Fill a Valid Nebraska 451 Form

Fill a Valid Nebraska 451 Form

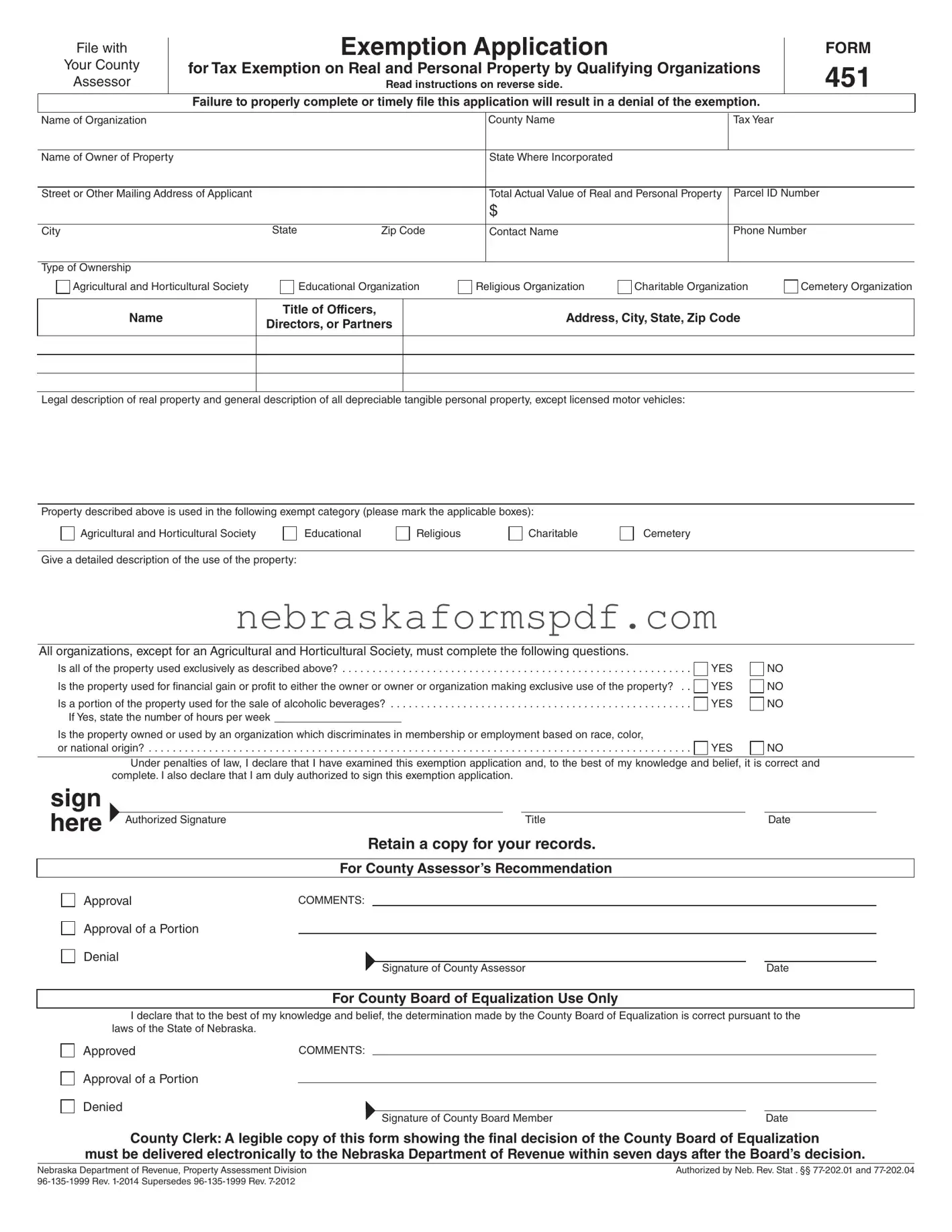

In navigating the intricate landscape of property taxes within Nebraska, organizations seeking exemption will find the FORM 451 to be a critical document, serving as the fulcrum for tax-related transactions impacting real and personal property. This document, officially titled the Exemption Application for Tax Exemption on Real and Personal Property by Qualifying Organizations, outlines the necessary steps and eligibility criteria for organizations aiming to secure a tax exemption. What stands out is the comprehensive nature of the form, catering to a wide array of organizations including, but not limited to, agricultural and horticultural societies, educational, religious, charitable, and cemetery organizations. It demands meticulous attention to detail in reporting, from the definition of property use to specific organizational information, such as the legal description of real property and a general description of all depreciable tangible personal property, excluding licensed motor vehicles. Moreover, the Form 451 underscores a strict adherence to deadlines, with a specific filing timeline that if not met, may result in a denial of the exemption, accentuating the urgency for timely compliance. Equally important, the form delves into issues of public interest such as nondiscrimination in membership or employment based on race, color, or national origin, hence, aligning tax exemption privileges with broader societal values. The procedural aspects concerning filing, penalties for late submissions, waivers, and the cycle of reaffirmation further articulate the nuanced requirements embedded within Nebraska’s property tax exemption process, marking the Form 451 as a key instrument in navigating the fiscal responsibilities of qualifying organizations.

File with |

|

|

|

Exemption Application |

|

|

FORM |

|

Your County |

|

for Tax Exemption on Real and Personal Property by Qualifying Organizations |

|

451 |

||||

Assessor |

|

|

||||||

|

|

|

Read instructions on reverse side. |

|

|

|||

|

|

Failure to properly complete or timely file this application will result in a denial of the exemption. |

|

|||||

|

|

|

|

|

|

|

|

|

Name of Organization |

|

|

|

County Name |

Tax Year |

|

||

|

|

|

|

|

|

|

|

|

Name of Owner of Property |

|

|

|

State Where Incorporated |

|

|

|

|

|

|

|

|

|

|

|||

Street or Other Mailing Address of Applicant |

|

|

Total Actual Value of Real and Personal Property |

Parcel ID Number |

|

|||

|

|

|

|

|

$ |

|

|

|

|

|

|

|

|

|

|

||

City |

|

State |

Zip Code |

Contact Name |

Phone Number |

|

||

|

|

|

|

|

|

|

|

|

Type of Ownership

Agricultural and Horticultural Society

Educational Organization

Religious Organization

Charitable Organization

Cemetery Organization

Name

Title of Officers,

Directors, or Partners

Address, City, State, Zip Code

Legal description of real property and general description of all depreciable tangible personal property, except licensed motor vehicles:

Property described above is used in the following exempt category (please mark the applicable boxes):

Agricultural and Horticultural Society |

|

Educational |

|

Religious |

|

Charitable |

Cemetery

Give a detailed description of the use of the property:

All organizations, except for an Agricultural and Horticultural Society, must complete the following questions.

Is all of the property used exclusively as described above? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Is the property used for financial gain or profit to either the owner or owner or organization making exclusive use of the property? . .

Is a portion of the property used for the sale of alcoholic beverages? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

If Yes, state the number of hours per week

Is the property owned or used by an organization which discriminates in membership or employment based on race, color,

or national origin? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

YES

YES

YES

YES

NO

NO

NO

NO

Under penalties of law, I declare that I have examined this exemption application and, to the best of my knowledge and belief, it is correct and complete. I also declare that I am duly authorized to sign this exemption application.

sign

|

|

|

|

|

|

|

|

|

|

|

here Authorized Signature |

|

|

|

|

Title |

|

Date |

|||

|

|

Retain a copy for your records. |

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

For County Assessor’s Recommendation |

|

|

|

|

||||

Approval |

COMMENTS: |

|

|

|

|

|

|

|

|

|

Approval of a Portion |

|

|

|

|

|

|

|

|

|

|

Denial |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Signature of County Assessor |

|

Date |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

For County Board of Equalization Use Only |

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

I declare that to the best of my knowledge and belief, the determination made by the County Board of Equalization is correct pursuant to the |

|||||||||

|

laws of the State of Nebraska. |

|

|

|

|

|

|

|

|

|

Approved |

COMMENTS: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Approval of a Portion |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Denied |

|

|

|

|

|

|

|

|

|

|

|

|

Signature of County Board Member |

|

Date |

||||||

|

|

|

|

|

||||||

County Clerk: A legible copy of this form showing the final decision of the County Board of Equalization

must be delivered electronically to the Nebraska Department of Revenue within seven days after the Board’s decision.

Nebraska Department of Revenue, Property Assessment Division |

Authorized by Neb. Rev. Stat . §§ |

|

Instructions

Who May File. An organization that owns real or depreciable tangible personal property, except licensed motor vehicles, and is seeking a property tax exemption, must ile an Exemption Application for Tax Exemption on Real and Personal Property by Qualifying Organizations, Form 451, if:

1.The property is owned by and used exclusively for agricultural and horticultural societies; or

2.The property is:

a.Owned by educational, religious, charitable, or cemetery organizations, or any organization for the exclusive beneit of any educational, religious, charitable, or cemetery organization;

b.Used exclusively for educational, religious, charitable, or cemetery purposes;

c.Not owned or used for inancial gain or proit to either the owner or user;

d.Not used for the sale of alcoholic beverages for more than 20 hours per week; AND

e.Not owned or used by an organization which discriminates in membership or employment based on race, color, or national origin.

An organization must ile a Form 451 if new property is acquired, or if the property is converted to exempt use.

When and Where to File. The Form 451 must be iled on or before the December 31 immediately preceding the year for which the exemption is sought, with the county assessor of the county where the property is subject to tax.

Late Filings/Waivers. If an organization fails to ile a Form 451 on or before December 31, it may ile a Form 451 on or before June 30 with the county assessor. The organization or society must also ile a written request with the county board of equalization for a waiver, so that the county assessor may consider the application for exemption. The county board of equalization may grant the waiver upon inding that good cause exists for the failure to make application on or before December 31.

If the waiver is granted, the county assessor will examine the application and recommend to the county board of equalization whether the real property or tangible personal property should be taxable or exempt. The county assessor must assess a penalty against the organization in the amount of 10% of the tax that would have been assessed had the waiver been denied or $100, whichever is less, for each calendar month or fraction thereof for which the iling of the exemption application missed the December 31 deadline. The penalty may not be waived.

Property Acquired or Converted to Exempt Use. If property is acquired or converted to exempt use after January 1, the organization may ile an application for exemption on or before July 1 of the year the property was acquired or converted. If an organization, between July 1 and levy date (October 15), purchases property that has been granted a tax exemption, and the property continues to be qualiied for exemption, the purchasing organization must ile an application for exemption on or before November 15.

Taxable property acquired or converted after July 1 is not eligible for exemption that year. If an application is iled, it will be considered an application for exemption for the next year.

Intervening Years.After an exemption has been approved, a new application must be iled for every year evenly divisible by four. For the intervening years (those years not evenly divisible by four), the Statement of Reafirmation of Tax Exemption, Form 451A , must be iled on or before the December 31 immediately preceding the year for which the exemption is sought, except for real property of cemeteries.

Cemetery Organizations. Any real property exemption granted to a cemetery organization will remain in effect without reapplication, unless disqualiied by change of ownership or use. On or before August 1, the county assessor must annually review the ownership and use of all cemetery real property and report this review to the county board of equalization.

Appeal Procedures. In the event of disapproval of this application by the county board of equalization, an appeal may be iled with the Tax Equalization and Review Commission within 30 days of the inal decision.

Specific Instructions. Property tax exemptions are strictly construed, and it is the responsibility of the applicant to prove the property qualiies for an exemption.

If the property is used for more than one type of use, mark the appropriate blocks and give the approximate percentage of use under the classiication. Describe in detail the use of the property for which an exemption is sought. Explain any circumstances when the property may be used for taxable purposes. If additional space is needed, use a separate sheet of paper and attach a copy to each copy of this form.

The completed Form 451 must be retained by the county clerk after the county board of equalization action, with a legible copy forwarded electronically to the Department within seven days of the board’s decision. The county assessor may make copies for the county’s records.

| Fact Name | Description |

|---|---|

| Form Purpose | This form is used for applying for tax exemption on real and personal property by qualifying organizations in Nebraska. |

| Eligibility | Organizations eligible for applying include agricultural and horticultural societies, educational, religious, charitable, or cemetery organizations owning real or depreciable tangible personal property, excluding licensed motor vehicles. |

| Filing Deadline | The form must be filed by December 31 preceding the tax year for which exemption is sought. A late filing may be submitted until June 30 with a request for a waiver. |

| Governing Laws | The form and the process are authorized by Neb. Rev. Stat §§ 77-202.01 and 77-202.04. |

| Penalty for Late Filing | A penalty is assessed for late filings at 10% of the tax that would have been assessed or $100, whichever is less, per calendar month or fraction thereof. |

| Reapplication and Reaffirmation | After an exemption is approved, a new application must be filed every year evenly divisible by four. For intervening years, a Statement of Reaffirmation of Tax Exemption, Form 451A, must be filed instead, except for real property of cemeteries. |

Filling out the Nebraska Form 451 can seem like a daunting task, but it's an important step for qualifying organizations seeking a tax exemption on real and personal property. This process involves providing detailed information about the organization, the property in question, and the manner in which it is used to justify the exemption under state law. Taking it step by step can make the whole process smoother and more manageable.

After submitting the Form 451, it will be reviewed by the county assessor and, subsequently, the County Board of Equalization. Approval can lead to significant tax savings for your organization, making it vital to accurately and thoroughly complete this application. If the form is not properly filled out or is filed late, it might result in a denial of the exemption. Therefore, paying close attention to the deadline and the details of the application is crucial. Should there be any disapproval or questions regarding your application, be prepared to provide additional information or clarification to support your exemption claim.

The Nebraska 451 form is designed for organizations seeking tax exemption on real and personal property they own. This form must be used by qualifying organizations such as agricultural and horticultural societies, educational, religious, charitable, or cemetery organizations. Its primary purpose is to apply for a property tax exemption by providing detailed information about the organization, the property owned, and the specific use of the property that justifies the exemption according to state law.

Qualifying organizations owning real or depreciable tangible personal property, except licensed motor vehicles, must file the Nebraska 451 form if the property is used exclusively for purposes that align with the organization's exempt status. Examples include properties used for educational, religious, charitable, agricultural, horticultural, or cemetery purposes. This form should be filed with the county assessor of the county where the property is located, on or before December 31st of the year preceding the year for which the exemption is sought. Late filings may be submitted up to June 30th with a waiver request to the county board of equalization, subject to a possible penalty.

If the Nebraska 451 form is filed after the December 31st deadline, an organization may still submit the form up until June 30th, but it must also request a waiver from the county board of equalization. A late filing without an approved waiver or incorrect completion of the form can result in a denial of the exemption. Additionally, there is a penalty for late filing, which is the lesser of 10% of the tax that would have been due or $100 for each month or part of a month the filing is late.

To qualify for a property tax exemption using the Nebraska 451 form, an organization must meet several criteria:

These requirements ensure that only organizations that truly use their property for specific exempt purposes without profit motive and comply with non-discrimination laws benefit from tax exemptions.

Filing the Nebraska 451 form, which is essential for organizations seeking property tax exemption, requires meticulous attention to detail. A majority of mistakes stem from omissions or inaccuracies that could significantly delay or deny the exemption. Highlighting common errors can guide organizations towards successful completion and submission of this crucial document.

The first notable mistake involves the failure to fully complete all required sections of the form. The Nebraska 451 form demands comprehensive information about the organization, including its name, the taxable year in question, and detailed descriptions of both the property and its use. Organizations often mistakenly leave sections incomplete, particularly the detailed description of the property’s use. This detail is critical in determining if the property's use aligns with the exemption criteria, such as religious, educational, or charitable purposes. An incomplete form results in the county assessor's inability to accurately assess the property's eligibility for tax exemption.

Another common error is inaccurately describing the property's use, especially when the property serves multiple purposes. The form requires the applicant to specify the property's use and to affirm its exclusivity towards the purposes that qualify for exemption. If a property is used for both qualifying and non-qualifying purposes, the organization must clearly delineate these uses and provide accurate percentages of use. Many organizations fail to adequately detail how the property is used or mistakenly overstate the extent to which it serves a qualifying purpose, leading to potential challenges in achieving exemption status.

Submitting the form after the prescribed deadline is a particularly detrimental mistake. As stipulated in the form's instructions, timely submission—on or before December 31st preceding the tax year for which exemption is sought—is imperative. Late submissions significantly jeopardize the organization's ability to obtain a tax exemption. Although a waiver may be sought for submissions until June 30th following the initial deadline, this process requires demonstrating good cause for the delay, adds an additional layer of complexity, and incurs penalties. It's crucial for organizations to adhere to the deadlines to avoid these complications.

Lastly, the failure to properly address ownership and discriminatory practices issues can lead to denial of the exemption. The form queries about the property’s ownership, its use for financial gain, and whether the organization discriminates based on race, color, or national originated. Misrepresentations or inaccuracies in these sections not only contravene legal requirements but also undermine the integrity of the application. Ensuring accurate and honest responses to these queries is fundamental to securing tax-exempt status.

In summary, organizations applying for property tax exemptions via the Nebraska 451 form should exercise diligence in:

Attention to these details enhances the likelihood of a successful exemption application, facilitating the continued operation of essential services provided by qualifying organizations.

When organizations in Nebraska undertake the process of applying for a property tax exemption using the Form 451, there are several other types of documents and forms that they might need to prepare and submit alongside it. These documents are essential for providing comprehensive information about the organization, its ownership of the property, and how the property is used, which helps in the evaluation of the exemption application.

The submission of Form 451 along with these additional forms and documents creates a comprehensive package for the county assessor to review. This thorough approach ensures that the organization provides all necessary information upfront, potentially streamlining the process by reducing the need for further queries or document requests. Providing complete and accurate documentation as part of the application process is vital for an organization to successfully obtain a tax exemption for its property.

The Nebraska 451 form is similar to other documents that organizations use to apply for tax exemptions on properties, including the IRS Form 1023 and state-specific property tax exemption forms. Each of these forms requires detailed information about the organization's status, its ownership and use of the property, and the purpose that the property serves. For instance, the IRS Form 1023 is used by organizations to establish their tax-exempt status under Section 501(c)(3) of the Internal Revenue Code. Similar to the Nebraska 451 form, it asks for comprehensive details about the organization's structure, activities, and financial data to determine eligibility for tax exemption. However, while Form 1023 focuses broadly on federal income tax exemption, Nebraska 451 zeroes in on property tax exemption within the state, emphasizing the use and ownership specifics tied to real and personal property.

Another document resembling the Nebraska 451 form is the California BOE-267 form, a Claim for Welfare Exemption (First Filing) used by charitable, religious, scientific, or hospital corporations to get property tax exemptions. Like the Nebraska 451 form, BOE-267 requires detailed descriptions of the property and its use, ownership information, organizational details, and a declaration of the property's exclusive use for exempt purposes. Both forms serve a similar purpose in providing tax relief to qualifying organizations, though they cater to the specific requirements and laws of their respective states. The attention to how properties are employed for exempt activities underlines the broader goal: to support non-profit operations through tax relief measures, keeping the organization's focus on public benefit activities.

When filling out the Nebraska 451 form for a Tax Exemption on Real and Personal Property by Qualifying Organizations, it's important to follow specific guidelines to ensure your application is processed successfully:

Following these dos and don'ts can help streamline your application process and increase the likelihood of your organization receiving the tax exemption it's seeking.

When it comes to the Nebraska 451 form, several misconceptions often arise, leading to confusion and potential mistakes in the filing process. Understanding the intricacies of this form can help organizations correctly navigate the exemption application process. Here are five common misconceptions clarified:

Correctly understanding and addressing these misconceptions about the Nebraska 451 form can significantly impact an organization's ability to successfully gain a property tax exemption. Detailed attention to the form's requirements and deadlines is crucial for any qualifying organization seeking exemption.

Filling out and using the Nebraska 451 form for tax exemption on real and personal property requires attention to detail and an understanding of the criteria for exemption. Here are six key takeaways that can help ensure the process is handled correctly:

Successfully navigating the exemption application process involves ensuring all documentation is accurate, submitted in a timely manner, and thoroughly supports the organization's qualification for exemption. Keeping these key points in mind can smooth the pathway to achieving tax-exempt status for qualifying properties.

Nebraska Form 33 - Farmers and ranchers have specific rules on Form 2210N for calculating underpayment penalties, with exemptions under certain conditions.

Nebraska Filing Requirements - For publicly traded partnerships, special provisions exempt them from the withholding requirements stated in the context of form 12N agreements.

Nebraska Sales Tax Login - Facilitates adjustments for sales through Multivendor Marketplace Platforms, ensuring accurate net taxable sales reporting.