Fill a Valid Nebraska 6 Form

Fill a Valid Nebraska 6 Form

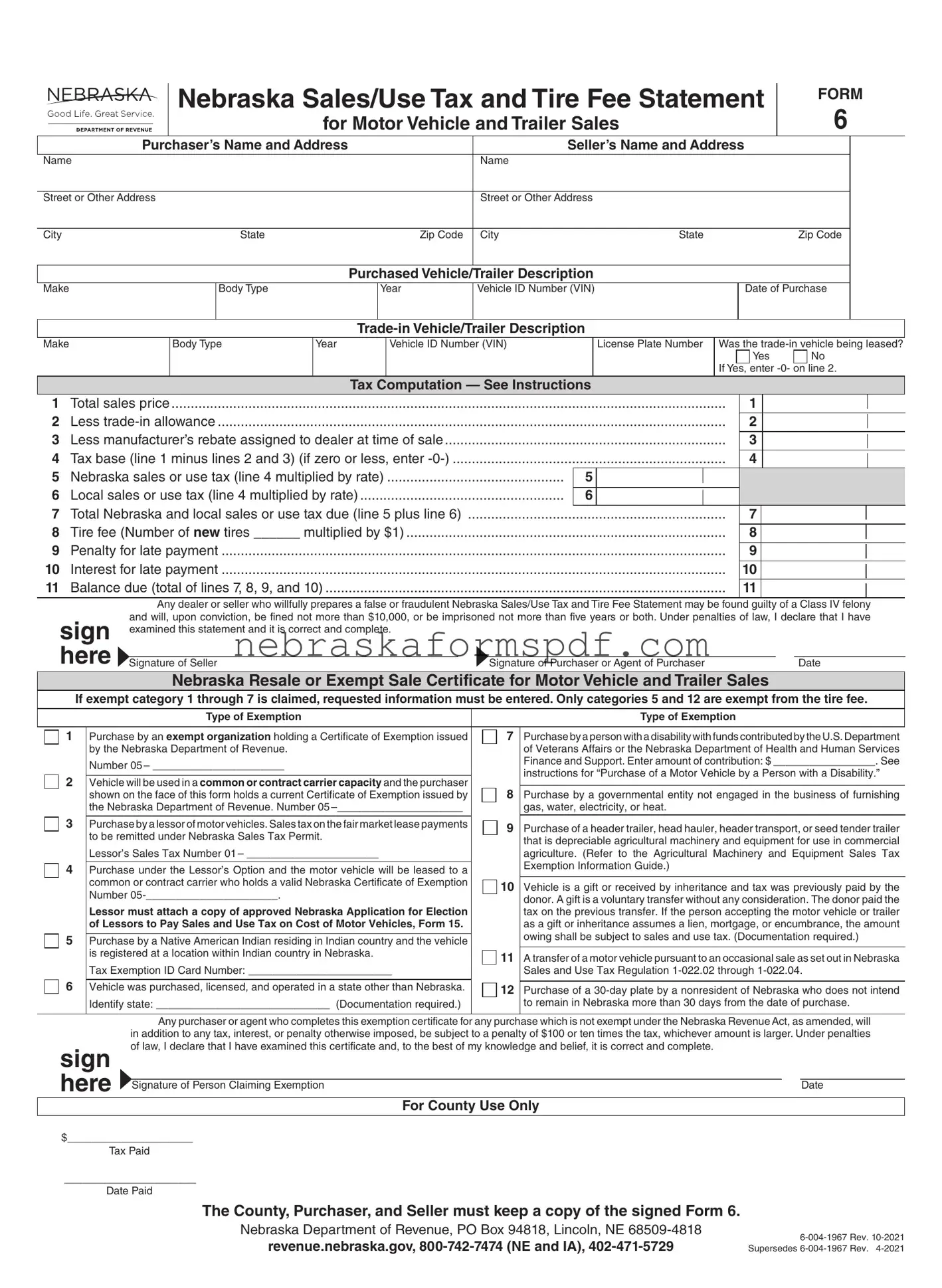

When it comes to purchasing a motor vehicle or trailer in Nebraska, understanding the complexities of the Nebraska Sales/Use Tax and Tire Fee Statement, commonly known as Form 6, is crucial for both buyers and sellers. This form serves as a comprehensive document that outlines the sales or use tax and tire fee obligations that must be satisfied during the transaction. Covering everything from the basic details of the purchaser and seller, through to the specific descriptions of the purchased and traded-in vehicles, including make, body type, year, and the Vehicle Identification Number (VIN), the form is detailed in its scope. Crucially, it includes a section for tax computation, guiding the involved parties through calculating the taxable amount after considering trade-ins and manufacturer rebates, the applicable sales or use tax, and any local taxes. Additionally, it warns of severe penalties for willful preparation of a false statement, emphasizing the form's legal significance. For those vehicles and transactions that qualify for exemption, Form 6 also outlines the necessary criteria and documentation, addressing scenarios ranging from purchases by exempt organizations to vehicles bought by persons with disabilities or purchased in other states. In essence, Form 6 not only facilitates the transparent and lawful exchange of vehicle ownership but also ensures compliance with Nebraska's tax laws, rendering it a critical document in the vehicle purchasing process.

Nebraska Sales/Use Tax and Tire Fee Statement

for Motor Vehicle and Trailer Sales

FORM

6

Purchaser’s Name and Address |

Seller’s Name and Address |

|

||

Name |

|

Name |

|

|

|

|

|

|

|

Street or Other Address |

|

Street or Other Address |

|

|

|

|

|

|

|

City |

State |

Zip Code City |

State |

Zip Code |

Purchased Vehicle/Trailer Description

Make

Body Type

Year

Vehicle ID Number (VIN)

Date of Purchase

Make

Body Type

Year

Vehicle ID Number (VIN)

License Plate Number

Was the

Yes |

No |

|

If Yes, enter |

2. |

|

Tax Computation — See Instructions

1 |

Total sales price |

|

|

1 |

|

2 |

Less |

|

|

2 |

|

|

Less manufacturer’s rebate assigned to dealer at time of sale |

|

|

|

|

3 |

|

|

3 |

|

|

|

Tax base (line 1 minus lines 2 and 3) (if zero or less, enter |

|

|

|

|

4 |

|

|

4 |

|

|

5 |

Nebraska sales or use tax (line 4 multiplied by rate) |

5 |

|

|

|

|

Local sales or use tax (line 4 multiplied by rate) |

|

|

|

|

6 |

6 |

|

|

|

|

|

Total Nebraska and local sales or use tax due (line 5 plus line 6) |

|

|

|

|

7 |

|

|

7 |

|

|

|

Tire fee (Number of new tires ______ multiplied by $1) |

|

|

|

|

8 |

|

|

8 |

|

|

|

Penalty for late payment |

|

|

|

|

9 |

|

|

9 |

|

|

|

Interest for late payment |

|

|

|

|

10 |

|

|

10 |

|

|

11 |

Balance due (total of lines 7, 8, 9, and 10) |

|

|

11 |

|

|

|

|

|

|

|

|

Any dealer or seller who willfully prepares a false or fraudulent Nebraska Sales/Use Tax and Tire Fee Statement may be found guilty of a Class IV felony |

||||

sign |

and will, upon conviction, be fined not more than $10,000, or be imprisoned not more than five years or both. Under penalties of law, I declare that I have |

||||

examined this statement and it is correct and complete. |

|

|

|

|

|

here |

|

|

|

|

|

|

|

|

|

|

|

Signature of Seller |

|

Signature of Purchaser or Agent of Purchaser |

|

Date |

|

|

|

||||

|

|

||||

Nebraska Resale or Exempt Sale Certificate for Motor Vehicle and Trailer Sales

If exempt category 1 through 7 is claimed, requested information must be entered. Only categories 5 and 12 are exempt from the tire fee.

|

|

|

Type of Exemption |

|

Type of Exemption |

|

|

|

|

|

|

||

|

|

1 |

Purchase by an exempt organization holding a Certificate of Exemption issued |

7 |

Purchase by a person with a disability with funds contributed by the U.S. Department |

|

|

|

|

by the Nebraska Department of Revenue. |

|

of Veterans Affairs or the Nebraska Department of Health and Human Services |

|

|

|

|

Number 05 – ______________________ |

|

Finance and Support. Enter amount of contribution: $ _________________. See |

|

|

|

|

|

instructions for “Purchase of a Motor Vehicle by a Person with a Disability.” |

||

2 |

|

|

||||

Vehicle will be used in a common or contract carrier capacity and the purchaser |

8 |

|||||

|

||||||

Purchase by a governmental entity not engaged in the business of furnishing |

||||||

|

|

|

shown on the face of this form holds a current Certificate of Exemption issued by |

|||

|

|

|

the Nebraska Department of Revenue. Number 05 |

|

gas, water, electricity, or heat. |

|

3 |

Purchase by a lessor of motor vehicles. Sales tax on the fair market lease payments |

9 |

Purchase of a header trailer, head hauler, header transport, or seed tender trailer |

|||

|

|

|

to be remitted under Nebraska Sales Tax Permit. |

|||

|

|

|

|

that is depreciable agricultural machinery and equipment for use in commercial |

||

|

|

|

|

|

||

|

|

|

Lessor’s Sales Tax Number 01 – ______________________ |

|

agriculture. (Refer to the Agricultural Machinery and Equipment Sales Tax |

|

4 |

Purchase under the Lessor’s Option and the motor vehicle will be leased to a |

|

Exemption Information Guide.) |

|||

|

|

|||||

|

|

|

common or contract carrier who holds a valid Nebraska Certificate of Exemption |

10 |

Vehicle is a gift or received by inheritance and tax was previously paid by the |

|

|

|

|

Number |

|||

|

|

|

|

donor. A gift is a voluntary transfer without any consideration. The donor paid the |

||

|

|

|

|

|

||

|

|

|

Lessor must attach a copy of approved Nebraska Application for Election |

|

tax on the previous transfer. If the person accepting the motor vehicle or trailer |

|

|

|

|

of Lessors to Pay Sales and Use Tax on Cost of Motor Vehicles, Form 15. |

|

as a gift or inheritance assumes a lien, mortgage, or encumbrance, the amount |

|

|

|

5 |

|

|

owing shall be subject to sales and use tax. (Documentation required.) |

|

|

|

Purchase by a Native American Indian residing in Indian country and the vehicle |

|

|||

|

|

|

|

|||

|

|

|

is registered at a location within Indian country in Nebraska. |

11 |

A transfer of a motor vehicle pursuant to an occasional sale as set out in Nebraska |

|

|

|

|

|

|||

|

|

|

Tax Exemption ID Card Number: ________________________ |

|

Sales and Use Tax Regulation |

|

|

|

6 |

|

|

|

|

|

|

Vehicle was purchased, licensed, and operated in a state other than Nebraska. |

12 |

Purchase of a |

||

|

|

|

Identify state: _____________________________ (Documentation required.) |

|

to remain in Nebraska more than 30 days from the date of purchase. |

|

|

|

|

|

|

|

|

|

Any purchaser or agent who completes this exemption certificate for any purchase which is not exempt under the Nebraska Revenue Act, as amended, will |

||

|

in addition to any tax, interest, or penalty otherwise imposed, be subject to a penalty of $100 or ten times the tax, whichever amount is larger. Under penalties |

||

sign |

of law, I declare that I have examined this certificate and, to the best of my knowledge and belief, it is correct and complete. |

|

|

here |

|

|

|

Signature of Person Claiming Exemption |

|

Date |

|

|

|

|

|

For County Use Only

$_____________________

Tax Paid

______________________

Date Paid

The County, Purchaser, and Seller must keep a copy of the signed Form 6.

Nebraska Department of Revenue, PO Box 94818, Lincoln, NE

revenue.nebraska.gov,

Instructions for Purchaser

Paying Taxes and Tire Fees. The purchaser of a motor vehicle or trailer must present two copies of this statement to the county treasurer, the Department of Motor Vehicles (DMV), or other designated county official within 30 days after the date of purchase, and pay the Nebraska and local sales or use tax, and the tire fee. The date of purchase is the earlier of two dates: the date on the motor vehicle title; or the date of possession, as evidenced by the date of purchase shown on the Nebraska Sales/Use Tax and Tire Fee Statement, Form 6. The purchaser should retain a copy of this statement for a period of at least six years.

Penalty and Interest. If the total sales or use tax and tire fee are not paid within 30 days of the purchase date, the county treasurer, DMV, or designated county official will assess and collect penalty and interest at the statutory rate. If you have any questions regarding the purchase date, or penalty and interest rates, please contact your local county treasurer’s office or the Nebraska Department of Revenue (DOR) at

Sales Tax Paid to Another State. A motor vehicle purchased in another state, with sales tax properly paid to the other state, but registered for the first time in Nebraska, is subject to use tax at the time of registration. If the state the vehicle was purchased in has reciprocity with Nebraska, the total sales tax paid in that state will be credited toward the total state and local use tax due in Nebraska. No refund will be made if the other state’s tax rate exceeds the total Nebraska and local use tax rate.

Line 2. A vehicle that is used as a

Line 4. No refund will be made if the tax base results in a negative amount. Exemptions. If the transfer of title to the motor vehicle or trailer described on this statement is exempt from sales and use taxes, the Nebraska Resale or Exempt Sale Certificate, located on the front of this statement, must be completed prior to registration.

The purchaser must present documentation that supports the sales tax exemption. If the documentation is not sufficient, the county treasurer, DMV, or other designated county official is authorized to collect the sales tax. The purchaser may submit a claim to DOR requesting a refund of the sales taxes paid.

Purchase of a Motor Vehicle by a Person with a Disability. If the amount contributed by the U.S. Department of Veterans Administration (VA) or the Nebraska Department of Health and Human Services Finance and Support (DHHS) is the maximum amount allowed by law, the entire purchase price of the motor vehicle is exempt from sales tax. The entire purchase price is exempt, even if the purchase price is greater than the maximum amount contributed. If the contributed amount is less than the maximum amount allowed by law, only the amount contributed is exempt from sales tax. If there is a question as to whether the maximum amount was received, Form

Mobility Enhancing Equipment. Any person with a disability who is required to use durable medical equipment or prosthetics for moving from one place to another place, may purchase mobility enhancing equipment with a motor vehicle exempt from sales tax. Please refer to the Nebraska Certificate of Exemption for Mobility Enhancing Equipment on a Motor Vehicle, Form 13ME.

Underpayment of Tax. Underpayment of sales or use tax or tire fee on this statement must be reported on an Amended Nebraska Sales/Use Tax and Tire Fee Statement for Motor Vehicle and Trailer Sales, Form 6XN. Form 6XN is available at each county treasurer’s office and DOR.

Instructions for Seller

Licensed Motor Vehicle Dealer or Licensed Permitholder. A motor vehicle dealer, or sales tax permitholder, must complete this statement for every sale of a motor vehicle or trailer. Signed copies should be distributed in the following manner:

1.A signed copy must be retained with your business records;

2.A signed copy must be mailed to DOR at the address at the bottom of the Form 6 if

3.Two signed copies must be given to the purchaser.

The sales price on line 1 must include amounts for destination charges, import custom fees, surcharges, service and maintenance agreements, document processing charges, charges for warranty transfers, and

Individual Without a Sales Tax Permit. An individual, who is not licensed to collect sales tax, must complete this statement for every

sale of a motor vehicle or trailer. The copies should be distributed in the following manner:

1.Retain a signed copy with your records; and

2.Provide two copies of the signed form to the purchaser.

An individual can accept another motor vehicle, motorboat,

Leased Vehicles. A lessee cannot use the

Tire Fee. Motor vehicle dealers selling new motor vehicles, trailers, or

of new tires on a

Individuals selling used motor vehicles are not required to indicate the number of tires.

Instructions for County Treasurers, DMV, and Other Designated County Officials

Collecting Taxes and Tire Fees. The county treasurer, DMV, or other designated county official must collect the state and applicable local sales and use taxes, and the tire fee, prior to registering the motor vehicle or trailer.

A signed copy of this form must be receipted in the space provided for validation. A copy must be returned to the purchaser. Counties are required to retain a copy of this form and provide copies to DOR upon request.

Collection of Penalty and Interest. If the appropriate sales or use taxes and fees are not paid within 30 days after the purchase date, penalty and interest must be collected at the statutory rate from the due date through the date of payment. If the due date falls on a Saturday, Sunday, or a holiday, the purchaser may still pay the amount due on the next business day without incurring penalty and interest.

Nebraska Department of Revenue, PO Box 94818, Lincoln, NE

| Fact Name | Fact Detail |

|---|---|

| Governing Law | The Nebraska Sales/Use Tax and Tire Fee Statement for Motor Vehicle and Trailer Sales, Form 6, is governed by the laws of the State of Nebraska. |

| Filing Deadline | Purchasers must present the completed Form 6 to the county treasurer, Department of Motor Vehicles (DMV), or other designated county official within 30 days after the date of purchase. |

| Penalties for Late Payment | If the total sales or use tax and tire fee are not paid within 30 days of the purchase date, penalty and interest at the statutory rate will be assessed and collected by the county treasurer, DMV, or designated county official. |

| Tax Reciprocity | A motor vehicle purchased in another state with sales tax properly paid, and registered for the first time in Nebraska, is subject to use tax at the time of registration. The state's tax paid will be credited against the total state and local use tax due in Nebraska if the vehicle was purchased in a state with reciprocity. |

| Documentation for Exemptions | If the transfer of title is exempt from sales and use taxes, the Nebraska Resale or Exempt Sale Certificate part of the Form 6 must be completed and sufficient documentation supporting the exemption must be presented before registration. |

| Responsibilities for Incorrect Declarations | Any dealer or seller who willfully prepares a false or fraudulent Form 6 may be found guilty of a Class IV felony and, upon conviction, be fined up to $10,000, imprisoned for up to five years, or both. Furthermore, any purchaser or agent completing the exemption certificate inaccurately will be subject to a penalty of $100 or ten times the tax, whichever is greater. |

Filling out the Nebraska 6 form, the Sales/Use Tax and Tire Fee Statement for Motor Vehicle and Trailer Sales, is a crucial step in the vehicle purchasing process within Nebraska. This form ensures the accurate calculation and payment of sales or use taxes, and tire fees associated with the transfer of vehicle ownership. It is vital for both the seller and the purchaser to provide complete and accurate information to avoid legal complications or possible penalties. Here are the steps to properly fill out the Nebraska 6 form.

After the form is fully completed and signed, the next step involves submitting it to the appropriate county office. Remember, timely submission within 30 days from the date of purchase is essential to avoid penalties. The purchaser should keep a copy of the completed form for their records. The attention to detail in completing the form ensures compliance with Nebraska tax laws and contributes to a smoother vehicle registration process.

The Nebraska 6 form, known as the Nebraska Sales/Use Tax and Tire Fee Statement for Motor Vehicle and Trailer Sales, is a document required for reporting and paying sales or use tax, and tire fees associated with the purchase of a motor vehicle or trailer. It ensures compliance with Nebraska state tax laws by documenting the transaction details, including the sale price, trade-in value, and applicable taxes and fees.

The form must be presented to the county treasurer, the Department of Motor Vehicles (DMV), or other designated county official within 30 days following the date of purchase. This timeframe helps avoid the assessment of penalties and interest for late payments.

Both individuals and dealers involved in the sale or purchase of a motor vehicle or trailer in Nebraska are required to complete the form. Dealers or sellers need to ensure its accurate completion and submission as part of their sales documentation process, while purchasers must present it when registering the vehicle.

The Total Sales or Use Tax is calculated by subtracting the trade-in allowance and any manufacturer’s rebate from the total sales price, resulting in the tax base. This amount is then multiplied by the applicable tax rate to determine the Nebraska sales or use tax, with local taxes added if applicable.

Exemptions can apply under specific conditions, including but not limited to:

Penalties and interest are assessed for payments made after 30 days from the purchase date. The rate is statutory and accrues from the due date until the date of payment. If the due date falls on a weekend or holiday, payment can be made on the next business day without incurring additional charges.

Yes, if a motor vehicle is purchased in another state and sales tax is paid to that state, the amount may be credited against the total state and local use tax due in Nebraska. The vehicle must be registered for the first time in Nebraska, and the credit applies only if the other state has tax reciprocity with Nebraska.

For trade-ins to be deductible, the vehicle must be titled in the purchaser’s name or that of their parent, guardian, or child. The trade-in value is deducted from the total sales price before calculating the tax due. Leased vehicles do not qualify for a trade-in allowance unless the lease buy-out was previously taxed.

In cases of underpayment on the form, the discrepancy must be reported on an Amended Nebraska Sales/Use Tax and Tire Fee Statement for Motor Vehicle and Trailer Sales, Form 6XN. This form is available at county treasurer’s offices and through the Nebraska Department of Revenue.

Filling out the Nebraska 6 form accurately is crucial for both the buyer and seller in a vehicle transaction to ensure compliance with state tax laws and regulations. Common mistakes can lead to unnecessary penalties, interest, or even legal issues. Here are ten common pitfalls to avoid:

It's vital for both parties involved in the sale or transfer of a vehicle or trailer to understand each section of the Nebraska 6 form. Paying close attention to the details and avoiding these common mistakes can ensure a smoother transaction and proper tax compliance. Awareness and diligence in filling out this form correctly can save time, avoid legal complications, and ensure that all financial obligations to the state of Nebraska are met accurately and timely.

When completing the Nebraska 6 form, which is crucial for documenting the sale, use tax, and tire fee details of motor vehicle and trailer transactions in Nebraska, it's essential to pair it with other relevant forms and documents to ensure full compliance and accuracy in reporting. These complementary documents not only streamline the process but also provide a comprehensive overview of the transaction's tax and legal aspects. Here's a look at four additional documents often used alongside the Nebraska 6 form:

These documents play vital roles in the vehicle sales process, from ensuring tax compliance and exemptions are properly applied, to correcting any potential mistakes in the initial documentation. Having a thorough understanding of each document's purpose and requirements can significantly ease the process of purchasing, selling, or transferring vehicle ownership in Nebraska.

The Nebraska 6 form is similar to other tax documents that are used across the United States for the specific purpose of reporting and paying sales/use tax and other fees related to the purchase of motor vehicles and trailers. While the form itself is unique to Nebraska, the principles and structure reflect a common approach to tax documentation within the realm of motor vehicle transactions.

One example of a document that resembles the Nebraska 6 form is the Sales and Use Tax Return (Form ST-3) used in many states for reporting general sales and use tax. Both forms require the seller and purchaser to provide detailed information about the transaction, including the sale price and identification of the item sold. However, Nebraska's Form 6 is more specialized, focusing specifically on motor vehicles and trailers, including specifics such as the VIN, and addresses additional fees like the tire fee. The ST-3 form, on the other hand, might be used for a wider range of transactions beyond just vehicles.

Another example is the Vehicle Use Tax Transaction Return in states like Illinois, known as Form RUT-25. Similar to Nebraska's Form 6, this form is tailored to vehicle transactions, requiring detailed vehicle and sales information to compute taxes owed. Both forms accommodate for trade-ins and provide fields for exemptions, specifying various scenarios where tax may be reduced or not applicable. They also share a focus on ensuring compliance with state-specific tax laws relating to vehicle purchases, highlighting the importance of accurately reporting to state revenue departments.

When completing the Nebraska 6 form, which is the Nebraska Sales/Use Tax and Tire Fee Statement for Motor Vehicle and Trailer Sales, certain practices should be followed to ensure accuracy and compliance with state laws. Here is a list of dos and don'ts:

Compliance with these guidelines will aid in the correct and timely processing of the Nebraska 6 form, ensuring adherence to Nebraska’s tax collection requirements for the sale of motor vehicles and trailers.

When it comes to the Nebraska Form 6, a document crucial for the sales/use tax and tire fee statement for motor vehicle and trailer sales, there are common misconceptions that can complicate its filing and understanding. Unraveling these myths can ensure compliance and prevent unintended penalties or oversights during the vehicle buying or selling process.

Misconception 1: Trade-ins always reduce the taxable amount. Many believe that any trade-in vehicle will automatically reduce the taxable sales price of the purchased vehicle. However, the trade-in allowance only applies if the vehicle was titled in the name of the purchaser, except for certain familial allowances (for vehicles titled in the name of the purchaser's parent, guardian, or child). Leased vehicles not owned by the lessee do not qualify for this reduction.

Misconception 2: Sales tax doesn't apply if purchasing from another state. A common myth is that vehicles purchased in another state and brought to Nebraska are exempt from Nebraska sales tax. While it's true that sales tax paid to another state can be credited against Nebraska taxes due, the vehicle is still subject to Nebraska sales or use tax when registered, making sure that no tax loss occurs due to interstate purchases.

Misconception 3: All vehicle sales between private individuals are exempt from sales tax. It's often misunderstood that private sales are automatically exempt from sales tax. However, the Nebraska Department of Revenue requires sales tax on most vehicle transactions, except for specific exemptions like gifts, inheritance, or occasional sales as defined by regulation.

Misconception 4: Exemptions are automatically granted. Some might think that if they qualify for an exemption, it is automatically applied. In reality, purchasers must complete the Nebraska Resale or Exempt Sale Certificate part of the Form 6 and provide adequate documentation to qualify for any exemption. Without proper documentation, the county treasurer, DMV, or other designated officials are authorized to collect the sales tax.

Misconception 5: Late fees are negotiable. A misunderstanding exists that penalties for late payment of sales/use tax and tire fees can be waived or negotiated. The truth is, if these fees are not paid within 30 days of the purchase date, penalty and interest are assessed at the statutory rate, and these fees are not subject to negotiation or waiver by county officials.

Understanding these points and clearing up these misconceptions about the Nebraska Form 6 can help ensure that both buyers and sellers of motor vehicles and trailers comply with Nebraska tax laws, thereby avoiding unnecessary penalties and ensuring a smooth transaction process.

Filling out and using the Nebraska 6 form correctly is crucial for buyers and sellers of motor vehicles and trailers in Nebraska to ensure compliance with sales/use tax and tire fee statements. Here are key takeaways to guide you through the process:

Adherence to these guidelines ensures lawful compliance with Nebraska's taxation requirements on motor vehicle and trailer sales, avoiding potential legal and financial penalties for all parties involved.

Nebraska Sales Tax Filing - Includes sections for detailing the purchased vehicle or trailer and any trade-in vehicle contributions.

Nebraska Form 33 - The form’s layout helps taxpayers calculate their underpayments or overpayments for each quarter, showing adjustments needed for correct penalty calculation.