Fill a Valid Nebraska Sales Tax Statement Form

Fill a Valid Nebraska Sales Tax Statement Form

The Nebraska Sales Tax Statement form, a crucial document in the sale and purchase of motor vehicles and trailers, mandates completion by the seller and presentation to the buyer to ensure compliance with sales and use tax laws in Nebraska. It facilitates the collection of necessary taxes and fees, including a tire fee, by outlining pertinent information such as the purchaser's and seller's names and addresses, vehicle description, and trade-in details. Moreover, it calculates the tax base and taxes due, including penalties for late payments. Obtained through the Department or county treasurer, this form serves multiple purposes: supporting tax compliance, detailing exemptions, and penalizing fraudulent claims, which can result in severe legal consequences. Its importance further extends to specific exemptions, like those for disabled persons or vehicles purchased outside Nebraska, providing a comprehensive guide for correctly processing the tax obligations linked to vehicle sales. The form's structure underscores the commitment to a transparent, fair taxation process, echoing the importance of adherence to the state's tax regulations to avoid legal penalties. Additionally, detailed instructions for both buyers and sellers ensure clarity in completing and submitting the form, illustrating the structured approach Nebraska takes to taxation and fee collection in vehicle transactions.

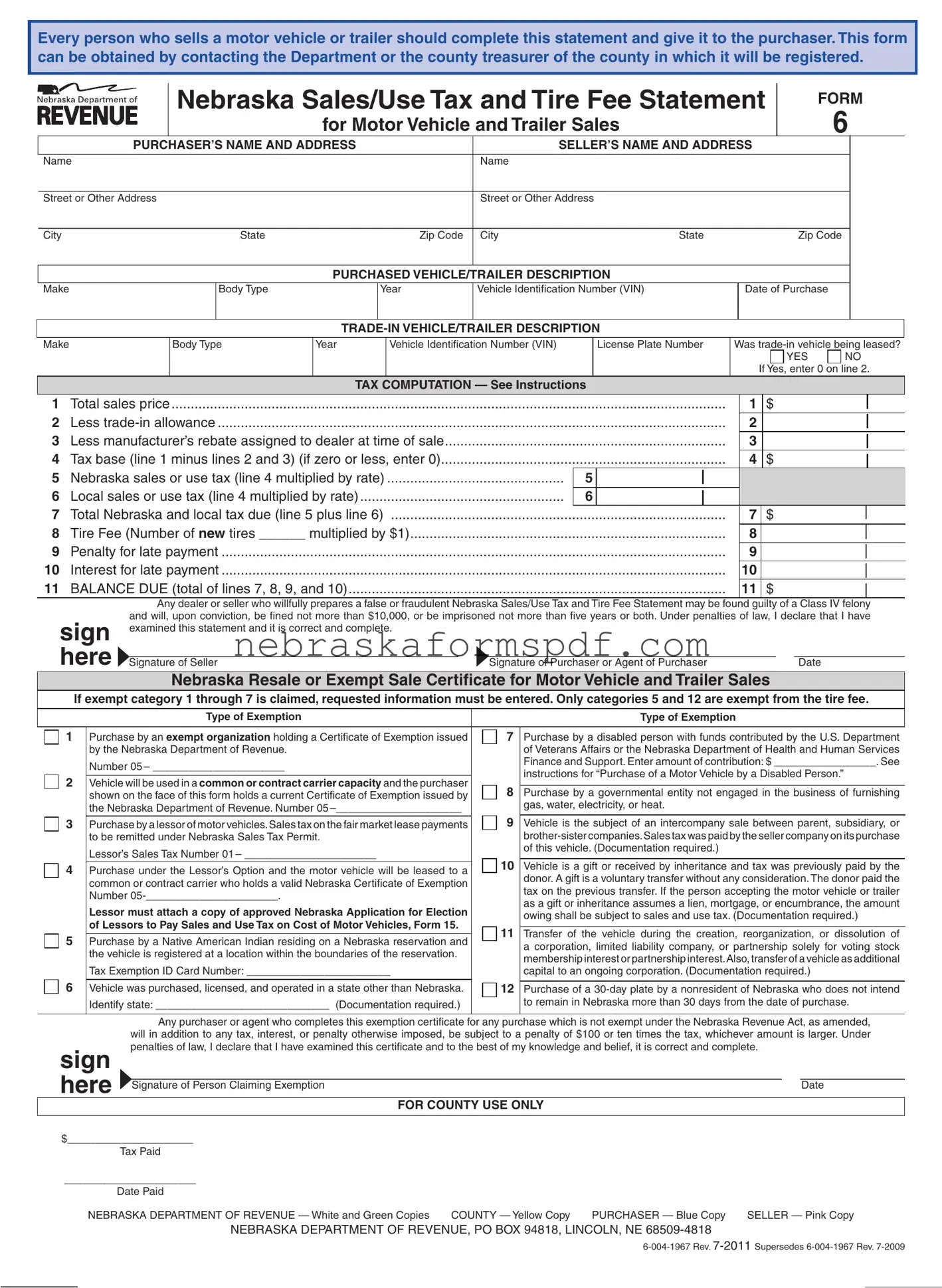

Every person who sells a motor vehicle or trailer should complete this statement and give it to the purchaser. This form can be obtained by contacting the Department or the county treasurer of the county in which it will be registered.

Nebraska Sales/Use Tax and Tire Fee Statement

for Motor Vehicle and Trailer Sales

FORM

6

PURCHASER’S NAME AND ADDRESS |

|

SELLER’S NAME AND ADDRESS |

|

|

||

Name |

|

|

Name |

|

|

|

|

|

|

|

|

|

|

Street or Other Address |

|

|

Street or Other Address |

|

|

|

|

|

|

|

|

|

|

City |

State |

Zip Code |

City |

State |

Zip Code |

|

|

|

|

|

|

|

|

PURCHASED VEHICLE/TRAILER DESCRIPTION

Make |

Body Type |

Year |

Vehicle Identification Number (VIN) |

Date of Purchase |

|

|

|

|

|

|

|

Make

Body Type |

Year |

Vehicle Identification Number (VIN) |

License Plate Number |

Was |

|

|

|

|

|

YES |

NO |

|

|

|

|

If Yes, enter 0 on line 2. |

|

TAX COMPUTATION — See Instructions

1 |

Total sales price |

|

|

1 |

$ |

2 |

Less |

|

|

2 |

|

3 |

Less manufacturer’s rebate assigned to dealer at time of sale |

|

|

3 |

|

4 |

Tax base (line 1 minus lines 2 and 3) (if zero or less, enter 0) |

|

|

4 |

$ |

5 |

Nebraska sales or use tax (line 4 multiplied by rate) |

5 |

|

|

|

6 |

Local sales or use tax (line 4 multiplied by rate) |

6 |

|

|

|

7 |

Total Nebraska and local tax due (line 5 plus line 6) |

|

|

7 |

$ |

8 |

Tire Fee (Number of new tires ______ multiplied by $1) |

|

|

8 |

|

9 |

Penalty for late payment |

|

|

9 |

|

10 |

Interest for late payment |

|

|

10 |

|

11 |

BALANCE DUE (total of lines 7, 8, 9, and 10) |

|

|

11 |

$ |

Any dealer or seller who willfully prepares a false or fraudulent Nebraska Sales/Use Tax and Tire Fee Statement may be found guilty of a Class IV felony and will, upon conviction, be fined not more than $10,000, or be imprisoned not more than five years or both. Under penalties of law, I declare that I have

sign |

examined this statement and it is correct and complete. |

|

|

|

|

|

|

here Signature of Seller |

Signature of Purchaser or Agent of Purchaser |

Date |

|

Nebraska Resale or Exempt Sale Certificate for Motor Vehicle and Trailer Sales

If exempt category 1 through 7 is claimed, requested information must be entered. Only categories 5 and 12 are exempt from the tire fee.

|

|

|

|

|

|

Type of Exemption |

|

|

|

|

|

|

Type of Exemption |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

1 |

Purchase by an exempt organization holding a Certificate of Exemption issued |

7 |

Purchase by a disabled person with funds contributed by the U.S. Department |

|||||||||||

|

|

|

|

by the Nebraska Department of Revenue. |

|

|

|

|

|

of Veterans Affairs or the Nebraska Department of Health and Human Services |

|||||||

|

|

|

|

Number 05 – ______________________ |

|

|

|

|

|

Finance and Support. Enter amount of contribution: $ _________________. See |

|||||||

|

|

|

|

|

|

|

|

|

instructions for “Purchase of a Motor Vehicle by a Disabled Person.” |

||||||||

2 |

|

|

|

|

|

|

|

|

|||||||||

Vehicle will be used in a common or contract carrier capacity and the purchaser |

8 |

||||||||||||||||

|

|

|

|

|

|||||||||||||

Purchase by a governmental entity not engaged in the business of furnishing |

|||||||||||||||||

|

|

|

|

shown on the face of this form holds a current Certificate of Exemption issued by |

|||||||||||||

|

|

|

|

|

|

|

|

gas, water, electricity, or heat. |

|

|

|

||||||

|

|

|

|

the Nebraska Department of Revenue. Number 05 |

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

3 |

Purchase by a lessor of motor vehicles. Sales tax on the fair market lease payments |

9 |

Vehicle is the subject of an intercompany sale between parent, subsidiary, or |

||||||||||||||

|

|

|

|

to be remitted under Nebraska Sales Tax Permit. |

|

|

|

|

|

||||||||

|

|

|

|

Lessor’s Sales Tax Number 01 – ______________________ |

|

|

|

|

|

of this vehicle. (Documentation required.) |

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

4 |

|

|

|

|

|

10 |

Vehicle is a gift or received by inheritance and tax was previously paid by the |

||||||||||

Purchase under the Lessor’s Option and the motor vehicle will be leased to a |

|

||||||||||||||||

|

|

|

|

donor. A gift is a voluntary transfer without any consideration. The donor paid the |

|||||||||||||

|

|

|

|

common or contract carrier who holds a valid Nebraska Certificate of Exemption |

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

tax on the previous transfer. If the person accepting the motor vehicle or trailer |

|||||||||

|

|

|

|

Number |

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

as a gift or inheritance assumes a lien, mortgage, or encumbrance, the amount |

||||||||

|

|

|

|

Lessor must attach a copy of approved Nebraska Application for Election |

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

owing shall be subject to sales and use tax. (Documentation required.) |

|||||||||

|

|

|

|

of Lessors to Pay Sales and Use Tax on Cost of Motor Vehicles, Form 15. |

|

|

|

|

|||||||||

|

|

|

|

|

|

|

11 |

|

|

|

|

|

|||||

|

|

|

5 |

|

|

|

|

|

|

Transfer of |

the vehicle during the creation, |

reorganization, or dissolution of |

|||||

|

|

|

Purchase by a Native American Indian residing on a Nebraska reservation and |

||||||||||||||

|

|

|

|

|

|

|

a corporation, limited liability company, or partnership solely for voting stock |

||||||||||

|

|

|

|

the vehicle is registered at a location within the boundaries of the reservation. |

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

membership interest or partnership interest.Also, transfer of a vehicle as additional |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

Tax Exemption ID Card Number: ________________________ |

|

|

|

|

|

capital to an ongoing corporation. (Documentation required.) |

|||||||

|

|

|

6 |

Vehicle was purchased, licensed, and operated in a state other than Nebraska. |

12 |

Purchase of a |

|||||||||||

|

|

|

|

Identify state: _____________________________ (Documentation required.) |

|

|

|

|

to remain in Nebraska more than 30 days from the date of purchase. |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

Any purchaser or agent who completes this exemption certificate for any purchase which is not exempt under the Nebraska Revenue Act, as amended, |

|||||||||||

|

|

|

|

|

|

will in addition to any tax, interest, or penalty otherwise imposed, be subject to a penalty of $100 or ten times the tax, whichever amount is larger. Under |

|||||||||||

|

|

|

sign |

|

penalties of law, I declare that I have examined this certificate and to the best of my knowledge and belief, it is correct and complete. |

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

here |

|

|

|

|

|

|

|

|

|

|

|

|

||

|

Signature of Person Claiming Exemption |

|

|

|

|

|

|

|

|

|

Date |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

FOR COUNTY USE ONLY |

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||

$_____________________ |

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

Tax Paid |

|

|

|

|

|

|

|

|

|

|

||

______________________ |

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

Date Paid |

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

NEBRASKA DEPARTMENT OF REVENUE — White and Green Copies |

COUNTY — Yellow Copy |

PURCHASER — Blue Copy |

SELLER — Pink Copy |

||||||||||

NEBRASKA DEPARTMENT OF REVENUE, PO BOX 94818, LINCOLN, NE

INSTRUCTIONS FOR PURCHASER

PAYMENT OF TAX AND TIRE FEE. The purchaser of a motor vehicle or trailer must present the white, yellow, and blue copies of this statement to the county treasurer, the Department of Motor Vehicles (DMV), or other designated county oficial within 30 days from the date of purchase, and pay the Nebraska and local sales and use tax, and the tire fee. The date of purchase is the earlier of two dates: the date on the motor vehicle title; or the date of possession, as evidenced by the Nebraska Sales/Use Tax and Tire Fee Statement, Form 6. The purchaser should retain their copy of this statement for a period of at least ive years.

PENALTY AND INTEREST. If the total taxes and tire fee are not paid within 30 days of the purchase date, the county treasurer, DMV, or designated county oficial will assess and collect penalty and interest at the statutory rate. If you have any questions regarding the due date, or penalty and interest rates, please contact your local county treasurer’s ofice or call the Nebraska Department of Revenue (Department),

SALES TAX PAID TO ANOTHER STATE. A motor vehicle purchased in another state, with sales tax properly paid to the other state, but registered for the irst time in Nebraska, is subject to sales or use tax at the time of registration. If the state the vehicle was purchased in has reciprocity with Nebraska, the total sales tax paid in that state will be credited toward the total state and local sales tax due in Nebraska. No refund will be made if the other state’s tax rate exceeds the total Nebraska and local option sales tax rate.

LINE 4. No refund will be made if the tax base results in a negative amount.

EXEMPTIONS. If the transfer of title to the motor vehicle or trailer described on this statement is exempt from sales and use tax, the Nebraska Resale or Exempt Sale Certiicate, located on the front of this statement, must be completed prior to registration.

The purchaser must present documentation that supports the exemption. If the documentation is not suficient, the county treasurer, DMV, or other designated county oficial is authorized to collect the tax. The purchaser may submit a claim to the Department requesting that the taxes and fees paid be refunded.

PURCHASE OF A MOTOR VEHICLE BY A DISABLED PERSON. If the amount contributed by the U.S. Department of VeteransAdministration (VA) or the Nebraska Department of Health and Human Services (DHHS) is the maximum amount allowed by law, the entire purchase price of the motor vehicle is exempt from sales tax. The entire purchase price is exempt, even if the purchase price is greater than the maximum amount contributed. If the contributed amount is less than the maximum amount allowed by law, only the amount contributed is exempt from sales tax. If there is a question as to whether the maximum amount was received, Form

MOBILITY ENHANCING EQUIPMENT. Any disabled or handicapped person who is required to use durable medical equipment or prosthetics for moving from one place to another place, may purchase mobility enhancing equipment with a motor vehicle exempt from sales tax. Please refer to the Nebraska Certiicate of Exemption for Mobility Enhancing Equipment on a Motor Vehicle, Form 13ME.

UNDERPAYMENT OF TAX. Underpayment of sales and use tax or tire fee on this statement must be reported on an Amended Nebraska Sales/Use Tax and Tire Fee Statement for Motor Vehicle and Trailer Sales, Form 6XN. Form 6XN is available at each county treasurer’s ofice and the Department.

INSTRUCTIONS FOR SELLER

LICENSED MOTOR VEHICLE DEALER OR LICENSED PERMIT HOLDER. A motor vehicle dealer, or sales tax permit holder, must complete this statement for every sale of a motor vehicle or trailer. The colored copies should be distributed in the following manner:

1.The pink copy must be retained with your business records;

2.The green copy must be mailed with the Nebraska and Local Sales and Use Tax Return, Form 10; and

3.The white, yellow, and blue copies must be given to the purchaser.

The sales price on line 1 shall include charges for items such as destination charges, import custom fees, surcharges, service and maintenance agreements, document processing charges, charges for warranty transfers, and

INDIVIDUAL WITHOUT A SALESTAX PERMIT. An individual, who is not licensed to collect sales tax, must complete this statement

for every sale of a motor vehicle or trailer. The colored copies should be distributed in the following manner:

1.The pink copy must be retained with your records; and

2.The white, yellow, and blue copies must be given to the purchaser.

An individual can only accept another motor vehicle or trailer as a

LEASED VEHICLES. A lessee cannot use the

TIRE FEE. Motor vehicle dealers selling new motor vehicles, trailers, or

the number of new tires on a

Individuals selling used motor vehicles are not required to indicate the number of tires.

INSTRUCTIONS FOR COUNTY TREASURERS, DMV,

AND OTHER DESIGNATED COUNTY OFFICIALS

COLLECTION OF TAX AND TIRE FEE. The county treasurer,

DMV, or other designated county oficial must collect the state and applicable local sales and use tax, and the tire fee, prior to registering the motor vehicle or trailer.

The white, yellow, and blue copies of this statement must be receipted in the space provided for validation. The blue copy must be returned to the purchaser. The yellow copy must be retained in your iles, and the white copy must be submitted with your monthly returns.

COLLECTION OF PENALTY AND INTEREST. If the appropriate taxes and fees are not paid within 30 days of the purchase date, penalty and interest must be collected at the statutory rate from the due date through the date of payment. If the due date falls on a Saturday, Sunday, or a holiday, the purchaser may still pay the amount due on the next business day without incurring penalty and interest.

NEBRASKA DEPARTMENT OF REVENUE, PO BOX 94818, LINCOLN, NE

| Fact Name | Description |

|---|---|

| Form Purpose | Every person who sells a motor vehicle or trailer must complete this form and provide it to the purchaser. |

| Form Availability | The form can be obtained by contacting the Nebraska Department of Revenue or the county treasurer of the county where the vehicle will be registered. |

| Form Identification | Nebraska Sales/Use Tax and Tire Fee Statement for Motor Vehicle and Trailer Sales, known as FORM 6. |

| Governing Law | The form is governed by Nebraska law pertaining to the sale and taxation of motor vehicles and trailers, including sales tax, use tax, and tire fees. |

| Penalty for False Statement | Any dealer or seller who willfully prepares a false or fraudulent statement may be found guilty of a Class IV felony, facing fines up to $10,000, imprisonment up to five years, or both. |

Completing the Nebraska Sales/Use Tax and Tire Fee Statement for Motor Vehicle and Trailer Sales, commonly referred to as Form 6, is a crucial step in the process of selling a vehicle in Nebraska. This form ensures that sales tax and any applicable tire fees are correctly calculated and paid, helping both the seller and the purchaser to comply with Nebraska's tax laws. The instructions below outline the process to fill out the form correctly, assisting sellers to navigate through the form's sections without any oversight.

Remember, any intentional falsification of this form may result in severe penalties, including being found guilty of a Class IV felony. Carefully reviewing the form for completeness and accuracy before submission is imperative to ensure compliance with Nebraska tax laws.

This form, designated as Form 6, is a document that every seller must complete and provide to the purchaser when selling a motor vehicle or trailer in Nebraska. It serves to calculate and declare the sales/use tax and tire fee applicable to the sale of a motor vehicle or trailer.

The form can be obtained from the Nebraska Department of Revenue or the county treasurer's office in the county where the vehicle will be registered. You may contact these offices directly to request a copy of the form.

The form requires detailed information about both the purchaser and the seller, including names and addresses. It also requires a description of the purchased vehicle/trailer, including make, body type, year, and Vehicle Identification Number (VIN). If there's a trade-in vehicle, details about it must also be provided. Additionally, the form includes sections for tax computation, tire fee, any penalties for late payment, and signatures from both the seller and the purchaser.

Yes, certain purchases may be exempt from sales or use tax under specific conditions, such as purchase by an exempt organization, vehicles used in a carrier capacity, gifts, transfer of vehicles among family businesses for voting stock or additional capital, and vehicles purchased by Native American Indians residing on a reservation. Detailed documentation is required to support any claim for exemption.

If these amounts are not paid within 30 days from the purchase date, the county treasurer, Department of Motor Vehicles (DMV), or other designated county official will assess and collect a penalty and interest at the statutory rate from the purchase date. It's important to ensure timely payment to avoid these additional charges.

Yes, if there was an underpayment or other error in the tax and tire fee reported, an Amended Nebraska Sales/Use Tax and Tire Fee Statement for Motor Vehicle and Trailer Sales, Form 6XN, must be completed. This form is available at county treasurer's offices and the Department of Revenue office. It allows for the correction of previously submitted information and ensures accurate tax and fee payments.

When filling out the Nebraska Sales Tax Statement form, it's important to avoid common pitfalls to ensure a smooth and compliant transaction. Here are some mistakes often made:

Incorrect Purchaser or Seller Information: One of the most common errors is providing incorrect names and addresses for either the purchaser or the seller. Accurate details are crucial for any potential future correspondence or legal purposes.

Vehicle Description Errors: Omitting or incorrectly filling in the vehicle's make, body type, year, or VIN (Vehicle Identification Number) can cause significant issues. These details are vital for registration and identifying the specific vehicle involved in the sale.

Failing to Record Trade-In Details Properly: If a trade-in vehicle is part of the transaction, failing to accurately include its description and whether it was being leased can affect the tax computation. Accurately recording a trade-in can legally reduce the total amount taxed.

Miscalculating Taxes and Fees: Tax computation errors are common and can result from incorrect input on lines 1 through 4 or misunderstanding how to apply local tax rates. Such mistakes can either lead to underpaying or overpaying. None is ideal as they can trigger a tedious correction process.

Missing or Incorrectly Applied Exemptions: Not applying for exemptions where applicable, such as for disabled persons or when a vehicle is purchased by a tax-exempt organization, can unnecessarily increase costs. Equally, claiming an exemption without proper documentation can lead to penalties.

Overlooking the Tire Fee on New Vehicles: The form requires dealers to include a tire fee for new vehicles (including spare tires). This is often overlooked or miscalculated, especially when dealing with used vehicles that have new tires.

These errors can have various consequences, from delays in processing to potential penalties. Therefore, careful completion of the form is essential. Sellers and buyers alike should take their time, double-check all entries, and ensure they understand each section before submission. When in doubt, consulting the instructions provided with the form or seeking professional advice can prevent these common mistakes.

It's also important to remember that both sellers and purchasers have responsibilities under the law when completing this statement. Misrepresentations or errors, whether intentional or accidental, can lead to legal consequences, including fines or other penalties. Thus, honesty and accuracy in completing the Nebraska Sales Tax Statement form cannot be overstated.

When dealing with the process of purchasing or selling a motor vehicle in Nebraska, the Nebraska Sales/Use Tax and Tire Fee Statement for Motor Vehicle and Trailer Sales is a critical document. However, this form often goes hand in hand with various other forms and documents to ensure compliance with the state's legal and fiscal requirements. Below is a brief description of six other forms and documents frequently used alongside the Nebraska Sales Tax Statement form.

Each of these documents plays a vital role in the vehicle transaction process, ensuring that all legal, financial, and regulatory bases are covered. Proper completion and submission of these forms protect both the buyer and seller and ensure the smooth transition of vehicle ownership. It is important for individuals involved in the sale or purchase of a vehicle in Nebraska to be aware of these documents and how they complement the Nebraska Sales Tax Statement form.

The Nebraska Sales Tax Statement form is similar to other state-specific motor vehicle sales and use tax forms in several ways. For example, the California Report of Sale form also requires detailed information about the seller, the purchaser, and the vehicle being sold, including its make, model, and Vehicle Identification Number (VIN). Just like the Nebraska form, it's designed to calculate the taxable amount after deductions like trade-ins and rebates and determine the sales tax owed. This allows states to collect appropriate sales and use taxes on vehicle transactions, ensuring that buyers contribute to state revenue through these purchases.

Additionally, it closely resembles the New York State Department of Taxation and Finance's Statement of Transaction – Sale or Gift of Motor Vehicle, Trailer, All-Terrain Vehicle (ATV), Vessel (Boat), or Snowmobile form. This document also captures comprehensive transaction details, including buyer and seller information and specifics about the vehicle. It calculates the tax due on the transaction, considering trade-ins and exempt sales. What makes these forms akin is not only their purpose to record and tax vehicle sales accurately but also their role in deterring fraudulent activities through detailed reporting and the requirement for seller and buyer acknowledgements.

On a broader scale, the Nebraska form shares characteristics with the Federal Odometer Disclosure Statement that is required for all vehicle sales across the United States. Although the main focus of the odometer statement is to report the mileage at the time of sale to prevent odometer fraud, it also includes essential details such as the name and address of the seller and buyer and the vehicle description. Both forms are crucial for a transparent and lawful transfer of ownership, ensuring that all parties are accurately reporting critical information pertaining to the sale.

When completing the Nebraska Sales Tax Statement form for a motor vehicle or trailer sale, it’s important to adhere to certain guidelines to ensure the process goes smoothly. The dos and don'ts listed below will help sellers and buyers navigate the form filling process effectively.

Dos:

Don'ts:

By following these guidelines, sellers and purchasers can navigate the completion of the Nebraska Sales Tax Statement with confidence, ensuring compliance with state regulations and a smoother vehicle registration process.

There are several misconceptions regarding the Nebraska Sales Tax Statement form that can lead to confusion for both buyers and sellers of motor vehicles or trailers. Understanding these common errors can help ensure that the process runs smoothly and in compliance with the law. Here are five of the most common misunderstandings:

Everyone must pay the sales tax as stated on the form, with no exceptions. This is not entirely true. There are several exemptions outlined on the form, such as purchases made by an exempt organization, transfers between corporate entities, or vehicles purchased by Native American Indians residing on a reservation. Each exemption requires specific documentation to be considered valid.

The tire fee applies to all vehicle sales. While the tire fee is a common charge in vehicle sales, there are exceptions. For example, certain types of exemptions listed on the form, like purchases by certain exempt organizations or categories, may not require payment of the tire fee. This highlights the importance of reviewing all applicable exemptions when completing the form.

Trade-in allowances are straightforward and apply equally to all transactions. The process of accounting for trade-ins can be complex, particularly when dealing with leased vehicles. In some cases, a leased vehicle cannot be used as a trade-in unless the lessee has fulfilled specific requirements, such as registering and paying the tax on the buy-out amount. Understanding these details is crucial.

The form is only for use by licensed dealers. This belief is incorrect. While dealers are the primary users, individuals who sell a motor vehicle or trailer are also required to complete and distribute the form properly, although their obligations, particularly regarding the collection and remittance of sales tax, may differ from those of dealers.

Filing the form is the final step in the sales tax process. Actually, completing and submitting this form is just one part of the process. Both purchasers and sellers must ensure that the applicable taxes and fees, along with any documentation for exemptions, are submitted to the correct county or state office as required. Additionally, keeping a copy of the form for records is essential, as it may be needed to resolve future discrepancies or audits.

Understanding these nuances ensures compliance with Nebraska's laws and can help avoid potential legal and financial penalties. Misunderstandings can lead to errors in tax payment and reporting, so reviewing the form's instructions and seeking clarification when necessary is advisable.

Every individual involved in the sale of a motor vehicle or trailer should complete the Nebraska Sales Tax Statement form, ensuring it's given to the buyer. This form plays a critical role in the documentation and tax calculation process associated with the sale.

Forms are accessible through the Department of Revenue or the county treasurer in the county where the vehicle will be registered. This availability makes it easier for both sellers and buyers to comply with state requirements.

It is mandatory to include various details on the form, such as the seller's and purchaser's names and addresses, the vehicle or trailer description including make, body type, year, and VIN, and the date of purchase. This ensures a comprehensive record of the transaction.

Tax and tire fee calculations are an integral part of the form, guiding sellers and buyers through determining the total amount due, including sales or use tax and any applicable tire fees. The form provides a structured way to calculate what is owed, minimizing errors.

Submitting the completed form to the designated authority, along with the appropriate payment, is required within 30 days from the date of purchase. Late submissions are subject to penalties and interest charges, emphasizing the importance of timely compliance.

Exemptions and rebates might apply under certain conditions, which can reduce the overall tax liability. For instance, transactions involving exempt organizations, trade-ins, manufacturer's rebates, and certain purchases by or for disabled persons are subject to specific considerations. It is important to carefully review the eligibility for any such exemptions.

To avoid legal consequences, it is critical that all information provided on the form is accurate and truthful. Willful submission of false or fraudulent statements may result in severe penalties, including a Class IV felony charge. This underscores the seriousness with which the state regards these transactions.

Form 941 Irs - Nonresident individuals receiving income from Nebraska sources get a copy of Form 14N, clarifying the tax withheld on their behalf.

Nebraska Gas Tax - The inclusion of operation descriptions in the form allows for a personalized claim process, tailoring each submission to the claimant's unique agricultural context.

Nebraska Ged Practice Test - An overview of the Nebraska GED Transcript Request form, including fees and mailing instructions.