Fill a Valid Nebraska 706N Form

Fill a Valid Nebraska 706N Form

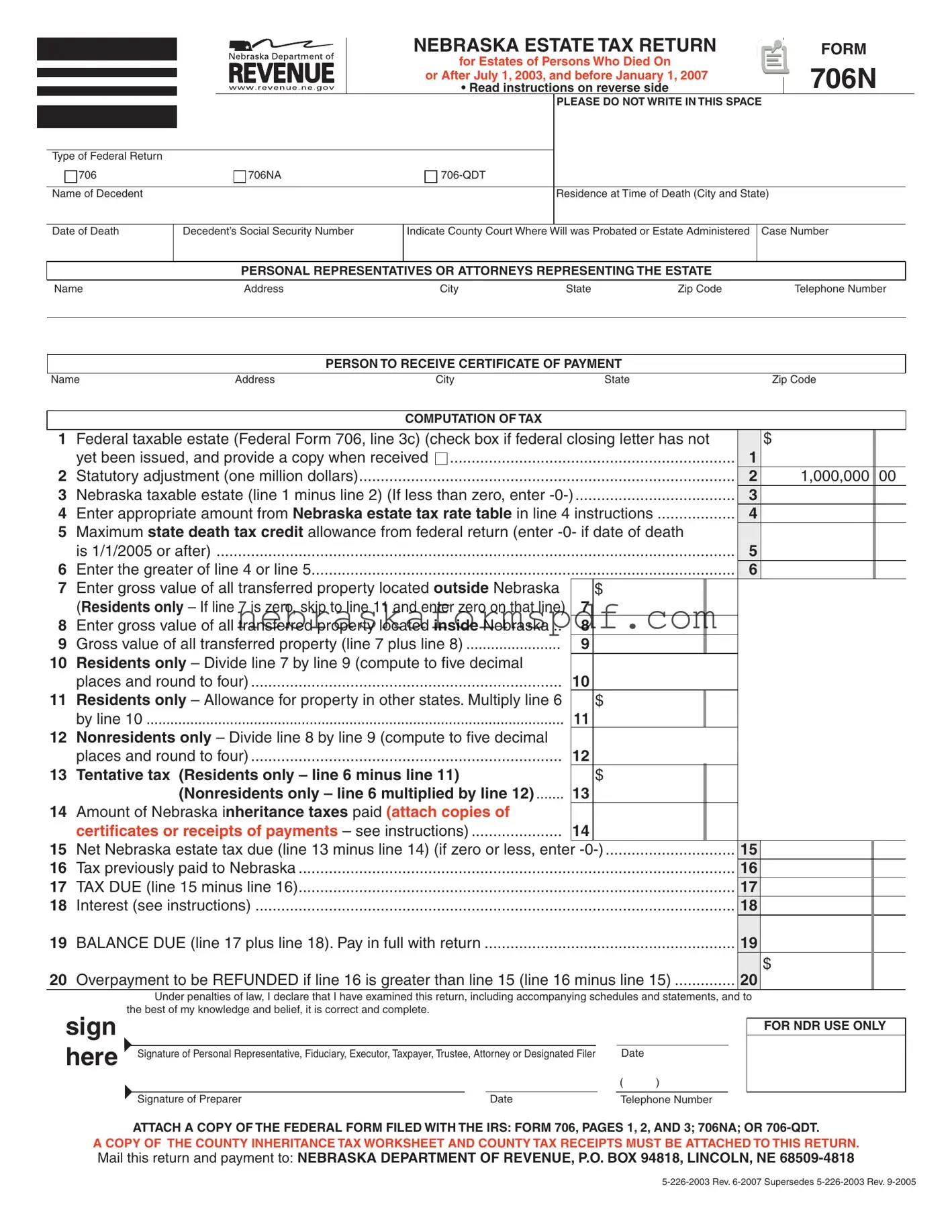

Navigating the complexities of estate taxation in Nebraska for any person dealing with the estate of someone who passed away between July 1, 2003, and January 1, 2007, involves understanding the Nebraska 706N Estate Tax Return. This form is imperative for estates that reach a federal taxable value of one million dollars or more, requiring meticulous attention to detail for both residents of Nebraska and those owning property within the state at the time of death. Its detailed sections demand input ranging from the decedent's basic information, including Social Security Number and date of death, to intricate financial details that calculate the estate's tax due in Nebraska. It entails declarations from personal representatives or attorneys, determinations of the federal taxable estate, adjustments for state taxation, and considerations for property distributed both within and outside Nebraska. The final tax computation acknowledges payments already made, whether through estimated taxes or inheritance offsets, culminating in a balance due or refundable overpayment. To ensure compliance and accuracy, the return mandates attachments like federal estate tax forms and evidence of any inheritance tax payments made to Nebraska counties. This form underscores the importance of understanding Nebraska's specific estate tax requirements, the strategic implications of federal estate taxation, and the need for precise documentation and timely filing with the Nebraska Department of Revenue.

NEBRASKAESTATETAXRETURN

forEstatesofPersonsWhoDiedOn

orAfterJuly1,2003,andbeforeJanuary1,2007

•Readinstructionsonreverseside

FORM

706N

PLEASEDONOTWRITEINTHISSPACE

TypeofFederalReturn

|

706 |

706NA |

|

|

|

|

|

NameofDecedent |

|

ResidenceatTimeofDeath(CityandState) |

|

DateofDeath

Decedent’sSocialSecurityNumber

IndicateCountyCourtWhereWillwasProbatedorEstateAdministered CaseNumber

|

PERSONALREPRESENTATIVESORATTORNEYSREPRESENTINGTHEESTATE |

|

|||

|

|

|

|

|

|

Name |

Address |

City |

State |

ZipCode |

TelephoneNumber |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

PERSONTORECEIVECERTIFICATEOFPAYMENT |

|

|

|

|

Name |

Address |

City |

State |

|

ZipCode |

|

|

|

|

|

|

|

|

|

|

COMPUTATIONOFTAX |

|

|

|

|

|

|

|

|||

1 Federaltaxableestate(FederalForm706,line3c)(checkboxiffederalclosingletterhasnot |

|

$ |

||||

|

yetbeenissued,andprovideacopywhenreceived |

1 |

|

|||

|

.......................................................................................2 Statutoryadjustment(onemilliondollars) |

2 |

1,000,000 00 |

|||

|

.....................................3 |

3 |

|

|||

|

..................4 EnterappropriateamountfromNebraskaestatetaxratetableinline4instructions |

4 |

|

|||

5

|

is1/1/2005orafter) |

5 |

|

|

..................................................................................................6 Enterthegreaterofline4orline5 |

6 |

|

|

7 EntergrossvalueofalltransferredpropertylocatedoutsideNebraska |

$ |

|

|

8 EntergrossvalueofalltransferredpropertylocatedinsideNebraska.. |

|

8 |

|

9 Grossvalueofalltransferredproperty(line7plusline8) |

|

9 |

10

|

placesandroundtofour) |

|

10 |

|

11 |

$ |

|

|

byline10 |

11 |

|

12

|

placesandroundtofour) |

12 |

|

|

|

|

|

||

|

13 Tentativetax |

|

$ |

|

|

|

|

|

|

|

|

13 |

|

|

|

|

|

||

14 AmountofNebraskainheritancetaxespaid(attachcopiesof |

|

|

|

|

|

|

|

||

|

|

14 |

|

|

|

|

|

||

|

15 NetNebraskaestatetaxdue(line13minusline14)(ifzeroorless,enter |

|

|

15 |

|

|

|||

|

.....................................................................................................16 TaxpreviouslypaidtoNebraska |

|

|

|

16 |

|

|

||

|

.....................................................................................................17 TAXDUE(line15minusline16) |

|

|

|

17 |

|

|

||

|

...............................................................................................................18 Interest(seeinstructions) |

|

|

|

18 |

|

|

||

|

19 BALANCEDUE(line17plusline18).Payinfullwithreturn |

|

|

|

19 |

|

|

||

|

20 OverpaymenttobeREFUNDEDifline16isgreaterthanline15(line16minusline15) |

20 |

$ |

|

|||||

|

|

||||||||

sign here

Underpenaltiesoflaw,IdeclarethatIhaveexaminedthisreturn,includingaccompanyingschedulesandstatements,andto thebestofmyknowledgeandbelief,itiscorrectandcomplete.

FORNDRUSEONLY

SignatureofPersonalRepresentative,Fiduciary,Executor,Taxpayer,Trustee,AttorneyorDesignatedFiler |

|

Date |

||

|

|

|

|

( ) |

|

|

|

|

|

SignatureofPreparer |

|

Date |

TelephoneNumber |

|

ACOPYOFTHECOUNTYINHERITANCETAXWORKSHEETANDCOUNTYTAXRECEIPTSMUSTBEATTACHEDTOTHISRETURN.

INSTRUCTIONS |

||

WHOMUSTFILE.This return must be filed for estates with a federal |

or his or her successors or assigns is entitled to a refund of the amount |

|

taxable estate of one million dollars or more, whether or not required to |

of overpayment plus interest. |

|

file Federal Forms 706, 706NA, or |

Interest on refunds will be calculated at the statutory rate. |

|

on or after July 1, 2003, and before January 1, 2007, and was a resident |

SPECIFICINSTRUCTIONS |

|

of Nebraska, or owned real property in Nebraska, at the time of death. |

||

|

||

Estates of persons who died on or after January 1, 2003, but before July 1, 2003, should use Nebraska Form

WHENANDWHERETOFILE.This return is due 12 months after the date of death of the decedent. This return is to be filed with the Nebraska Department of Revenue, P.O. Box 94818, Lincoln, Nebraska

HAVEQUESTIONS?Check our Web site: www.revenue.ne.gov or call

AMOUNTOFTAX.The amount of estate tax due the state of Nebraska begins with the greater of two amounts. The first amount is the maxi- mum state tax credit allowance upon the tax imposed by Chapter 11 of the Internal Revenue Code. (Note: This allowance has been completely phased out on the federal return for decedents with dates of death after December 31, 2004.) The second amount is the Nebraska taxable estate (federal taxable estate [Federal Form 706 line 3c] minus one million dollars) multiplied by the tax rates in the Nebraska estate tax table — see line 4 instructions. Certain adjustments are allowed as reflected in lines 7 through 14. The net Nebraska estate tax due as a result of these calcula- tions is entered on line 15.

INTEREST.If the tax due as computed on line 15 of this return is not paid by the prescribed due date, interest on the unpaid tax will be assessed at the statutory rate from the due date until payment is received. The rate of interest may be adjusted on January 1 of every

FEDERALRETURNS. Attach to this return a copy of Federal Form 706 (pages 1, 2, and 3), 706NA, or

FEDERAL CLOSING LETTER. If a federal return is required to be filed attach a copy of the Internal Revenue Service or federal court determination of estate tax, i.e., the federal closing letter which sets out the federal estate tax liability. If the determination is unavailable, the box on line 1 must be checked. When the closing letter is issued by the Internal Revenue Service or the federal court, a copy of the determination must be filed with the Nebraska Department of Revenue by the personal representative within ten days of receipt.

CERTIFICATEEVIDENCINGPAYMENT.A certificate evidencing payment of Nebraska estate tax will be issued after the Nebraska Estate Tax Return has been filed and the tax paid. The Nebraska Estate Tax Return has not been properly filed until the federal closing letter (if any) and certificates or receipts evidencing tax payments to other states or political subdivisions have been provided.

INHERITANCETAXWORKSHEET.Attach a copy of the inheritance tax worksheet filed with the appropriate Nebraska county court.

AMENDEDRETURN.If the amount of Nebraska tax due is affected by a change made by the Internal Revenue Service or otherwise by the filing of an amended federal return, then an amended Nebraska return must be filed. Complete Form 706N, mark it “Amended” at the top of the return, and attach a copy of the dated notice of change from the Internal Revenue Service or a copy of the amended federal return.

REFUNDOFOVERPAYMENT.An overpayment of tax to the state of Nebraska will be refunded upon the filing of an amended return. The claim for refund must be filed with the department within four years after the date of overpayment, or within one year of a change in the amount of federal tax due, whichever is later. The party making such overpayment

|

Nebraskataxableestate |

|

|

|

OfExcess |

|||

|

fromline3 |

|

|

|

|

|

Over |

|

|

Atleast |

Butlessthan |

|

Tax= |

+ % |

|

|

|

$ |

0 |

$ |

100,000 |

$ |

0 |

5.6 |

$ |

0 |

|

100,000 |

|

500,000 |

|

5,600 |

6.4 |

|

100,000 |

|

500,000 |

|

1,000,000 |

|

31,200 |

7.2 |

|

500,000 |

|

1,000,000 |

|

1,500,000 |

|

67,200 |

8.0 |

|

1,000,000 |

|

1,500,000 |

|

2,000,000 |

|

107,200 |

8.8 |

|

1,500,000 |

|

2,000,000 |

|

2,500,000 |

|

151,200 |

9.6 |

|

2,000,000 |

|

2,500,000 |

|

3,000,000 |

|

199,200 |

10.4 |

|

2,500,000 |

|

3,000,000 |

|

3,500,000 |

|

251,200 |

11.2 |

|

3,000,000 |

|

3,500,000 |

|

4,000,000 |

|

307,200 |

12.0 |

|

3,500,000 |

|

4,000,000 |

|

5,000,000 |

|

367,200 |

12.8 |

|

4,000,000 |

|

5,000,000 |

|

6,000,000 |

|

495,200 |

13.6 |

|

5,000,000 |

|

6,000,000 |

|

7,000,000 |

|

631,200 |

14.4 |

|

6,000,000 |

|

7,000,000 |

|

8,000,000 |

|

775,200 |

15.2 |

|

7,000,000 |

|

8,000,000 |

|

9,000,000 |

|

927,200 |

16.0 |

|

8,000,000 |

|

9,000,000 |

|

|

1,087,200 |

16.8 |

|

9,000,000 |

|

LINE7.Enter the gross value of the transferred property located outside Nebraska.

For a resident decedent, this is the value of real estate and tangible personal property located outside of Nebraska.

For a nonresident decedent, this is the entire value of his or her estate, less the value of any interest in Nebraska real estate and tangible personal property located within Nebraska. Intangibles held in Nebraska at the time of a nonresident’s death are to be valued at their fair market value and included on line 7.

Residentsonly – If the gross value of the transferred property located outside Nebraska is zero, skip to line 11 and enter zero on that line. If line 7 is greater than zero, however, complete lines 8 through 10 before proceeding to line 11. Use line 9 instructions for assistance in determining the appropriate gross value amounts.

LINE8. Enter the gross value of all transferred property within Nebraska. This includes a nonresident decedent’s interest in Nebraska real estate and tangible personal property.

LINE9.Enter the gross value of all transferred property. This amount is the total gross estate reported on the federal return. This gross amount is prior to any adjustments for expenses or any other allowable deductions used in computing the taxable estate.

LINE14.Attach a copy of the county inheritance tax worksheet and copies of receipts or certificates evidencing payment of inheritance tax.

LINE 19. Attach a check or money order payable to the Nebraska Department of Revenue for the sum reported on line 19.

SIGNATURES.A personal representative, fiduciary, executor, taxpayer, trustee, attorney, or designated filer of the estate must sign this return. An attorney must indicate the state wherein currently qualified to practice law. If another person is authorized to sign this return, there must be a power of attorney on file with the department.

Any person who is paid for preparing this return must also sign the return as preparer.

| Fact Name | Detail |

|---|---|

| Form Number | Nebraska Form 706N |

| Purpose | Nebraska Estate Tax Return for estates of persons who died on or after July 1, 2003, and before January 1, 2007 |

| Filing Requirement | Required for estates with a federal taxable estate of one million dollars or more, regardless of the need to file Federal Forms 706, 706NA, or 706-QDT |

| Filing Deadline | Due 12 months after the date of the decedent's death |

| Filing Address | Nebraska Department of Revenue, P.O. Box 94818, Lincoln, Nebraska 68509-4818 |

| Governing Law | Nebraska, as based on the requirements setting forth the estate tax calculations and payments |

| Interest on Unpaid Tax | Assessed at the statutory rate from the due date until payment is received |

| Attachments Required | Copy of Federal Form 706, 706NA, or 706-QDT that was filed with the IRS. If not required to file a federal return, a pro forma Federal Form 706 must be prepared and filed. |

| Amended Returns | Required if the Nebraska tax due is affected by a change made by the IRS or by the filing of an amended federal return |

| Refund of Overpayment | Granted upon filing of an amended return if tax to the state of Nebraska was overpaid |

Filling out the Nebraska 706N form requires careful attention to detail and accuracy. This step-by-step guide aims to simplify the process, ensuring that each section is completed correctly. By following these instructions, you can help ensure the estate is compliant with Nebraska's regulations. Remember, this form is utilized for estates of individuals who passed away within a specific time frame and involves computing taxes based on the estate's value and other significant factors. Don't rush through this process; take your time to gather all necessary information before starting.

Completing the Nebraska 706N form might appear daunting at first, but breaking it down into manageable steps can make the process much smoother. Ensure all information provided is accurate and all necessary documents are attached before sending the form to avoid any delays or issues with the estate’s tax obligations.

The Nebraska 706N form must be filed for estates with a federal taxable estate of one million dollars or more, regardless of whether a Federal Form 706, 706NA, or 706-QDT is required. This applies to decedents who passed away on or after July 1, 2003, and before January 1, 2007, and who were either residents of Nebraska at the time of death or owned real property in Nebraska.

This form is due 12 months after the decedent's date of death. It should be filed with the Nebraska Department of Revenue at P.O. Box 94818, Lincoln, Nebraska 68509-4818. Timely filing is crucial to avoid potential penalties and interest charges on any tax due.

When filing the Nebraska 706N form, several pieces of information and documents are required, including:

It's also important to attach a pro forma Federal Form 706 if a federal return is not required to be filed, and promptly send in a copy of the federal closing letter if it is not available at the time the Nebraska 706N is filed.

Calculating the tax on the Nebraska 706N form starts with the greater of two amounts:

The final tax amount is the net Nebraska estate tax due, which can be further adjusted by accounting for any Nebraska inheritance taxes paid, tax previously paid to Nebraska, and any interest due on late payments or adjustments.

When filing the Nebraska 706N Estate Tax Return, individuals often make errors that can lead to processing delays or incorrect tax calculations. Understanding these pitfalls can help filers to avoid them. Here are nine commonly observed mistakes:

Furthermore, individuals should pay attention to:

By avoiding these common pitfalls, filers can ensure a smoother and more accurate process in fulfilling their Nebraska estate tax obligations.

When handling the responsibilities and documentation for an estate in Nebraska, particularly for individuals who passed away between July 1, 2003, and January 1, 2007, the Nebraska 706N form serves as a vital piece of the puzzle. However, it's not the only document that individuals dealing with estate matters may need to be familiar with. Several other forms and documents often accompany the Nebraska 706N form to ensure the process is completed comprehensively.

Each document serves its specific role in the intricate process of settling an estate, from determining tax liabilities to transferring assets. For those navigating this landscape, understanding the purpose and requirements of each form can significantly streamline estate administration and ensure compliance with both state and federal regulations.

The Nebraska 706N form, primarily for estate tax return purposes for specific decedents, bears resemblance to a few other significant documents in both scope and necessity for estate processing. These documents include the Federal Form 706, Nebraska Form 706N-GST for generation-skipping transfers, and various state-specific estate or inheritance tax returns. Each of these forms serves a unique role in the legal and financial processing of an individual's estate, reflecting adjustments, tax calculations, and allowances based on jurisdiction and specific circumstances of the estate.

Firstly, the Federal Form 706 is directly referenced within the Nebraska 706N instructions, emphasizing its integral role in determining the estate's federal taxable estate, which is crucial for completing the state version. Federal Form 706 is utilized for reporting the estate and calculating the federal estate tax due for decedents. It forms the basis from which the Nebraska 706N operates, requiring information on the federal taxable estate to accurately calculate state taxes owed. This close relationship underlines the interconnectedness of state and federal estate tax obligations, ensuring that estates meet requirements at both levels.

Additionally, the Nebraska Form 706N-GST, aimed at reporting generation-skipping transfer taxes for Nebraska residents, parallels the 706N in its design to address specific taxable events post-death. While the 706N focuses on the broader estate tax implications, the 706N-GST zeroes in on generation-skipping transfers, suggesting a specialized approach within the same framework. This form captures situations where wealth bypasses a direct generation, a nuanced area of estate planning that reflects the complexity and breadth of tax law as it applies to inheritance.

Lastly, other state-specific estate or inheritance tax returns offer a comparative perspective on how different jurisdictions handle post-death tax assessments. Just as the Nebraska 706N form dictates the procedure and requirements for estates within Nebraska, similar documents in other states cater to their local laws and guidelines. This variation underscores the diversity of estate taxation across the United States, with each state formulating its rules within the broader context of federal stipulations. The collaborative and sometimes complex interplay between state-specific and federal requirements reflects the tailored approach needed to navigate estate taxation effectively.

When completing the Nebraska 706N Estate Tax Return, accuracy and attention to detail are crucial. Below is a compiled list of essential dos and don'ts to guide you through the process:

Meticulously following these dos and don'ts can help ensure that the filing process is as smooth and error-free as possible. Always remember to check the revenue department's website or contact their office directly for any updates or further assistance.

When it comes to estate planning and the settling of estates, understanding the intricacies of tax forms is crucial yet can be confusing. One such form, the Nebraska 706N form, designed for the estates of persons who passed away between July 1, 2003, and January 1, 2007, comes with its own set of complexities. Let's clear up four common misconceptions about this particular form.

Addressing these misconceptions ensures that representatives of estates are better informed, leading to smoother and more accurate estate tax filings. Remember, when in doubt, seeking professional advice or consulting with the Nebraska Department of Revenue can help clarify these and other complex aspects.

Filling out and submitting the Nebraska 706N form is a crucial step in managing the estate of someone who passed away between July 1, 2003, and before January 1, 2007. Here are six key takeaways to ensure the process is handled correctly:

Given the detailed process and specific requirements, ensuring accuracy when filling out and submitting the Nebraska 706N form is paramount. Careful adherence to the instructions and deadlines will help streamline the estate tax process in Nebraska.

Nebraska 1040n - Streamline your interactions with the Nebraska Department of Revenue by detailing a designated attorney-in-fact on Form 33 to act on your tax-related matters.

Nebraska Medicaid Enrollment - The MLTC-62 form is required for disclosing ownership and controlling interests in Nebraska healthcare entities.