Fill a Valid Nebraska Sales Tax Form

Fill a Valid Nebraska Sales Tax Form

In navigating the complexities of Nebraska's sales tax, the Nebraska Sales Tax form stands out as a crucial document designed for the purposes of claiming exemptions. This form, specifically Form 13, is meticulously structured to cater to various exemptions, including purchases for resale, exempt purchases, and particular provisions for contractors. Individuals or entities engaged in purchasing goods or services for resale can utilize Section A of the form to declare their intent, thereby exempting these purchases from Nebraska sales tax provided they are operating within the delineated parameters as a wholesalanufacturer, or lessor, among others. For purchases that fall under exempt categories, Section B offers a pathway to elucidate the basis of such exemptions, spanning a range of categories laid out in the instructions. Moreover, contractors find a tailored section, Section C, designed to simplify the exemption process for purchases related to building materials or fixtures, highlighting the form's versatility in addressing distinct needs. This form not only mandates detailed information about the purchases and the purchasers but also embeds stringent penalties for misuse, emphasizing the gravity of accuracy and honesty in its completion. By offering a comprehensive framework for exemption claims, the Nebraska Sales Tax form plays a pivotal role in the state's tax administration, ensuring both compliance and facilitation for eligible sales tax exemptions.

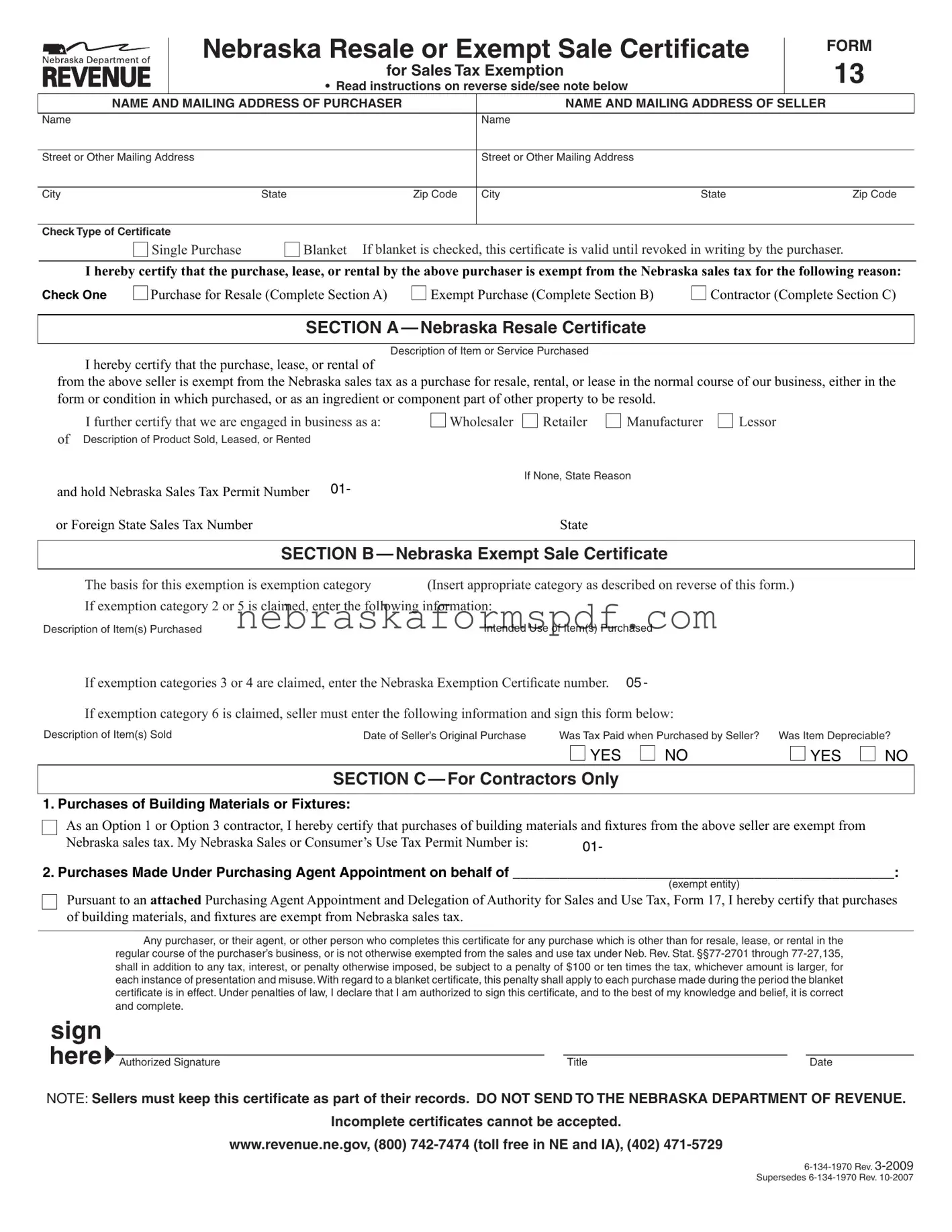

Nebraska Resale or Exempt Sale Certificate

for Sales Tax Exemption

• Readinstructionsonreverseside/seenotebelow

FORM

13

NAME AND MAILING ADDRESS OF PURCHASER |

NAME AND MAILING ADDRESS OF SELLER |

|

|

Name |

Name |

Street or Other Mailing Address

Street or Other Mailing Address

City |

State |

Zip Code |

City |

State |

Zip Code |

Check Type of Certificate

Single Purchase

Blanket If blanket is checked, this certiicate is valid until revoked in writing by the purchaser.

Blanket If blanket is checked, this certiicate is valid until revoked in writing by the purchaser.

I hereby certify that the purchase, lease, or rental by the above purchaser is exempt from the Nebraska sales tax for the following reason:

Check One |

Purchase for Resale (Complete Section A) |

Exempt Purchase (Complete Section B) |

Contractor (Complete Section C) |

SECTION A — Nebraska Resale Certificate

Description of Item or Service Purchased

I hereby certify that the purchase, lease, or rental of

from the above seller is exempt from the Nebraska sales tax as a purchase for resale, rental, or lease in the normal course of our business, either in the form or condition in which purchased, or as an ingredient or component part of other property to be resold.

I further certify that we are engaged in business as a:

of Description of Product Sold, Leased, or Rented

Wholesaler

Retailer

Manufacturer

Lessor

|

If None, State Reason |

and hold Nebraska Sales Tax Permit Number 01- |

|

or Foreign State Sales Tax Number |

State |

|

|

SECTION B — Nebraska Exempt Sale Certificate |

|

|

|

The basis for this exemption is exemption category |

(Insert appropriate category as described on reverse of this form.) |

If exemption category 2 or 5 is claimed, enter the following information:

Description of Item(s) Purchased |

Intended Use of Item(s) Purchased |

If exemption categories 3 or 4 are claimed, enter the Nebraska Exemption Certiicate number. 05 -

If exemption category 6 is claimed, seller must enter the following information and sign this form below:

Description of Item(s) Sold |

Date of Seller’s Original Purchase |

Was Tax Paid when Purchased by Seller? |

Was Item Depreciable? |

YES

YES

NO |

YES |

NO

SECTION C — For Contractors Only

1.purchasesofbuildingmaterialsorfixtures:

As an Option 1 or Option 3 contractor, I hereby certify that purchases of building materials and ixtures from the above seller are exempt from

Nebraska sales tax. My Nebraska Sales or Consumer’s Use Tax Permit Number is: |

01- |

2.purchasesmadeunderpurchasingagentappointmentonbehalfof_________________________________________________:

(exempt entity)

Pursuant to an attached Purchasing Agent Appointment and Delegation of Authority for Sales and Use Tax, Form 17, I hereby certify that purchases of building materials, and ixtures are exempt from Nebraska sales tax.

Any purchaser, or their agent, or other person who completes this certificate for any purchase which is other than for resale, lease, or rental in the regular course of the purchaser’s business, or is not otherwise exempted from the sales and use tax under Neb. Rev. Stat.

sign

here |

|

|

|

|

|

Authorized Signature |

|

Title |

|

Date |

NOTE: Sellersmustkeepthiscertiicateaspartoftheirrecords. DonotSenDtothenebRaSkaDepaRtmentofRevenue.

Incompletecertiicatescannotbeaccepted.

INSTRUCTIONS

Who maY ISSue a ReSaLe CeRtIfICate. Form 13, |

(3) a statement of basis for exemption including completion of all |

||

Section A, is to be issued by persons or organizations making |

information for the basis chosen, (4) the signature of an authorized |

||

purchases of property or taxable services in the normal course of |

person, and (5) the date the certiicate was issued. |

||

their business for the purpose of resale either in the form or condition |

penaLtIeS.Any purchaser who gives a Form 13 to a seller for |

||

in which it was purchased, or as an ingredient or component part of |

|||

any purchase which is other than for resale, lease, or rental in the |

|||

other property. |

|||

normal course of the purchaser’s business, or is not otherwise |

|||

Who maY ISSue an eXempt SaLe CeRtIfICate. |

exempted from sales and use tax under the Nebraska Revenue Act, |

||

Form 13, Section B can only be issued by persons or organizations |

shall be subject to a penalty of $100 or ten times the tax, whichever |

||

exempt from payment of the Nebraska sales tax by qualifying for |

amount is larger, for each instance of presentation and misuse. |

||

one of the six enumerated Categories of Exemption (see below). |

Any purchaser, or their agent, who fraudulently signs a Form 13 |

||

Nonprofit organizations that have a 501(c) designation and are |

may be found guilty of a Class IV misdemeanor. |

||

exempt from federal and state income tax are not automatically |

|

CATEGORIES OF EXEMPTION |

|

exempt from sales tax. Only the entities listed in the referenced |

|

||

1. Purchases made directly by certain governmental agencies |

|||

regulations are exempt from paying Nebraska sales tax on their |

|||

purchases when the exemption certiicate is properly completed and |

identiied in Nebraska Sales and Use Tax |

||

provided to the seller. Organizations claiming a sales tax exemption |

|||

may do so only on items purchased for their own use. For health care |

and |

||

organizations, the exemption is limited to the speciic level of health |

A list of speciic governmental units are provided in the above |

||

care they are licensed for. The exemption is not issued to the entire |

regulations. Governmental units are not assigned exemption |

||

organization when multiple levels of health care or other activities are |

numbers. |

|

|

provided or owned by the organization. Items purchased by an exempt |

Sales to the United States government, its agencies, and |

||

organization that will be resold must be supported by a properly |

corporations wholly owned by the United States government are |

||

completed Nebraska Resale Certiicate, Form 13, Section A. |

exempt from sales tax. However, sales to institutions chartered |

||

Indicate the category which properly relects the basis for your |

or created under federal authority, but which are not directly |

||

exemption. Place the corresponding number in the space provided |

operated and controlled by the United States government for the |

||

in Section B. If category 2 through 6 is the basis for exemption, you |

beneit of the public, generally are taxable. Construction projects |

||

must complete the information requested in Section B. |

for federal agencies have speciic requirements, see |

||

Nebraska Sales and Use Tax |

Contractors. |

||

Purchases that are not exempt from Nebraska sales and use tax |

|||

Certificate, and |

|||

include, but are not limited to, governmental units of other states, |

|||

additional information on the proper issuance and use of this |

|||

sanitary and improvement districts, urban renewal authorities, |

|||

certificate. These and other regulations referred to in these |

|||

rural water districts, railroad transportation safety districts, and |

|||

instructions are available on our Web site: www.revenue.ne.gov/ |

|||

county historical or agricultural societies. |

|||

legal/regs/slstaxregs. |

|||

2. Purchases when the intended use renders it exempt as set out |

|||

Use Form 13E for purchases of energy sources which qualify for |

|||

in paragraph 012.02D of |

|||

exemption. Use Form 13ME for purchases of mobility enhancing |

|||

the description of the item purchased and the intended use as |

|||

equipment on a motor vehicle. |

|||

required on the front of Form 13. Sellers of repair parts for |

|||

ContRaCtoRS.Form 13, Section C, Part 1, must be completed |

|||

agricultural machinery and equipment cannot accept a Form 13 |

|||

by contractors operating under Option 1 or Option 3 to document |

to exempt such sales from tax. |

||

their |

3. Purchases made by organizations that have been issued a |

||

suppliers. Section C, Part 2, may be completed to exempt the |

|||

Nebraska |

Exempt Organization - Certiicate of Exemption are |

||

purchase of building materials or ixtures pursuant to a Purchasing |

|||

exempt from sales tax. |

|||

Agent Appointment, Form 17. See the contractor information guides |

|||

on our Web site www.revenue.ne.gov for additional information. |

|||

Institutions, identify such organizations. These organizations will |

|||

|

|||

WheReto fILe. Form 13 is given to the seller at the time of |

be issued a Nebraska state exemption identiication number. This |

||

the purchase of the property or service or when sales tax is due. |

exemption number must be entered in Section B of the Form 13. |

||

The certiicate must be retained with the seller’s records for audit |

4. Purchases of common or contract carrier vehicles and repair and |

||

purposes. Do not send to the Department of Revenue. |

replacement parts for such vehicles. |

||

SALES TAX NUMBER. A purchaser who completes Section A |

5. Purchases |

of manufacturing machinery or equipment by |

|

and is engaged in business as a wholesaler or manufacturer is |

a taxpayer engaged in business as a manufacturer for use |

||

not required to provide an identification number. |

predominantly in manufacturing. This includes the installation, |

||

purchasers can provide their home state sales tax number. Section B |

repair, or maintenance of such qualiied manufacturing machinery |

||

does not require an identification number when exemption |

or equipment (see Revenue Ruling |

||

category 1, 2, or 5 is indicated. |

6. A sale that qualiies as an occasional sale, such as a sale of |

||

pRopeRLY CompLeteD CeRtIfICate. A purchaser |

|||

depreciable machinery and equipment productively used by the |

|||

must complete a certificate before issuing it to the seller. To |

seller for more than one year and the seller previously paid tax on |

||

properly complete the certificate, the purchaser must include: |

the item. The seller must sign and give the exemption certiicate |

||

(1) identiication of the purchaser and seller, (2) a statement whether |

to the purchaser. The certiicate must be retained by the purchaser |

||

the certiicate is for a single purchase or is a blanket certiicate, |

for audit purposes (see |

||

| Fact Number | Fact Description |

|---|---|

| 1 | The form serves as a certificate for sales tax exemption in Nebraska under specific conditions. |

| 2 | It includes different sections (A, B, C) for various exemptions such as resale, exempt purchases, and contractor purchases. |

| 3 | Section A is specific for purchases intended for resale, rental, or lease as a part of the purchaser's business operations. |

| 4 | Section B caters to exempt purchases, requiring details depending on the exemption category selected. |

| 5 | Contractors use Section C for building materials or fixtures purchases that are exempt from sales tax. |

| 6 | The form must be completely filled and retained by the seller for records, but not sent to the Nebraska Department of Revenue. |

| 7 | Misuse or fraudulent use of the form may result in penalties, including a $100 fine or ten times the tax amount per incident. |

| 8 | It is governed by the Nebraska Revenue Act, specifically Neb. Rev. Stat. §§77-2701 through 77-27,135 and associated sales and use tax regulations. |

Filling out the Nebraska Sales Tax form, specifically the Form 13, is an essential process for entities making tax-exempt purchases within Nebraska. This includes purchases for resale, those made by exempt organizations, and items bought by contractors for use in construction that meet specific tax exemption criteria. Proper completion and submission of this form ensure compliance with Nebraska's sales tax regulations, thereby avoiding potential penalties. Here, you'll find a step-by-step guide to accurately fill out the form, whether it's for a single purchase or as a blanket certificate for ongoing transactions.

Following these steps will guide you through the completion of the Nebraska Sales Tax Form 13. This procedure facilitates tax-exempt purchases in compliance with Nebraska tax laws, contributing to the smooth operation of businesses and organizations eligible for tax exemptions. Properly filled-out forms serve as critical documentation for both buyers and sellers, defending their tax-exempt transactions during audits. It's important to periodically review the form for accuracy and to ensure compliance with any changes in tax law.

A Nebraska Sales Tax Exemption Certificate, also referred to as Form 13, allows entities to make tax-exempt purchases of goods and services that are either intended for resale, qualify under specific exempt categories, or are purchased by certain contractors for use in construction. It can be issued by any business or organization making purchases in the normal course of their operations for purposes of resale, lease, or rental as well as by organizations that qualify for exemption under six specific categories due to the nature of their operations or status.

Qualification for a sales tax exemption depends on the nature of your business operation or organizational status. The categories include:

To determine your eligibility, you should review the specific requirements and regulations for each category provided by the Nebraska Department of Revenue.

For the certificate to be considered complete, it must include:

Yes, out-of-state purchasers can use the Nebraska Sales Tax Exemption Certificate, Form 13, particularly when making purchases for resale or for other qualified exempt reasons. While they may not have a Nebraska sales tax permit number, they can provide their home state sales tax number when completing Section A for wholesaler or manufacturer exemptions.

Misusing the exemption certificate for purchases not qualifying under the stated exemptions results in penalties. Such misuse includes, but is not limited to, claiming exemptions for personal purchases not intended for resale or not covered under the six exempt categories. The penalties involve a fine of $100 or ten times the amount of tax due, whichever is larger, for each instance of misuse. Fraudulent misuse of the certificate could additionally lead to a Class IV misdemeanor charge.

A blanket exemption certificate does not have a predefined expiration date and remains valid until it is expressly revoked by the purchaser in writing. This allows for ongoing purchases without the need to issue a new certificate for each transaction. To revoke a certificate, the purchaser must send a written notice to the seller stating their intention to revoke the exemption for future transactions.

Filling out the Nebraska Sales Tax form, specifically the Nebraska Resale or Exempt Sale Certificate, requires attention to detail and a clear understanding of the qualifications for sales tax exemptions. However, individuals often make errors that can compromise the validity of their certificates, resulting in penalties or the denial of tax exemption claims. Here are nine common mistakes:

In summary, users of the Nebraska Resale or Exempt Sale Certificate for Sales Tax Exemption must exercise diligence and precision in completing the form. Each section of the form serves a specific legal purpose, integral to the validation of a claim for sales tax exemption. Avoiding these common mistakes not only ensures compliance with Nebraska tax laws but also safeguards against potential financial penalties.

When handling the complexities of Nebraska sales tax, businesses and tax professionals must navigate a variety of documents that support or correspond to the Nebraska Resale or Exempt Sale Certificate (Form 13). Understanding these forms can aid in compliance and streamline tax processing. Below is a list of documents frequently used alongside Form 13, each critical for different scenarios in tax documentation and reporting.

When completing the Nebraska Sales Tax Exemption form, certain guidelines will help ensure the process is done correctly and efficiently. Here’s a list of things you should and shouldn't do:

Following these guidelines ensures that your sales tax exemption process is both smooth and compliant with Nebraska state laws. Remember, accuracy and thoroughness are key to a successful exemption claim.

Understanding the Nebraska Sales Tax Form, particularly the Resale or Exempt Sale Certificate, can be tricky. Without proper guidance, it's easy to fall victim to common misconceptions. Let's clear up some of these misunderstandings to ensure compliance and avoid unnecessary penalties.

Correcting these misconceptions ensures that organizations and businesses can navigate the complexities of the Nebraska Sales Tax Form more efficiently, enabling them to claim the appropriate exemptions while fulfilling their legal obligations.

Understanding the Nebraska Sales Tax form can be straightforward if you keep these key takeaways in mind:

Navigating Nebraska's Sales Tax Form requires attention to detail and an understanding of your purchase's purpose. Using this guide, you can confidently fill out the form, ensuring compliance and avoiding penalties. Both sellers and buyers have responsibilities in maintaining the correctness and integrity of the information provided.

Dmv Nebraska - Showcase your pride in Nebraska's wildlife with the Mountain Lion Specialty Plate, available for personalization.

Nebraska 1040N - Careful attention to detail is required in completing the form to accurately reflect one’s tax liability and potential refunds.

Nebraska Homestead Exemption - Legal representatives or duly authorized officers of the organization are required to sign the Form 451, validating its contents.