Fill a Valid Nebraska 51C Form

Fill a Valid Nebraska 51C Form

When counties, cities, or villages in Nebraska embark on the journey of conducting a lottery, they must acquaint themselves with the necessary procedural and fiscal responsibilities dictated by the Nebraska 51C form. This document, integral to the compliance framework surrounding local lotteries, requires diligent completion and timely submission per tax period, ensuring that even in instances where no tax is due, a return is filed. The form meticulously outlines the requirement to report gross proceeds from lottery activities, calculate due taxes at a designated rate, and reconcile any previous balances with applicable interest or payments received. Furthermore, it underlines the importance of a signed declaration by an authorized official, attesting to the accuracy and completeness of the information provided. Essential instructions on the reverse side of the form guide entities through the preparation process, offer clarity on who must file, highlight the significance of adhering to the filing deadline, and address the protocol for submitting the form alongside the requisite payment to the Nebraska Department of Revenue. The directions also emphasize the consequences of non-compliance, including penalties, interest charges, potential license ramifications, and the necessity of retaining records for verification and audit purposes. Completeness, accuracy, and punctuality are crucial elements emphasized throughout the documentation, which serves not just as a tax return but as a vital link in the regulatory oversight of lottery operations within the state.

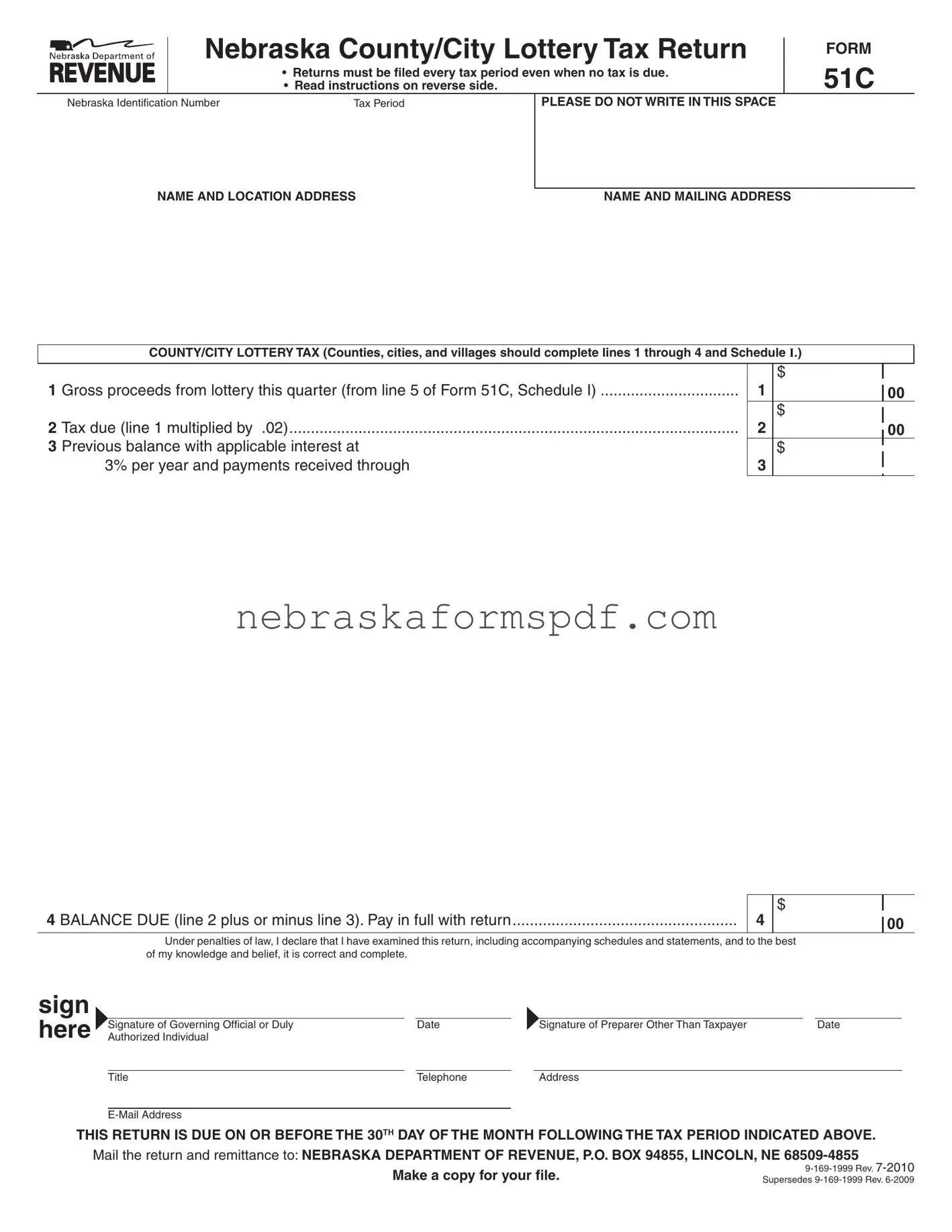

Nebraska County/City Lottery Tax Return

• Returns must be filed every tax period even when no tax is due. • Read instructions on reverse side.

FORM

51C

Nebraska Identification Number |

Tax Period |

PLEASE DO NOT WRITE IN THIS SPACE

NAME AND LOCATION ADDRESS |

NAME AND MAILING ADDRESS |

COUNTY/CITY LOTTERY TAX (Counties, cities, and villages should complete lines 1 through 4 and Schedule I.)

1 Gross proceeds from lottery this quarter (from line 5 of Form 51C, Schedule I) ................................

2 Tax due (line 1 multiplied by .02)........................................................................................................

3 Previous balance with applicable interest at

3% per year and payments received through

|

$ |

1 |

00 |

|

|

|

$ |

2 |

00 |

|

$ |

3 |

|

|

|

4 BALANCE DUE (line 2 plus or minus line 3). Pay in full with return ....................................................

4

$

00

Under penalties of law, I declare that I have examined this return, including accompanying schedules and statements, and to the best of my knowledge and belief, it is correct and complete.

sign here

|

|

|

|

|

|

|

Signature of Governing Official or Duly |

|

Date |

|

Signature of Preparer Other Than Taxpayer |

|

Date |

Authorized Individual |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Title |

Telephone |

Address |

THIS RETURN IS DUE ON OR BEFORE THE 30TH DAY OF THE MONTH FOLLOWING THE TAX PERIOD INDICATED ABOVE.

Mail the return and remittance to: NEBRASKA DEPARTMENT OF REVENUE, P.O. BOX 94855, LINCOLN, NE

Make a copy for your file. |

||

Supersedes |

||

|

INSTRUCTIONS

WHO MUST FILE. Every county, city, or village licensed to conduct a lottery must ile this return. A return is required for every tax period, or portion of a tax period, from each county, city, or village licensed even when no tax is due.

WHEN AND WHERE TO FILE. This return, properly signed, with a check payable to the Nebraska Department of Revenue for the balance reported on line 4, is considered timely iled if postmarked on or before the 30th day of the month following the end of the tax period covered by the return. Mail to the Nebraska Department of Revenue, P.O. Box 94855, Lincoln, Nebraska

Counties, cities, and villages licensed to conduct a lottery must ile Nebraska Schedule I – County/City Lottery Activity Report with this return.

PREIDENTIFIED RETURN. This return must be used only by the licensed organization whose name is printed on it. Do not ile returns which are photocopies, are for another tax period, or have not been preidentiied. If you have not received a return for the tax period, and will be iling a paper return, request a duplicate from the Charitable Gaming Division, or visit our website at www.revenue.ne.gov/gaming to print a Form 51C. Complete the ID number, tax period, name, and address information.

PENALTY AND INTEREST. In the event that the return is not iled by the prescribed due date, a penalty will be assessed in the amount of ten percent of the tax not paid by the due date, or $25, whichever is greater. Interest on any unpaid tax will be assessed at the rate speciied in Neb. Rev. Stat. §

VERIFICATION AND AUDIT. Records to substantiate this return must be kept available for a period of at least three years following the date of iling the return.

SPECIFIC INSTRUCTIONS

LINE 1. Counties, cities, and villages are required to remit a two percent tax on all gross proceeds from the conduct of a lottery. Enter line 5 from Nebraska Schedule I – County/City Lottery Activity Report.

LINE 2. Multiply line 1 by the state tax rate indicated. This is the amount of county/city lottery tax due to the Department for this tax period.

LINE 3. A balance due or credit resulting from a partial payment, mathematical or clerical error, penalty, or interest relating to prior returns will be entered in this space by the Department. The amount of interest includes interest on unpaid tax through the due date of this return. If the amount due is paid before the due date, the interest will be recomputed, and a credit will be given on your next return. If the amount entered has been satisied by a previous remittance, it should be disregarded when computing the amount to remit on line 4. If a credit is shown, it may be applied to the current tax liability.

LINE 4. Attach a check made payable to the Nebraska Department of Revenue for the amount reported on line 4. Checks may be presented for payment electronically.

AUTHORIZED SIGNATURE. This return must be signed by a governing oficial or other duly authorized individual. A person who is paid for preparing this return must also sign the return as a preparer.

Any questions regarding the completion of the Nebraska County/City Lottery Tax Return, Form 51C, should be addressed to the Nebraska Department of Revenue, Charitable Gaming Division, P.O. Box 94855, Lincoln, Nebraska

| Fact | Details |

|---|---|

| Purpose of Form 51C | Nebraska County/City Lottery Tax Return is used by counties, cities, or villages licensed to conduct a lottery to report and pay taxes on the gross proceeds from the lottery. |

| Filing Requirement | A return must be filed for every tax period, or portion thereof, even when no tax is due. |

| Filing Deadline | The return must be postmarked on or before the 30th day of the month following the end of the tax period covered by the return. |

| Where to File | Returns should be mailed to the Nebraska Department of Revenue, P.O. Box 94855, Lincoln, Nebraska 68509-4855. |

| Tax Rate | A two percent tax is assessed on all gross proceeds from the conduct of a lottery. |

| Penalty for Late Filing | If not filed by the due date, a penalty of ten percent of the tax not paid by the due date, or $25, whichever is greater, is assessed. Interest is also charged on any unpaid tax. |

| Record Keeping | Records substantiating the return must be kept for at least three years following the date of filing. |

| Authorized Signature | The return must be signed by a governing official or another duly authorized individual. If a preparer is paid to prepare the return, they must also sign. |

| Contact Information | Questions regarding Form 51C can be addressed to the Nebraska Department of Revenue, Charitable Gaming Division, at the provided mailing address or telephone numbers. |

Successfully completing and submitting the Nebraska 51C form is an essential step for counties, cities, and villages licensed to conduct a lottery in the state of Nebraska. This document, necessary for every tax period, ensures compliance with regulatory requirements and aids in the proper accounting of lottery proceeds. Here are the steps that should be followed carefully to fill out the Nebraska 51C form accurately:

After the submission, keep in mind that the Nebraska Department of Revenue may reach out if there are questions or further clarification is needed. It's also important to maintain records related to the return and its associated documents for at least three years after filing, as these may be requested for verification or auditing purposes. Timely and accurate completion of the Nebraska 51C form helps in upholding the integrity of licensed lottery activities within the state.

The Nebraska 51C form, referred to as the Nebraska County/City Lottery Tax Return, is designed for counties, cities, and villages licensed to conduct a lottery. Its primary purpose is for these entities to report and remit a two percent tax on all gross proceeds derived from lottery operations for the designated tax period. This filing requirement applies even if no tax is due for the period.

Every county, city, or village that holds a license to conduct a lottery within Nebraska is obligated to file this return. A return must be filed for every tax period or portion thereof during which the licensed organization was active, regardless of whether any tax is owed for that period.

The completed form, along with any tax due, must be postmarked on or before the 30th day of the month following the end of the tax period it covers. Timely submission is crucial to avoid penalties and interest for late filing and payment.

The filing entity should mail the signed form and any applicable payment to the Nebraska Department of Revenue at the address provided: P.O. Box 94855, Lincoln, NE 68509-4855. The Department emphasizes the importance of using the pre-identified return specific to the licensed organization for a given tax period.

If a county, city, or village fails to file the return by the due date, the law mandates a penalty. The penalty is calculated as ten percent of the unpaid tax by the due date or $25, whichever amount is greater. Additionally, interest accrues on any unpaid tax from the due date until full payment is received. This rate is specified in Nebraska Revised Statute § 45-104.02, as amended.

The tax owed is computed as two percent of the gross lottery proceeds for the tax period. Gross proceeds are reported on line 5 of Form 51C, Schedule I – County/City Lottery Activity Report, which must be attached to the return. Calculation errors or missing information can lead to adjustments by the Department, resulting in either additional tax due or credit.

In case of any discovered inaccuracies after submission, counties, cities, and villages should contact the Nebraska Department of Revenue, Charitable Gaming Division, directly to rectify the situation. Keeping accurate and comprehensive records for at least three years following the filing date of the return is advised to support any needed amendments or audits.

Filling out the Nebraska 51C form might seem straightforward, but there are common pitfalls that can lead to errors, potentially causing delays or financial penalties. Here's a look at four mistakes people often make when completing this document:

Understanding these pitfalls and ensuring attention to detail can mitigate the risks of encountering delays, penalties, or additional scrutiny. The Nebraska Department of Revenue also provides resources and guidance to assist with the completion of the 51C form. When in doubt, contacting the department directly or consulting with a professional can provide clarity and prevent these common mistakes.

Filing the Nebraska 51C form, a Nebraska County/City Lottery Tax Return, is a crucial step for counties, cities, and villages licensed to conduct lotteries in Nebraska. However, to ensure compliance and thorough reporting, several other forms and documents often accompany this key form. Understanding these additional requirements can simplify the process and help avoid common pitfalls.

Properly managing and filing these documents ensures compliance with Nebraska's regulatory requirements for conducting lotteries. It protects the rights of all parties involved and supports the smooth operation of lawful gambling activities within the state. Keep in mind, staying informed and up-to-date with Nebraska’s Department of Revenue’s guidelines plays a crucial role in navigating the complexities of legal lottery or gambling operations.

The Nebraska 51C form, which is designed for counties, cities, and villages to report and remit a tax on gross proceeds from lottery activities, bears similarity to other tax forms that cater to specific segments or transactions within the state's governance framework. Understanding these similarities can help in comprehensively navigating the tax filing procedures for various entities.

One similar document is the Form 10, the Sales and Use Tax Return. Like the Nebraska 51C form, Form 10 is utilized for reporting the gross proceeds from sales, albeit in a broader commercial context rather than specifically from lotteries. Both forms require the calculation of a tax amount based on a prescribed rate (2% for lottery tax, and varying rates for sales and use tax), the reporting of any previous balances or adjustments, and the remittance of the resulting balance due. Additionally, both forms necessitate the declaration of the tax period and the detailed instruction on payment and submission deadlines, emphasizing their structured approach to state tax compliance.

Another document sharing common ground with the Nebraska 51C is the Form 941N, the Nebraska Income Tax Withholding Return. This form is for employers to report state income tax withheld from employees' wages. Similar to the 51C, the 941N form requires entities to report gross amounts (in this case, wages paid) and calculate taxes due based on specific rates. Both forms also provide space for adjustments to prior reports and require the identification of the reporting period. The necessity for accurate calculations and timely submissions under penalty of interest and fines underscores the critical nature of these forms in maintaining tax compliance and supporting state-funded programs and services.

These comparisons illuminate the 51c form's role within a complex system of state taxation, highlighting its specific focus on lottery proceeds while drawing parallels to the broader tax reporting and remittance landscape. While each form targets different sources of state revenue, their structured format, requirement for periodic filing, and emphasis on detailed record-keeping and accurate payment submission unite them in purpose.

When filling out the Nebraska 51C form for lottery tax return, there are several crucial dos and don'ts to keep in mind. Being thorough and accurate ensures compliance and avoids potential issues with the Nebraska Department of Revenue. Here is a guided list to help streamline this task:

By following these guidelines, organizations can ensure they meet all requirements for the Nebraska County/City Lottery Tax Return and avoid penalties or errors in their submission.

Misunderstandings often arise regarding the Nebraska 51C form, which is crucial for counties, cities, and villages conducting lotteries. Let's clarify some common misconceptions.

Only counties and cities with substantial lottery earnings need to file Form 51C. In reality, every county, city, or village licensed to conduct a lottery must file this return for every tax period, regardless of the amount of earnings or even if no tax is due.

It's acceptable to file a photocopy of Form 51C if the original is misplaced. Actually, the form must be used only by the licensed organization whose name is printed on it. Photocopies or forms from other tax periods are not allowed. If the original form is misplaced, a new one must be requested from the Charitable Gaming Division.

Filing the form late has no consequences if no tax is due. This is incorrect. Failing to file by the deadline can result in penalties, even if no tax is owed. The law requires timely filing of this form to ensure compliance with licensing requirements.

The form is complex and requires professional preparation. While the form does require careful attention to detail, the instructions provided are designed to help county, city, or village officials complete it correctly. Professional preparation is not necessarily required, but accuracy is important.

Payment method is limited to checks. While the form instructions suggest attaching a check, it also mentions that checks may be presented for payment electronically. This provides more flexibility in payment methods than some might assume.

Any governing official can sign the form. The form must be signed by a governing official or other duly authorized individual. This distinction is important to ensure that the signatory has the legal authority to bind the entity in matters related to the lottery tax return.

Records related to the lottery only need to be kept until the form is filed. Actually, records must be kept available for at least three years following the filing of the return. This requirement is in place to accommodate possible verification and audit processes.

If a mistake is made, it's too late to correct once the form is filed. Corrections are possible through adjustments in subsequent filings or through communication with the Nebraska Department of Revenue. Making an error does not mean compliance is permanently compromised.

Understanding these aspects of the Nebraska 51C form helps ensure that counties, cities, and villages comply with state regulations and avoid unnecessary penalties or audits.

Filling out and using the Nebraska 51C form is crucial for counties, cities, and villages conducting lotteries. Here are four key takeaways that one should remember:

Adhering to these guidelines when completing the Nebraska 51C form can help counties, cities, and villages smoothly navigate the process of reporting lottery tax, ensuring compliance and avoiding unnecessary penalties.

Nebraska 1040n - Appoint authorized personalities to interface with Nebraska tax officials on audits, refunds, and appeals using the convenient Form 33.

How Much Notary Cost - Helps to prevent the misuse of notarial powers by binding the notary to a legal and financial commitment.

Form 6 Nebraska - Requirement to state the number of wells on the lease, including the new well, that are completed in or drilling into the reservoir.