Fully represent the taxpayer in any hearing, determination, or appeal.

•Enter into any compromise with the Department.

•Execute waivers, including offers of waivers, of restrictions on assessment or collection of tax deiciencies.

•Execute waivers of notice of disallowance of a claim for credit or refund.

•Execute consents extending the statutory period for issuing a notice of deiciency determination.

•Receive, but not endorse or collect, checks in payment of any refund of taxes, penalties, or interest.

•Receive all notices and other written communications with respect to the taxpayer in proceedings involving the above matters. If more than one

•Perform other acts, speciically:

REVOCATION OF PRIOR POWERS OF ATTORNEY

A.

B.

I choose to revoke all prior powers of attorney on ile with the Department with respect to the same tax matters, and tax periods listed above, except the following:

I choose to revoke all powers of attorney on ile with the Department.

If signed by a corporate officer, partner, member, LLC manager, or fiduciary on behalf of the taxpayer, I hereby certify that I have the authority to execute this Power of Attorney on behalf of the taxpayer.

sign  here

here

Signature |

|

|

Date |

||

|

|

|

|

|

|

|

|

|

|

|

|

Print Name |

|

Email Address |

Title, If Applicable |

||

|

|||||

|

|

|

|

|

|

Signature |

|

|

Date |

||

|

|

|

|

||

|

|

|

|

|

|

Print Name |

|

|

Email Address |

Title, If Applicable |

|

|

|||||

INSTRUCTIONS

WHO MUST FILE. Any taxpayer who wishes to secure representation by another party in matters before the Nebraska Department of Revenue (Department) with regard to any tax imposed by the tax laws of the State of Nebraska, must ile a Power of Attorney (POA), Form 33. A Form 33 authorizes that party to receive conidential tax information regarding the taxpayer. This form is provided for the taxpayer’s convenience in designating a POA, but it is not the sole form which may be used. The Department will honor all other properly completed and signed POA authorizations.

WHEN AND WHERE TO FILE. The completed Form 33 may be iled any time. This form, or another properly completed and signed POA, must be iled with the Department before any person designated can represent the taxpayer in matters involving disclosure of conidential tax information.

This form, or other appropriate POA, may be scanned and emailed, faxed, or mailed to the Department:

•Email to rev.poa@nebraska.gov;

•Fax to

•Mail to the Nebraska Department of Revenue, PO Box 94818, Lincoln, NE

TAXPAYER’S NAME AND ADDRESS. If the taxpayer is an individual, a Social Security number must be listed. If a married, iling jointly return was iled, enter both spouses’ Social Security numbers in the spaces provided.

If the taxpayer is a corporation, partnership, or association, enter the name, state and federal ID numbers (if applicable), and the business address. If the Form 33 will be used in a tax matter in the case of a partnership for which the names, addresses, and Social Security numbers or ID numbers have not already been furnished to the Department, these items should be listed on an attached sheet.

If the taxpayer is an estate or trust, enter the name, title, and address of the iduciary, as well as the name and ID number or Social Security number of the taxpayer. If this space is used to list other information, clearly label the change.

DESIGNATION OF

TAX CATEGORY, TAX MATTER, AND TAX PERIOD. Form 33 is designed to clearly express the scope of the authority granted by the taxpayer to any

“Tax Category” requires a list of the type of tax, such as “income” or “sales and use.” “Tax Matter of Representation” requires a brief summary of the subjects for which the

AUTHORIZED ACTS. The Form 33 lists several acts which can be performed by the

not wish to authorize the named

particular act which is listed, the taxpayer must strike through the power which is not granted. This is particularly important with respect to correspondence from the Department to the taxpayer regarding the designated tax matters. If the taxpayer wants to receive refund claim approvals or denials, and other notices and written communications, rather than have the

If the taxpayer wishes to authorize an act which is not listed, a concise and speciic statement about the additional authorization must be made in the space provided, or a separate signed statement may be attached to the Form 33.

REVOCATION OF PRIOR POWERS OF ATTORNEY. To revoke any POAs previously iled with the Department, choose Box A or B.

Box A. Checking this box allows the taxpayer the option of revoking all POAs on ile with the Department with the exception of those listed on the lines provided (or on a list attached to the Form 33). Check box A and list the names, addresses, and zip codes of the

Box B. Checking this box revokes all POAs previously iled with the Department. Check Box B, and sign the form.

If no boxes are checked, all prior POAs will remain in force.

SIGNATURE. The taxpayer must sign and date the form. If spouses ile a married, iling jointly income tax return, which both have signed, then both spouses must sign the Form 33. If only one spouse in a married couple signs Form 33, then a separate Form 33 must be signed by the other spouse. If there is only one spousal signature or a second POA is not signed, then only the person designated by the POA would be authorized to perform the acts authorized by the POA. The nonsigning spouse who has iled a joint return with his or her spouse may still obtain information about, and may discuss issues regarding, the couple’s joint return. However, a person may not authorize another party, or themselves, to receive conidential tax information regarding separate returns iled by the person’s spouse.

Only certain people may represent a taxpayer in a contested case once a hearing oficer is appointed: (1) the taxpayer; (2) a Nebraska attorney; or (3) a

If the taxpayer is a partnership, all partners must sign, unless one is duly authorized to act in the name of the partnership. Nebraska has adopted the Uniform Partnership Act of 1998 (Neb. Rev. Stat. §§

If the taxpayer is a corporation or an association, an oficer having authority to bind the entity must sign. The oficer must indicate his or her oficial title on the line provided.

If the taxpayer is a Nebraska limited liability company (LLC), all the members must sign, unless a manager is duly authorized to act in the name of the LLC. The validity of the authorizations made by a foreign LLC will be determined governed by the laws of the state in which the LLC was organized.

| Fact Name | Description |

|---|---|

| Purpose and Use | Form 33 is used by taxpayers to grant authority to another individual or firm to represent them in matters before the Nebraska Department of Revenue, specifically for tax matters. |

| Governing Law | The form is governed by the tax laws of the State of Nebraska and is recognized by the Nebraska Department of Revenue. |

| Filing Method | The form can be submitted via email, fax, or mail to the addresses and numbers provided by the Nebraska Department of Revenue. |

| Identification Requirements | Taxpayers must provide personal or business identification information, including Nebraska ID or Social Security Numbers and Federal ID for businesses. |

| Designation of Attorney-in-Fact | Form 33 allows for the designation of one or more attorneys-in-fact, granting them specified powers including receiving confidential tax information and representing the taxpayer in tax matters. |

| Revocation of Previous Powers | Taxpayers can choose to revoke all previously filed powers of attorney regarding the same tax matters and periods, except for those specifically listed on the form. |

| Authorized Acts | The form lists specific acts the attorney-in-fact can perform on behalf of the taxpayer, with an option to strike through any powers not granted. |

| Signature Requirements | Form 33 must be signed and dated by the taxpayer, with additional rules for spouses, partnerships, corporations, and LLCs as outlined in the form's instructions. |

Filing the Power of Attorney Form 33 is a critical step for taxpayers in Nebraska who need to authorize someone else to handle their tax matters with the Nebraska Department of Revenue. Whether it's dealing with tax assessments, compromises, refunds, or other tax-related issues, completing this form accurately ensures that the appointed person or entity has the legal authority to act on behalf of the taxpayer. Follow these steps carefully to ensure the form is properly filled out and submitted.

After submitting Form 33, the designated attorney-in-fact will have the authority to represent the taxpayer in dealings with the Nebraska Department of Revenue for the specified tax matters. This ensures that the taxpayer’s affairs are managed efficiently and effectively, allowing for peace of mind regarding tax issues.

The Nebraska 33 Form, also known as the Power of Attorney (POA) form, must be filed by any taxpayer seeking to designate another party to represent them in matters before the Nebraska Department of Revenue (Department). This includes both individuals and entities who wish to authorize another person to receive confidential tax information and act on their behalf for specific tax-related issues in Nebraska. Whether you're an individual, a corporation, a partnership, an estate, or a trust, you'll find this form essential when you need representation for tax matters with the Department.

Submitting Form 33 is quite straightforward. Taxpayers or their representatives have three options to file this form:

Through the Nebraska 74 Form, a taxpayer can grant their appointed attorney-in-fact a wide range of powers for managing tax matters, including but not limited to:

To revoke any previously filed Powers of Attorney (POAs) with the Nebraska Department of Revenue, the Form 33 offers two options:

Filling out Form 33 in Nebraska, which grants power of attorney for tax representation, involves careful attention to detail. Common mistakes can hinder the process, affecting the taxpayer's representation. Understanding these mistakes is crucial for a correct and efficient completion of the form.

Firstly, a frequent error is providing incomplete or incorrect taxpayer information, including the taxpayer’s name, address, and identification numbers. It's essential to double-check these details for accuracy, as they establish the identity of the person granting the power of attorney.

In conclusion, when filling out the Nebraska Form 33 for granting power of attorney for tax purposes, attention to detail is paramount. Common errors, such as incomplete information and failure to specify or revoke authority accurately, can significantly impact the effectiveness of tax representation. Taxpayers are encouraged to review their forms carefully and ensure all required information is correct and complete. Understanding and avoiding these common mistakes is key to a smoother, more efficient process.

When dealing with legal and tax matters, it's essential to be well-prepared with the right documentation. In addition to the Nebraska Form 33, Power of Attorney, which authorizes representation before the Nebraska Department of Revenue, there are various other forms and documents often used to ensure thorough and compliant tax handling. Understanding these documents can significantly streamline tax-related procedures and assist in maintaining accuracy and legality in financial affairs.

Understanding and correctly utilizing these forms can be pivotal for individuals and businesses in navigating Nebraska's tax laws effectively. Each document serves a unique purpose in the tax preparation and filing process, contributing to a comprehensive tax strategy that minimizes liabilities and leverages potential benefits. For further assistance, consider consulting with a tax professional or attorney who specializes in Nebraska tax law.

The Nebraska 33 form is similar to other types of power of attorney (POA) forms that are used across various states and for different purposes. While the content and structure may bear similarities, the specific use and legal standing of each form can vary depending on its purpose and the jurisdiction under which it operates. For instance, a general power of attorney form grants broad powers to an agent to act on the principal's behalf in various matters, while the Nebraska 33 form specifically authorizes representation and actions concerning tax matters before the Nebraska Department of Revenue.

Similar to the Nebraska 33 form, the IRS Form 2848, Power of Attorney and Declaration of Representative, is used for tax matters, but at the federal level. Both forms authorize an individual or entity to represent the taxpayer in front of the respective tax authority and to receive confidential information. However, the IRS Form 2848 is broader in scope, applicable for all tax types and issues at the federal level, while the Nebraska 33 is state-specific. Despite these differences, the core function of allowing taxpayer representation remains a fundamental similarity.

Another document akin to the Nebraska 33 form is the Durable Power of Attorney, which is primarily utilized for financial matters. While the durable form can encompass a wide range of authorities, including tax-related decisions, it is much broader and not limited to tax matters alone. The durable power of attorney remains effective even if the principal becomes incapacitated. In contrast, the Nebraska 33 form is narrowly focused on tax representation before the Nebraska Department of Revenue and does not extend its power if the principal faces incapacity, highlighting its more specialized nature.

When completing the Nebraska Power of Attorney Form 33, it's crucial to adhere to specific guidelines to ensure the process is done correctly and efficiently. Here is a list of dos and don’ts:

When dealing with the Nebraska 33 form, several misconceptions can lead to confusion and potential missteps. Understanding these misconceptions is crucial for taxpayers and their representatives to ensure accurate and effective use of this form. Below are seven common misconceptions about the Nebraska 33 form and explanations to clarify them:

Understanding these misconceptions ensures taxpayers can accurately complete and use the Nebraska 33 form for their representation needs before the Nebraska Department of Revenue. Properly appointing an attorney-in-fact and clarifying the scope of their authority avoids unnecessary complications in managing tax matters.

Filling out and using the Nebraska 33 form, also known as the Power of Attorney (POA) form, involves a few key takeaways to ensure it is completed correctly and achieves the intended purpose. This form is a legal document that allows a taxpayer to authorize another person to handle their tax matters with the Nebraska Department of Revenue. Understanding the essential aspects of the form can aid in a smoother process and legal compliance.

When filling out and filing the Nebraska 33 form, it's also essential for the correct individuals to sign the document to validate it. Depending on the taxpayer's status, this could mean signatures from individuals, partners, corporate officers, or LLC members. Making sure the form is properly signed according to the taxpayer's legal status ensures the POA is legally binding and acknowledged by the Nebraska Department of Revenue.

Nebraska Form 33 - Individuals who did not pay or withhold enough state income tax by the due dates might need to complete this form.

Or Title Application - Successful completion and approval of the DLB-1A form is a key step in establishing a vehicle dealership in Nebraska.